U.S. stock futures slip lower; Cook’s firing increases Fed independence worries

Introduction & Market Context

GMS Inc . (NYSE:GMS), a leading North American distributor of building products, presented its fourth quarter and full-year fiscal 2025 results on June 18, 2025, revealing significant earnings pressure amid challenging market conditions. Despite implementing substantial cost reduction measures, the company reported sharp declines in both quarterly and annual profits, though strong cash flow generation provided a bright spot.

In premarket trading, GMS shares rose 7.76% to $78.92, suggesting investors were encouraged by the company’s outlook and cash generation despite the earnings decline. This marks a notable shift from the previous quarter when shares plummeted nearly 13% following Q3 results.

Quarterly Performance Highlights

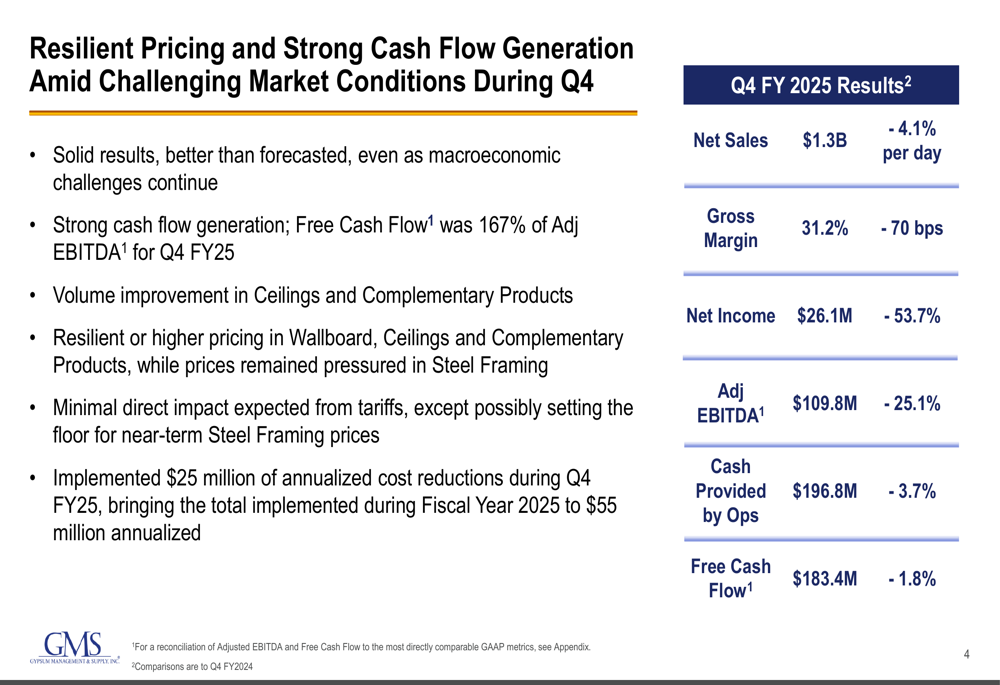

GMS reported Q4 FY2025 net sales of $1.3 billion, representing a 4.1% per-day decline compared to the same period last year. Net income fell sharply by 53.7% to $26.1 million, while Adjusted EBITDA decreased by 25.1% to $109.8 million. Despite these declines, the company highlighted its strong cash flow generation, with free cash flow reaching $183.4 million, representing an impressive 167% of Adjusted EBITDA.

As shown in the following quarterly results overview:

The company maintained a gross margin of 31.2%, down 70 basis points year-over-year but flat compared to the previous quarter. Management attributed the resilience in margins to strong pricing across Wallboard, Ceilings, and Complementary Products, which helped offset volume declines.

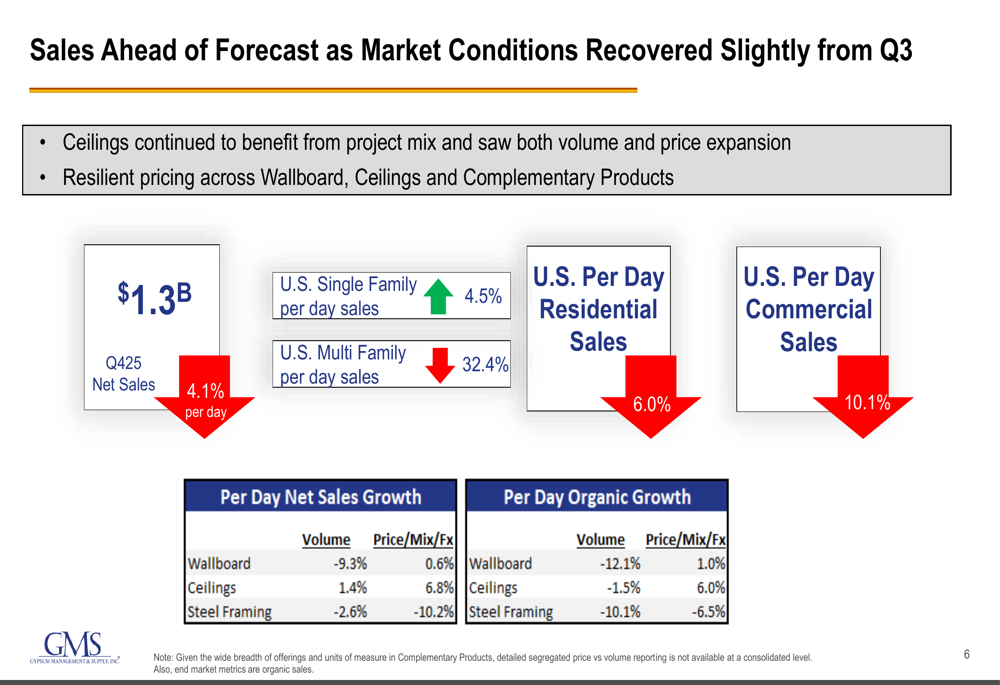

A detailed analysis of sales performance reveals significant disparities across market segments:

The U.S. single-family segment showed signs of recovery with a 4.5% increase in per-day sales, while multi-family sales plummeted by 32.4%. Commercial sales also declined by 10.1% on a per-day basis. These mixed results reflect broader market conditions, with high interest rates and economic uncertainty continuing to weigh on construction activity.

Detailed Financial Analysis

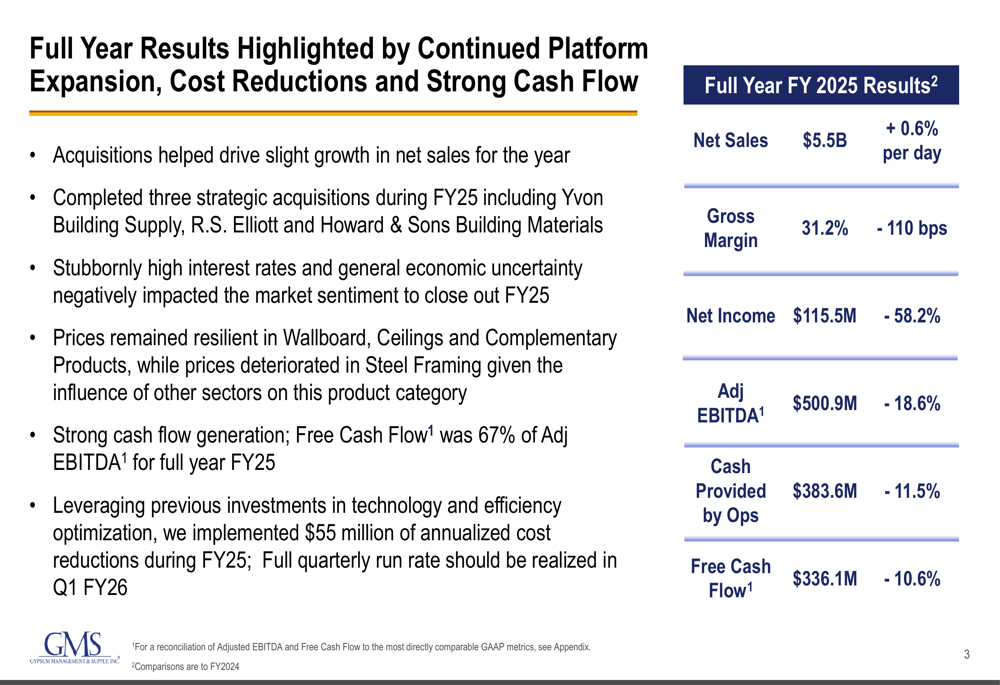

For the full fiscal year 2025, GMS reported net sales of $5.5 billion, a modest 0.6% per-day increase from FY2024. However, net income fell by 58.2% to $115.5 million, and Adjusted EBITDA declined by 18.6% to $500.9 million. The company completed three strategic acquisitions during the year, which helped drive the slight growth in net sales.

The full-year performance summary highlights both challenges and areas of resilience:

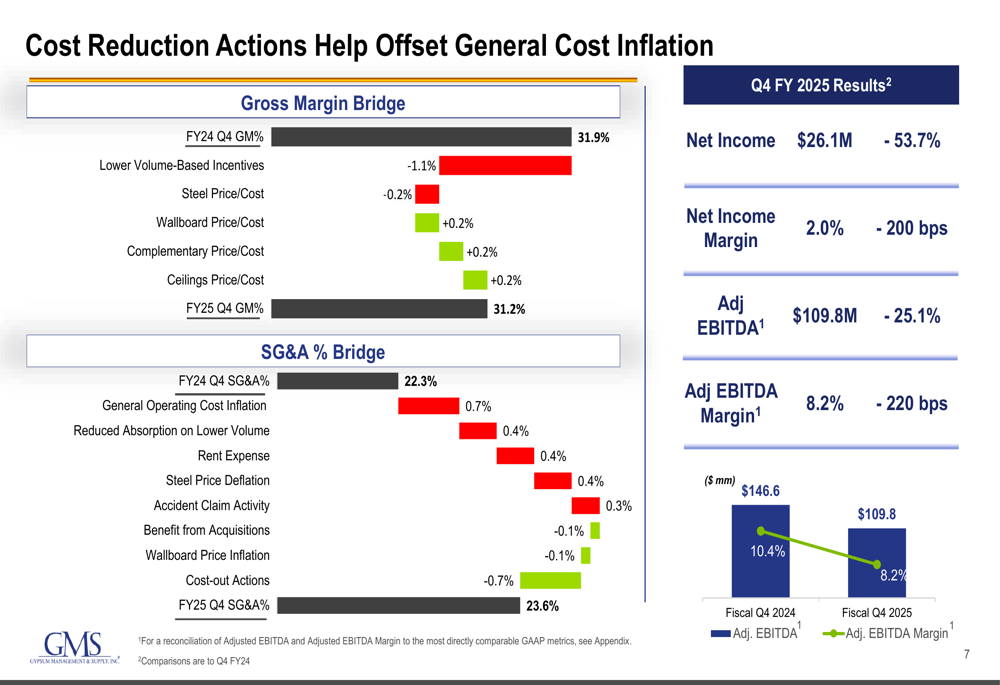

Management has implemented aggressive cost reduction measures to mitigate margin pressure, with $25 million in annualized cost reductions implemented in Q4 alone and $55 million for the full year. These efforts are reflected in the company’s margin analysis:

The gross margin bridge illustrates how various factors affected margins, with lower volume-based incentives having the most significant negative impact (-1.1%), while price/cost improvements in Wallboard, Complementary Products, and Ceilings each contributed positively (+0.2%).

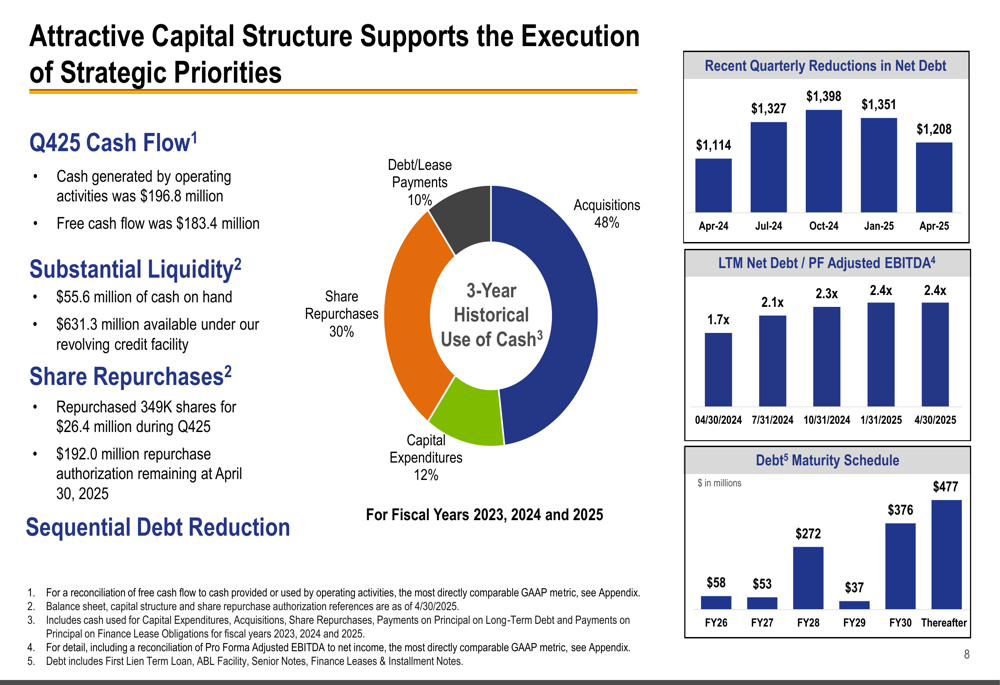

GMS has maintained a solid capital structure despite market challenges. The company ended the fiscal year with $55.6 million in cash and $631.3 million in available credit. During Q4, GMS repurchased 349,000 shares for $26.4 million and reduced its debt sequentially:

Strategic Initiatives

GMS continues to execute its strategic priorities across four key pillars: expanding share in core products, growing complementary products, platform expansion, and driving improved productivity and profitability. The company’s acquisition strategy remains focused on these areas, with three strategic acquisitions completed during FY2025.

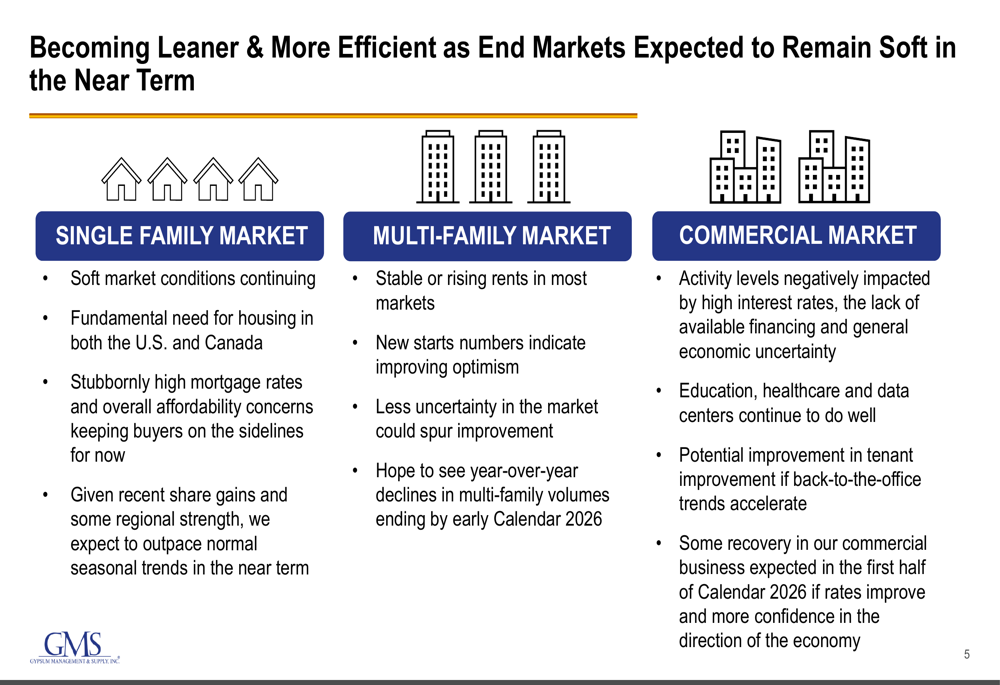

Management provided a detailed assessment of end market conditions, which informs their strategic approach:

The single-family market shows some regional strength expected to outpace normal seasonal trends, while the multi-family market is stabilizing with rising rents. The commercial market continues to face challenges from high interest rates, though education, healthcare, and data centers are performing relatively well. Management anticipates some recovery in the first half of calendar 2026.

Forward-Looking Statements

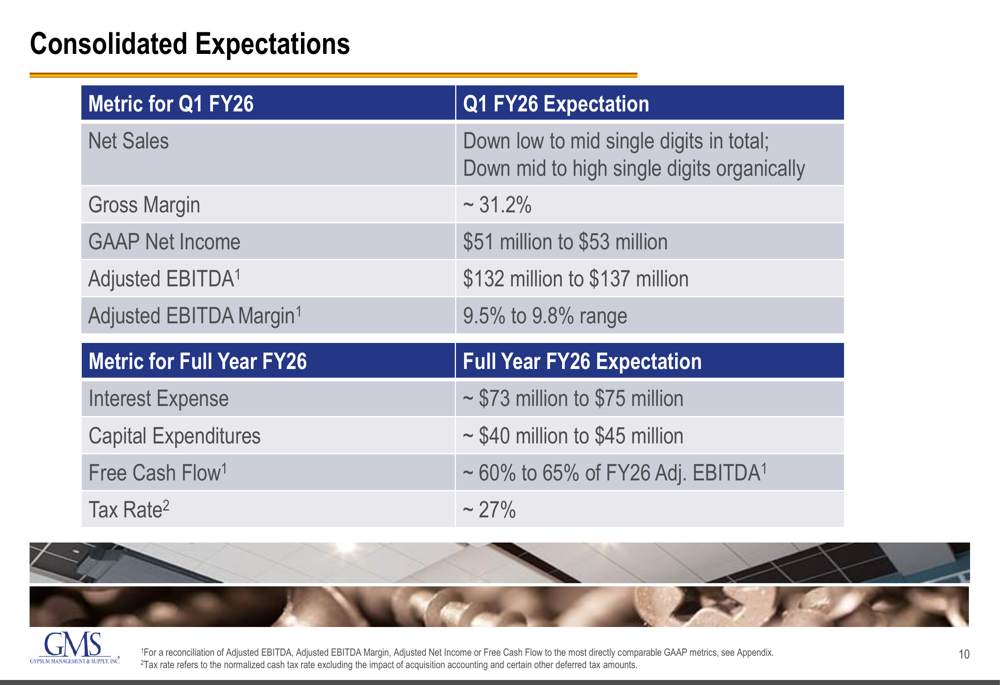

Looking ahead to fiscal 2026, GMS provided guidance for both the first quarter and full year. For Q1 FY26, the company expects:

Net sales are projected to decline in the low to mid-single digits, with organic sales down in the mid to high single digits. Gross margin is expected to remain stable at approximately 31.2%, while GAAP net income is forecast between $51 million and $53 million. Adjusted EBITDA is projected to range from $132 million to $137 million, with margins between 9.5% and 9.8%.

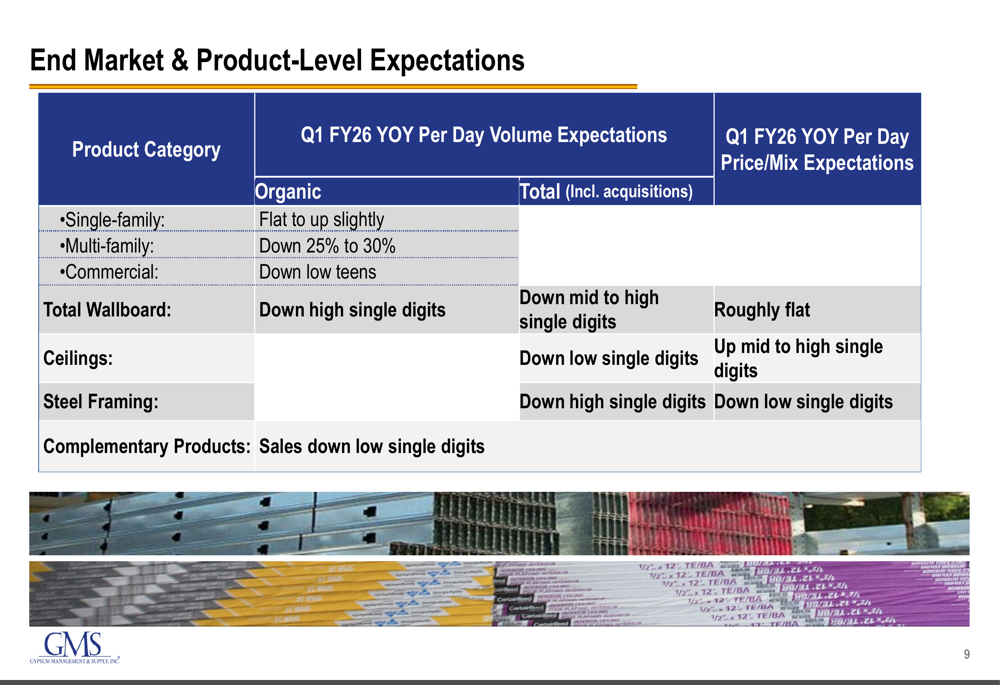

The company also provided more specific expectations for different product categories and market segments:

Single-family volumes are expected to be flat to up slightly in Q1 FY26, while multi-family volumes are projected to decline by 25% to 30%. Commercial volumes are anticipated to decrease in the low teens. Wallboard volumes are expected to decline in the high single digits, though pricing should remain roughly flat.

Despite the challenging environment, management expressed cautious optimism about a gradual market recovery, particularly in the single-family segment. The company’s focus on cost management, cash generation, and strategic acquisitions positions it to navigate the current market conditions while preparing for eventual improvement.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.