Interactive Brokers shares jump as it secures spot in S&P 500

Introduction & Market Context

Integra LifeSciences (NASDAQ:IART) reported its first quarter 2025 results on May 5, revealing continued operational challenges amid compliance investments and international headwinds. The medical technology company’s stock, which closed at $16.85 on May 2, was indicated down 4.75% in pre-market trading following the earnings release, reflecting investor concerns about the negative organic growth and reduced earnings guidance.

The company has seen its share price decline significantly over the past year, with the stock currently trading near its 52-week low of $14.45, far below its 52-week high of $32.66. This downward trend highlights the ongoing challenges Integra faces as it works through regulatory compliance issues and navigates a complex global trade environment.

Quarterly Performance Highlights

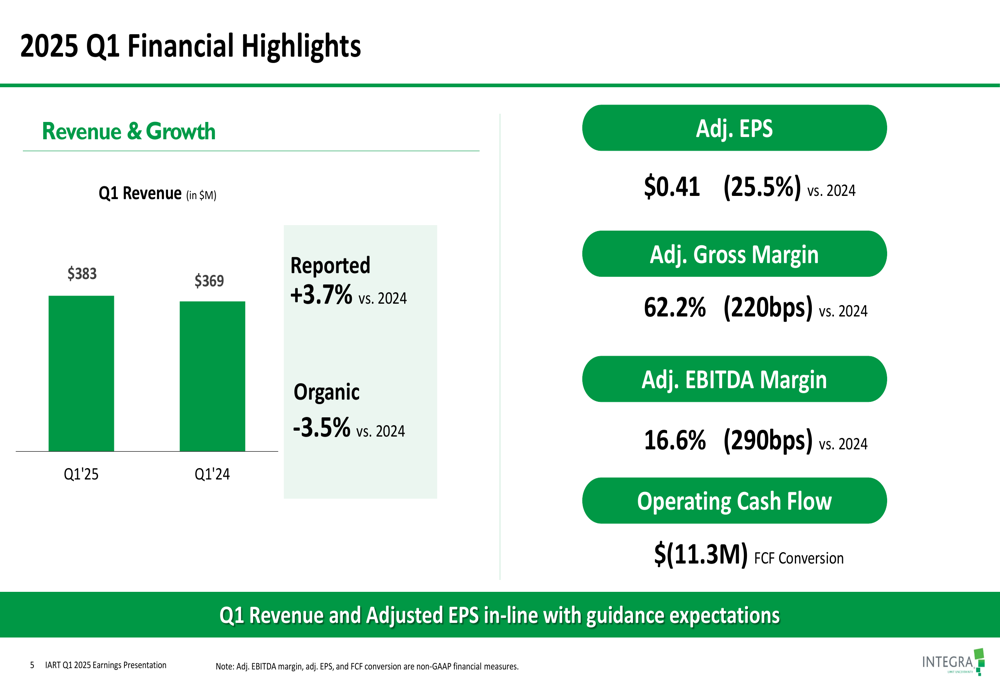

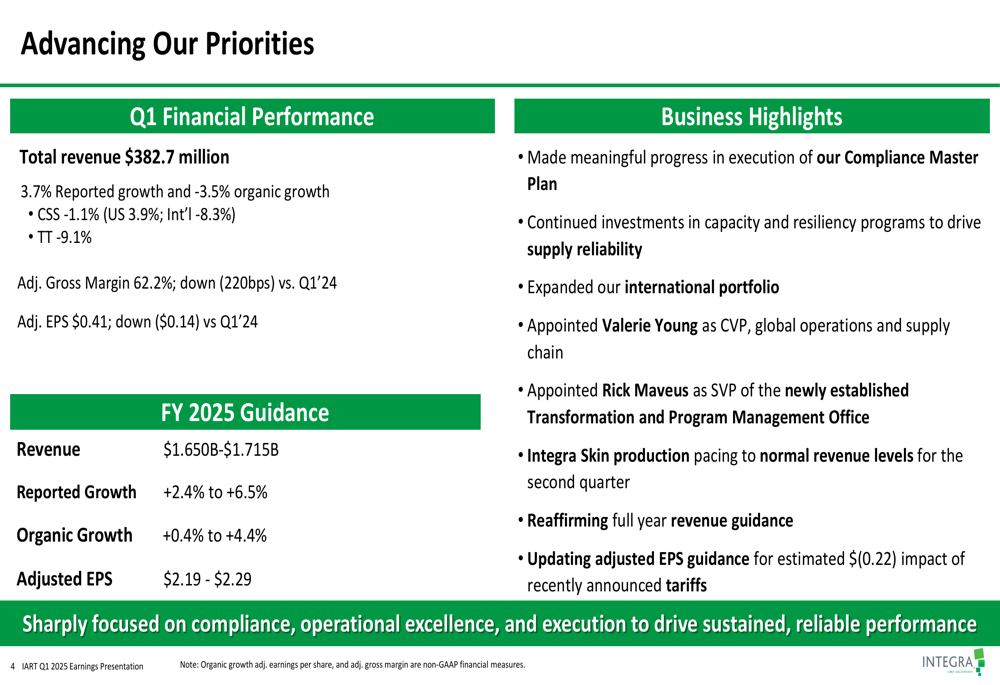

Integra reported total revenue of $382.7 million for Q1 2025, representing 3.7% reported growth but a 3.5% organic decline compared to the same period last year. The company’s adjusted earnings per share came in at $0.41, down $0.14 from Q1 2024.

As shown in the following financial highlights chart:

The company’s profitability metrics showed significant pressure, with adjusted gross margin declining 220 basis points to 62.2% and adjusted EBITDA margin falling 290 basis points to 16.6% compared to the prior year. Operating cash flow was negative at $(11.3) million.

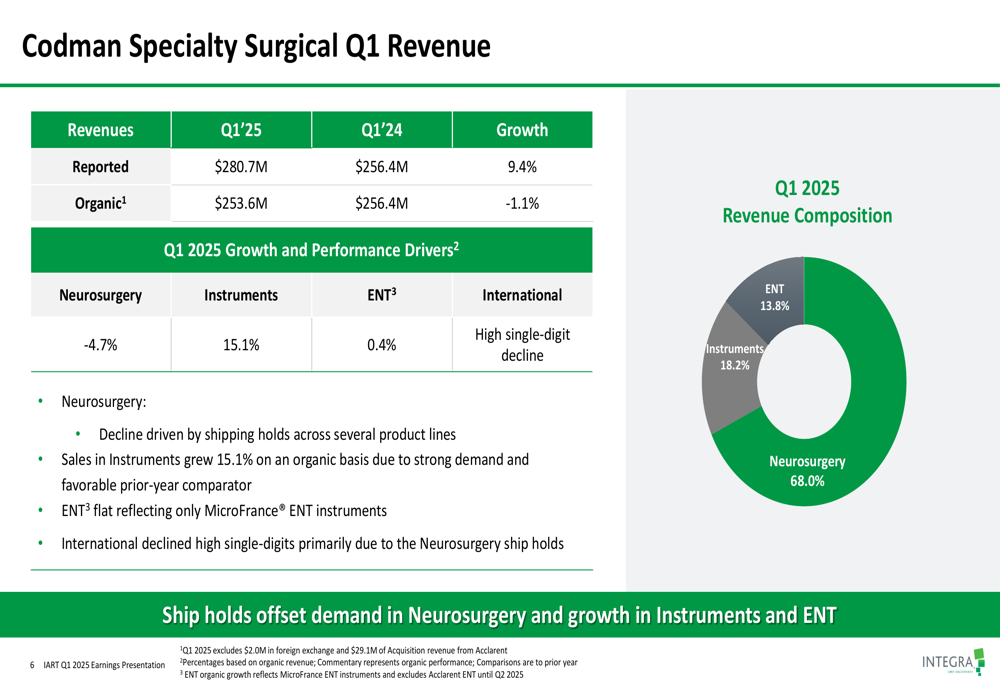

Performance varied across Integra’s business segments. The Codman Specialty Surgical (CSS) division, which accounts for approximately 73% of total revenue, reported 9.4% reported growth but a 1.1% organic decline. Within CSS, U.S. sales grew 3.9% while international sales fell 8.3%.

The following chart breaks down the CSS segment performance:

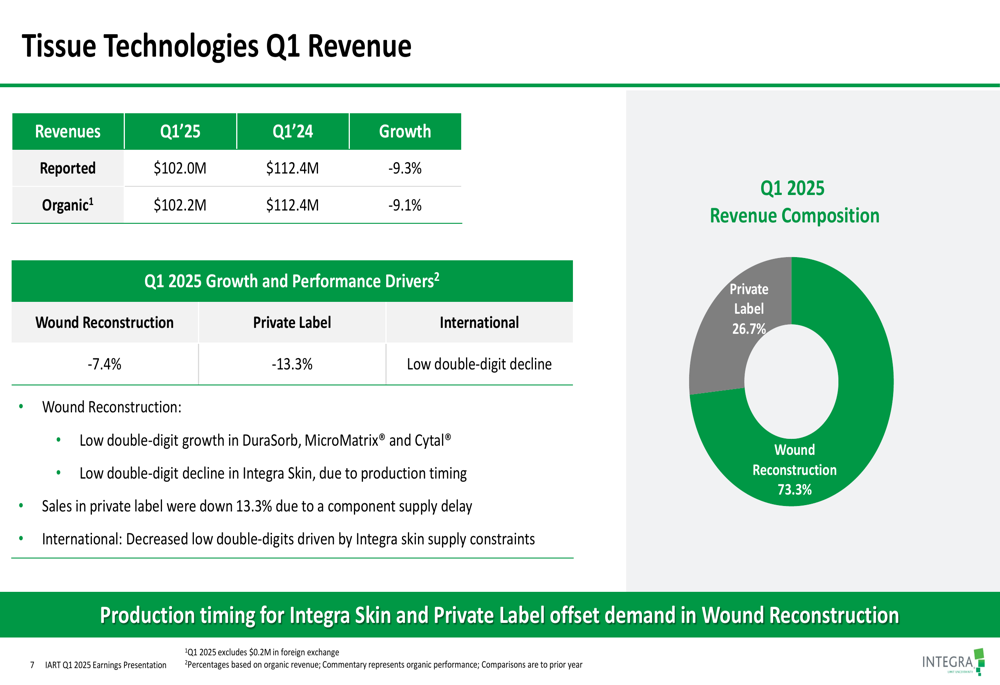

The Tissue Technologies segment, representing about 27% of total revenue, faced more significant challenges with a 9.1% organic decline. Both Wound Reconstruction (-7.4%) and Private Label (-13.3%) products experienced substantial decreases, with international sales showing a low double-digit decline.

The Tissue Technologies segment breakdown is illustrated here:

Detailed Financial Analysis

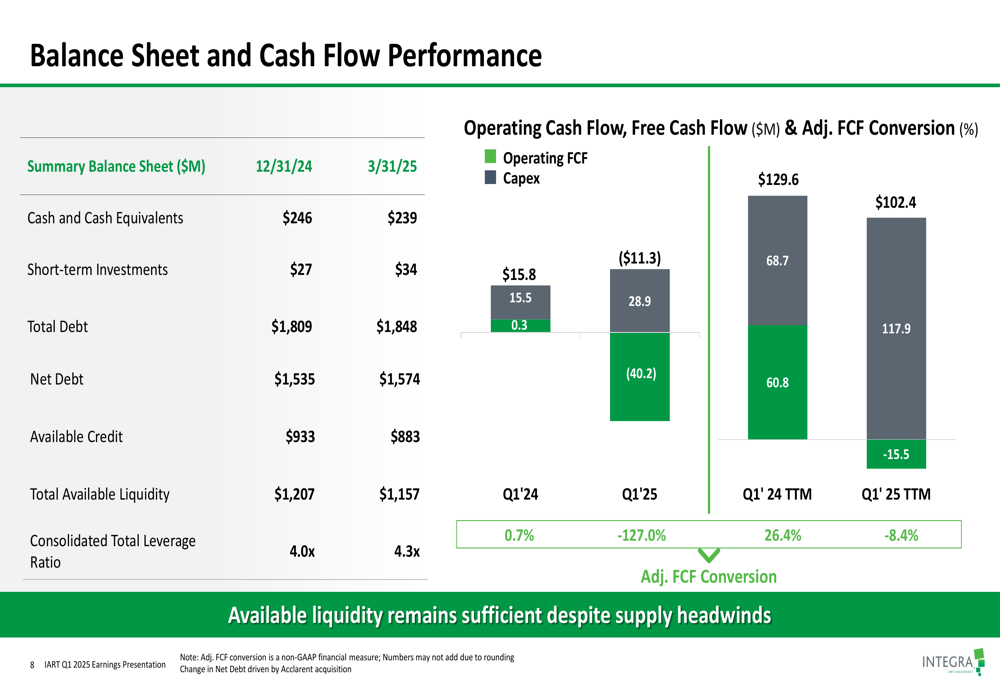

Integra’s balance sheet showed some deterioration during the quarter, with net debt increasing to $1,574.4 million as of March 31, 2025, compared to $1,535.0 million at the end of 2024. The company’s consolidated total leverage ratio rose to 4.3x from 4.0x over the same period.

Available liquidity remained substantial at $1,157 million, though this represented a decrease from $1,207 million at year-end 2024. The company noted that this liquidity remains sufficient despite ongoing supply chain headwinds.

The following chart illustrates the company’s balance sheet and cash flow performance:

Free cash flow was negative at $(40.2) million for Q1 2025, compared to a positive $0.3 million in Q1 2024. The adjusted free cash flow conversion rate deteriorated significantly to -126.9% from 0.7% in the prior year period. On a trailing twelve-month basis, free cash flow was $(15.5) million, down from $60.8 million in the comparable period.

Forward-Looking Statements

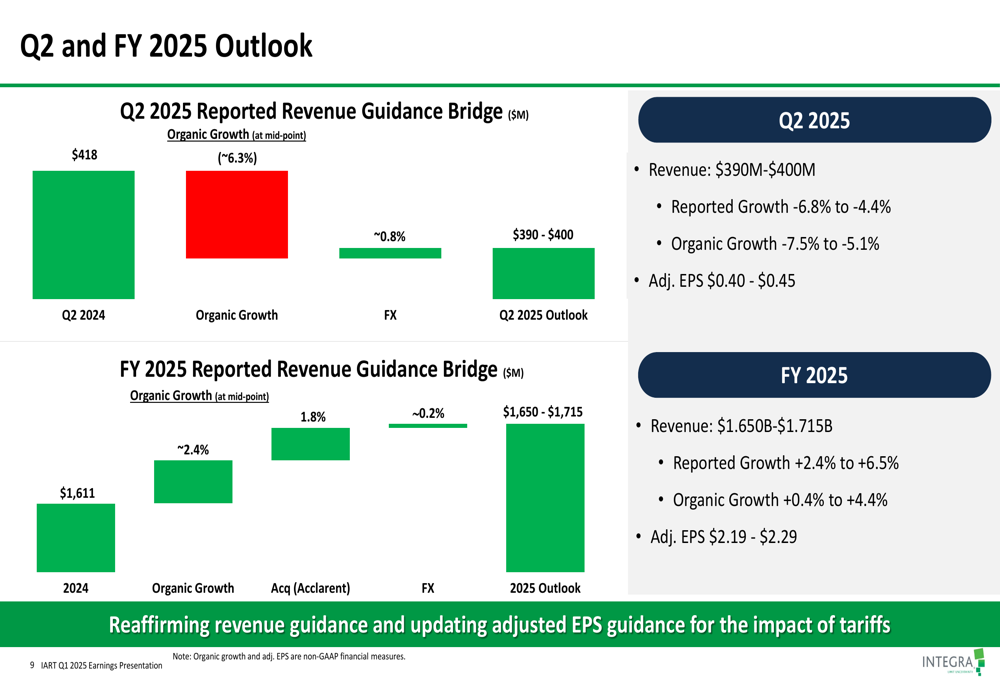

Despite the challenging Q1 results, Integra reaffirmed its full-year 2025 revenue guidance of $1.650 billion to $1.715 billion, representing reported growth of 2.4% to 6.5% and organic growth of 0.4% to 4.4%. However, the company updated its adjusted EPS guidance to $2.19-$2.29, incorporating an estimated $0.22 negative impact from tariffs.

For Q2 2025, Integra expects revenue between $390 million and $400 million, representing a reported decline of 6.8% to 4.4% and an organic decline of 7.5% to 5.1%. Adjusted EPS for Q2 is projected to be between $0.40 and $0.45.

The company’s outlook for the remainder of 2025 is illustrated in this guidance chart:

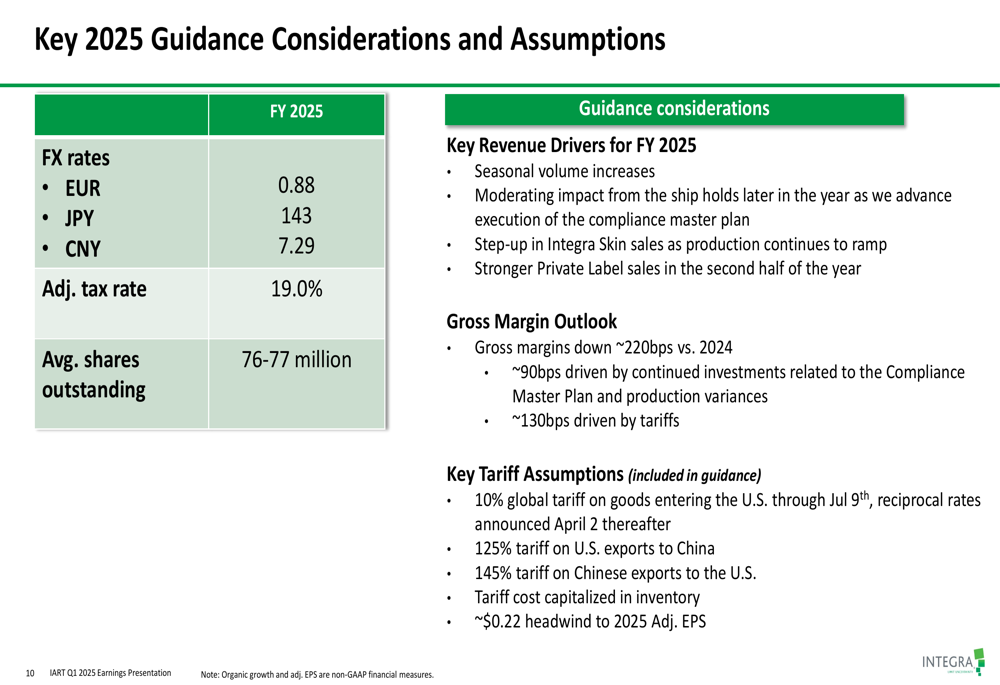

Management highlighted several key assumptions underlying their 2025 guidance, including seasonal volume increases, moderating impact from shipping holds later in the year, increased Integra Skin sales as production ramps up, and stronger Private Label sales in the second half of the year.

The company also detailed the expected impact of tariffs on its business, noting that gross margins are projected to decline approximately 220 basis points versus 2024, with about 130 basis points of that decline attributed directly to tariffs.

The following slide outlines the key guidance considerations and assumptions:

Strategic Initiatives

Integra emphasized progress on several strategic fronts during the quarter. The company reported advancements in its Compliance Master Plan, which is critical to addressing regulatory concerns that have impacted operations. Management also highlighted ongoing investments in capacity and resiliency programs to strengthen the supply chain.

The company made key leadership appointments, including Valerie Young as Corporate Vice President of global operations and supply chain, and Rick Maveus as Senior Vice President of Transformation and Program Management Office. These appointments underscore Integra’s focus on operational improvements and transformation initiatives.

Management noted that Integra Skin production is expected to return to normal revenue levels in Q2, which should help improve performance in the Tissue Technologies segment. The company also expanded its international portfolio, though international sales continued to face significant headwinds across both business segments.

As shown in this comprehensive overview of the company’s priorities and performance:

Integra’s focus remains on executing its Compliance Master Plan, improving operational efficiency, and navigating the challenging global trade environment while positioning for a recovery in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.