TSX lower after index logs fresh record closing high

Introduction & Market Context

Matador Resources Company (NYSE:MTDR) reported record quarterly production in its second quarter 2025 earnings presentation released on July 22, 2025. The company’s stock closed at $49.86 on the day of the announcement, with a modest 0.28% gain in after-hours trading, according to available market data.

The oil and gas producer continues to demonstrate strong operational performance in the Delaware Basin, maintaining its position as one of the highest-margin operators in the region while balancing production growth with free cash flow generation.

Quarterly Performance Highlights

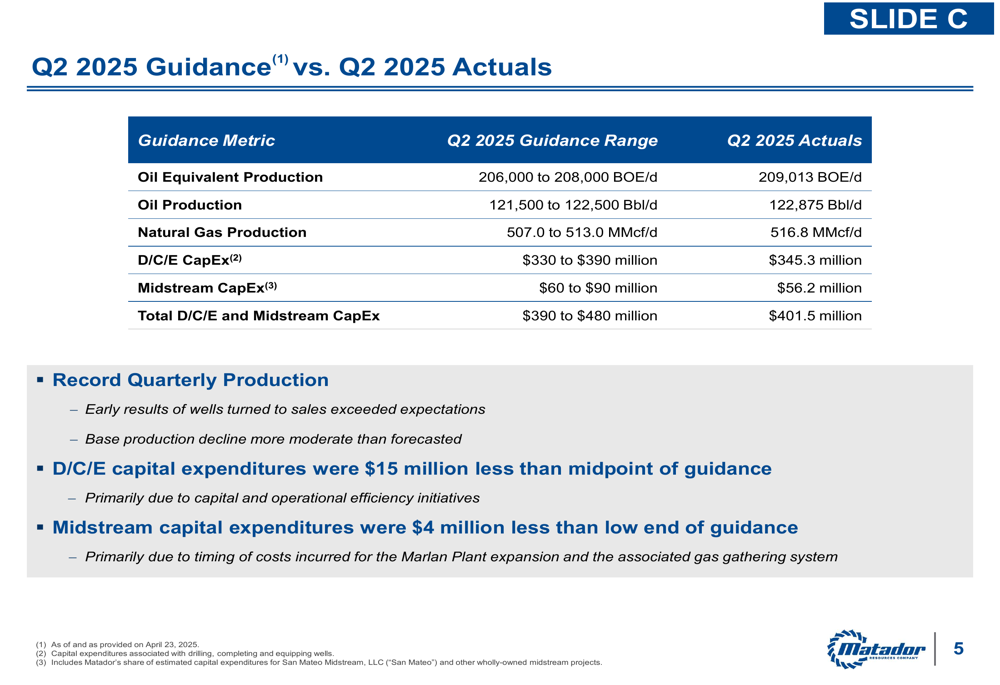

Matador exceeded its production guidance across all key metrics for Q2 2025. The company reported total oil equivalent production of 209,013 BOE/d, surpassing its guidance range of 206,000 to 208,000 BOE/d. Oil production reached 122,875 Bbl/d, exceeding the projected 121,500 to 122,500 Bbl/d, while natural gas production hit 516.8 MMcf/d, above the forecasted 507.0 to 513.0 MMcf/d.

As shown in the following comparison of guidance versus actual results:

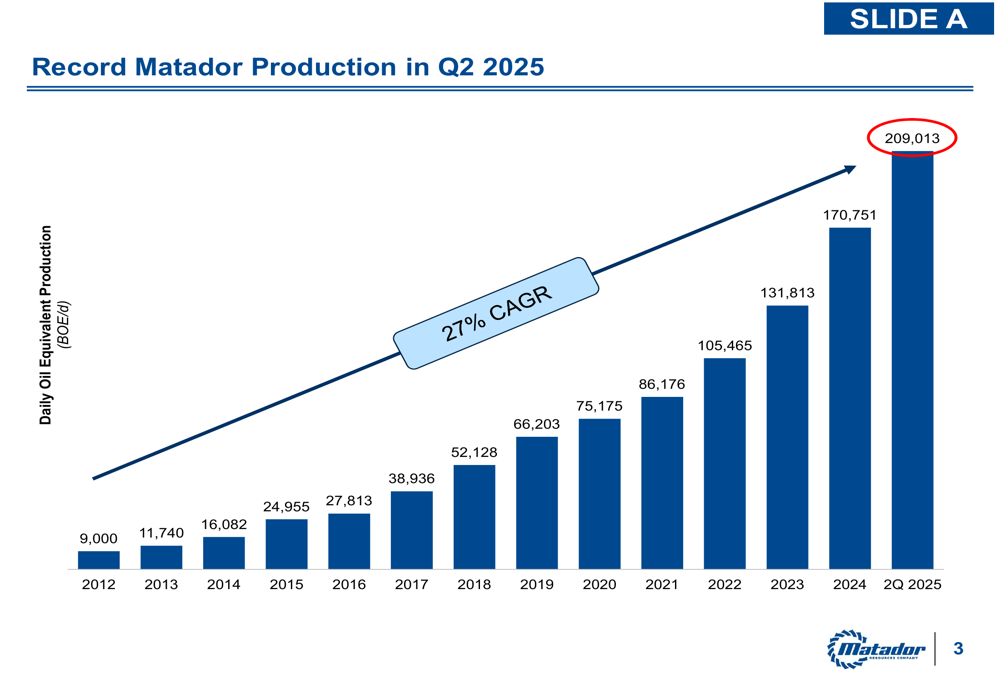

This performance continues Matador’s impressive production growth trajectory, which has expanded at a 27% compound annual growth rate (CAGR) since 2012. The company’s Q2 2025 production of 209,013 BOE/d represents significant growth from the 170,751 BOE/d reported in 2024.

The following chart illustrates this consistent long-term production growth:

Operational Efficiencies

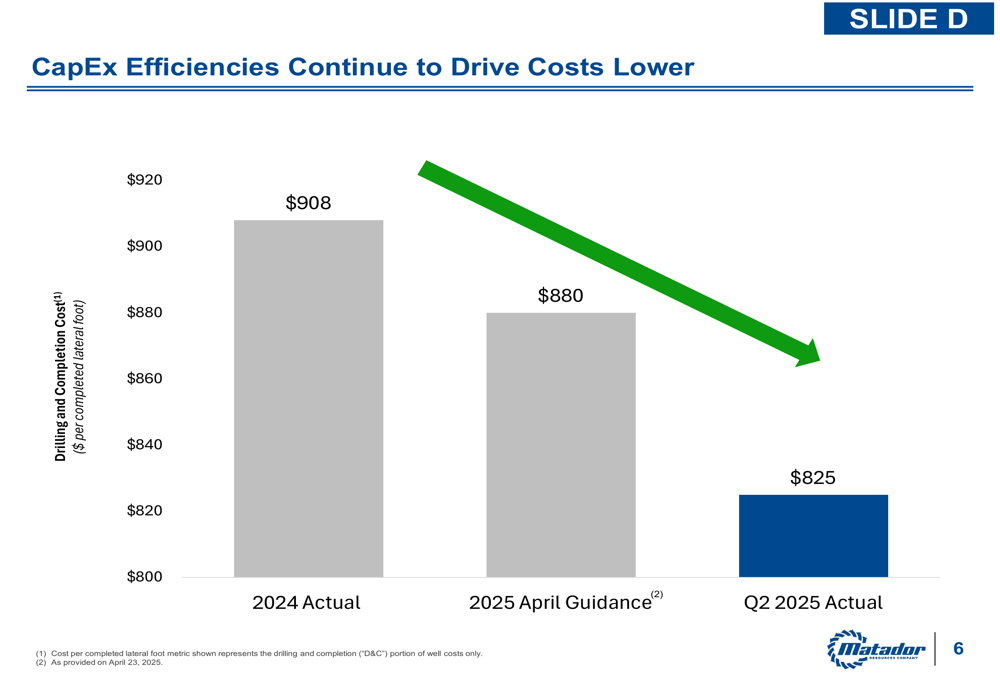

A key driver of Matador’s performance has been its continued improvement in operational efficiencies, particularly in drilling and completion costs. The company reported drilling and completion costs of $825 per completed lateral foot in Q2 2025, a significant reduction from $908 in 2024 and below the April 2025 guidance of $880.

This trend of declining costs is clearly demonstrated in the following chart:

Contributing to these efficiencies is Matador’s MAXCOM Operations Center, which provides 24/7 geosteering and engineering support. The center has generated increasing cost savings, from $1.5 million in 2018 to $9.1 million in 2025 year-to-date, highlighting the company’s commitment to technological integration and operational excellence.

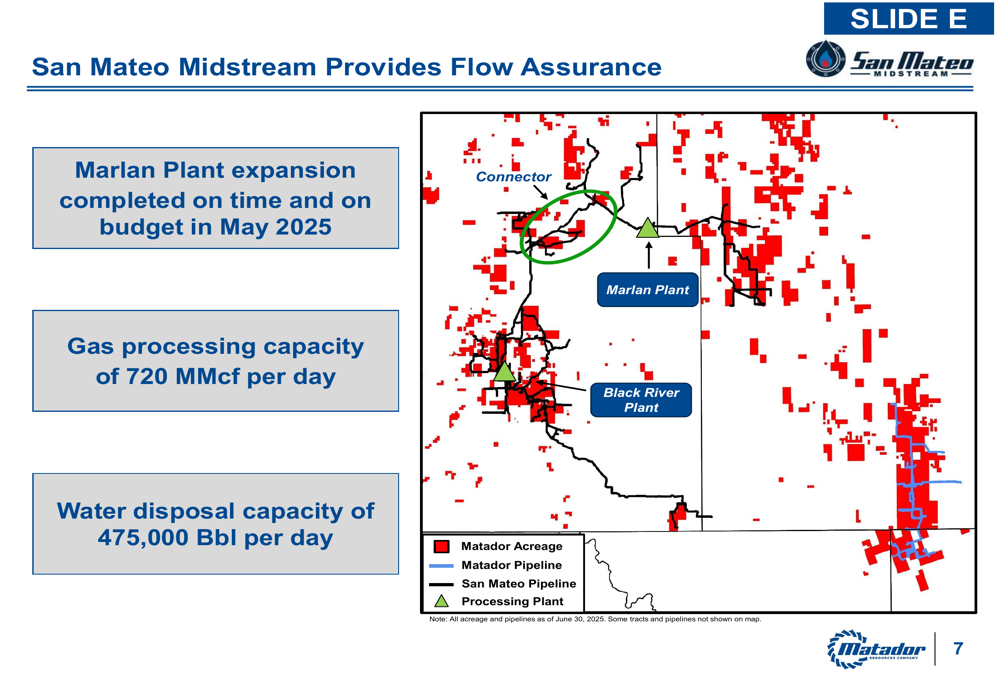

The company’s midstream subsidiary, San Mateo, also plays a crucial role in operational efficiency by providing flow assurance across Matador’s acreage. The Marlan Plant expansion was completed on time and on budget in May 2025, bringing gas processing capacity to 720 MMcf per day and water disposal capacity to 475,000 Bbl per day.

The following map illustrates San Mateo’s midstream infrastructure:

Financial Position and Capital Allocation

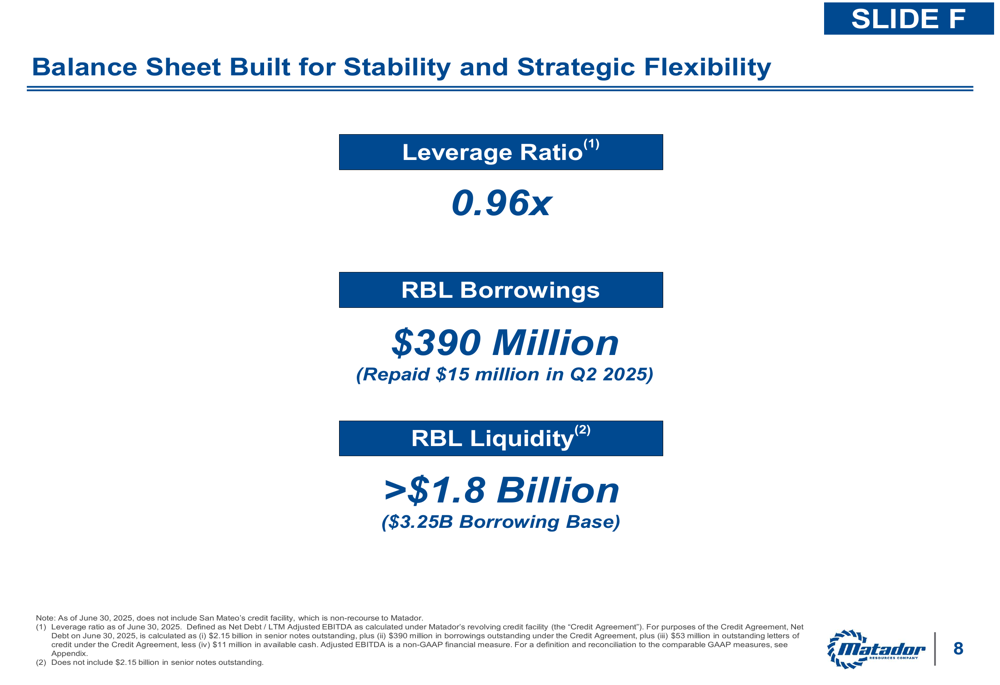

Matador continues to maintain a strong balance sheet with a leverage ratio of 0.96x as of Q2 2025. The company reduced its RBL borrowings by $15 million during the quarter to $390 million, while maintaining liquidity greater than $1.8 billion with a $3.25 billion borrowing base.

The following slide highlights the company’s financial position:

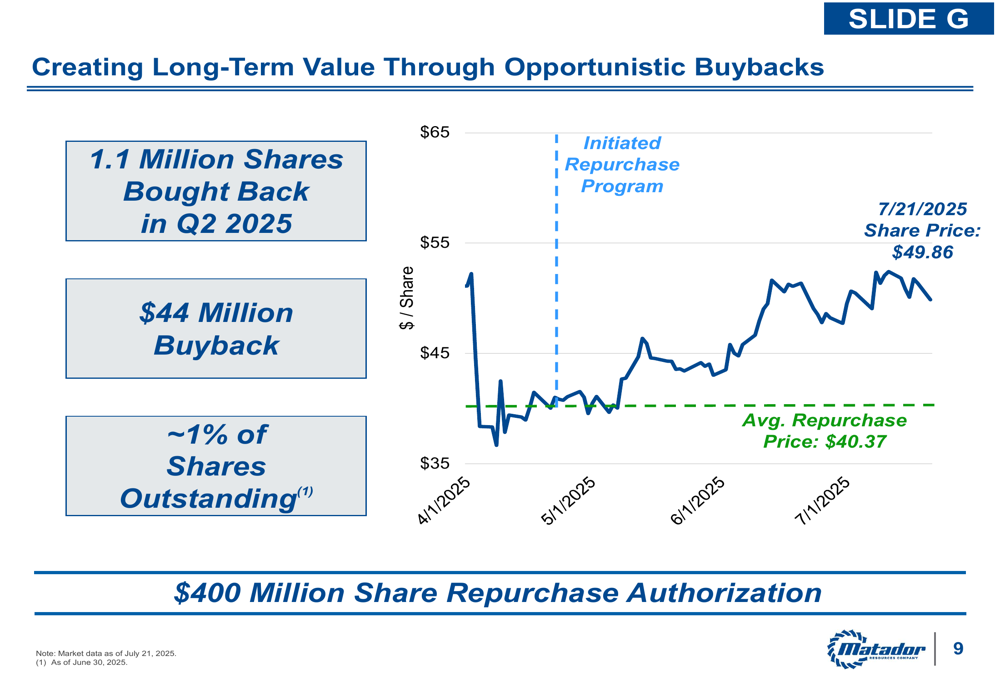

Matador has been actively returning capital to shareholders through both dividends and share repurchases. The company has increased its dividend six times in the past four years, with a current annualized dividend yield of 2.5%. Additionally, Matador repurchased 1.1 million shares (approximately 1% of shares outstanding) for $44 million in Q2 2025 at an average price of $40.37, representing a discount to the July 21, 2025 share price of $49.86.

The company’s share repurchase activity is illustrated in the following chart:

Notably, Matador’s senior management has demonstrated strong alignment with shareholders through significant equity participation. Since January 2021, Section 16 officers have been net buyers of company shares, contrasting with the selling patterns observed at many peer companies.

Strategic Initiatives and Outlook

Looking ahead, Matador has updated its full-year 2025 guidance and provided specific projections for Q3 2025. The company expects oil production of 117.5-119.5 MBbl/d and natural gas production of 495.0-513.0 MMcf/d for the full year. Capital expenditures are projected to be lower in the second half of the year.

For Q3 2025, Matador plans to turn 28 to 32 net operated wells to sales, primarily in the Antelope Ridge area. This aligns with the company’s earlier statements from the Q1 2025 earnings call, where management projected Q2 to be a record quarter for production, with Q3 expected to be lower.

The company maintains a robust inventory of drilling locations in the Delaware Basin, with 2,546 gross (1,667 net) potential Matador-operated locations across multiple formations. This inventory supports the company’s projection of 10-15 years of future drilling opportunities.

Matador has also implemented a strategic hedging program to manage commodity price risk, with 70,000 Bbl/d of oil production hedged for H2 2025 at $52 x $77 collars, representing approximately 60% of production.

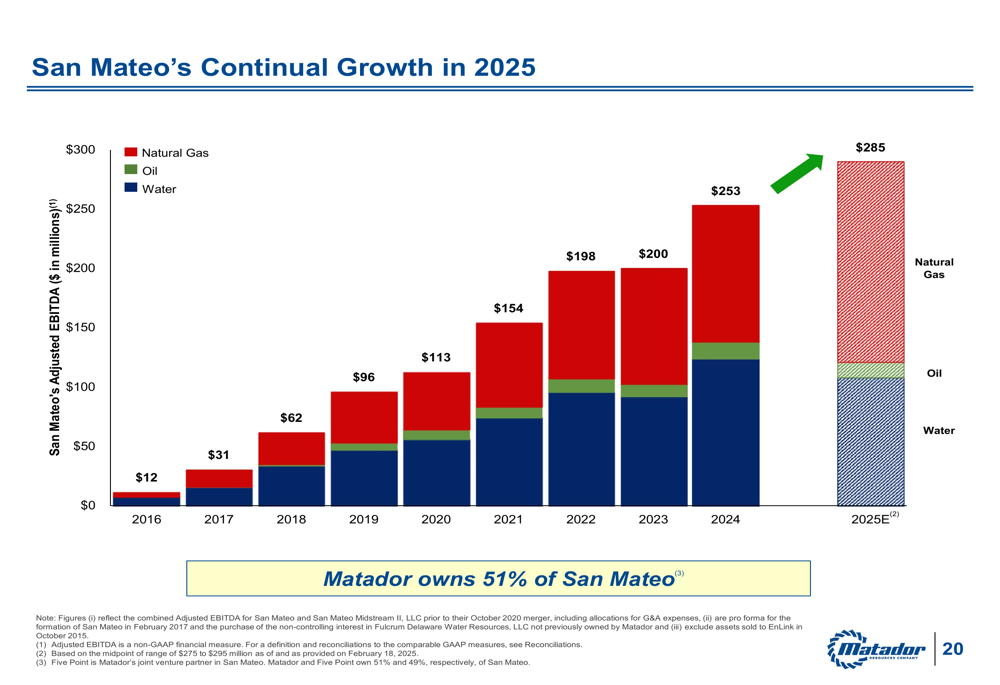

San Mateo continues to be a strategic asset for Matador, with projected 2025 Adjusted EBITDA of $275-$295 million. Matador owns 51% of San Mateo, providing a steady source of cash flow and operational advantages. The following chart shows San Mateo’s consistent growth in Adjusted EBITDA since 2016:

In summary, Matador Resources’ Q2 2025 presentation demonstrates the company’s continued success in balancing production growth with operational efficiencies and financial discipline. With record production, declining costs, a strong balance sheet, and active capital return program, Matador appears well-positioned to maintain its competitive standing in the Delaware Basin while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.