Trump announces trade deal with EU following months of negotiations

Introduction & Market Context

Metropolitan Commercial Bank (NYSE:MCB) released its Q1 2025 investor presentation on April 22, 2025, highlighting the bank’s continued outperformance against regional banking peers. The presentation comes as MCB reported Q1 earnings with EPS of $1.45 (below analyst expectations of $1.56) but revenue of $70.59 million (exceeding forecasts of $67.62 million). Despite the EPS miss, MCB’s stock rose 4.59% in after-hours trading, reflecting investor confidence in the bank’s growth trajectory and strategic positioning.

The bank, which brands itself as "The Entrepreneurial Bank Since 1999," has received several accolades, including recognition from Newsweek as one of America’s Best Regional Banks 2025, Piper Sandler’s Sm-All Stars Bank & Thrift 2024, and a "Top Lender 2024" award. MCB maintains a KBRA rating of BBB+.

Performance Metrics Highlights

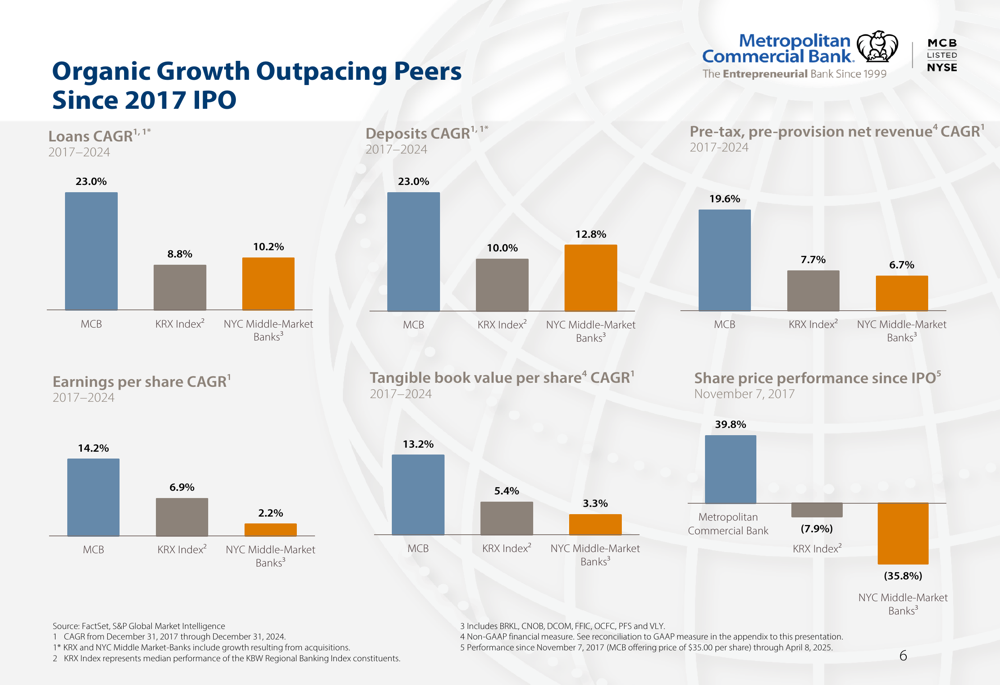

Metropolitan Bank ’s presentation emphasized its substantial outperformance compared to both the KRX Index and NYC Middle-Market Banks since its 2017 IPO. As shown in the following chart, MCB has achieved impressive growth across key metrics:

The bank has delivered a 23.0% CAGR in both loans and deposits from 2017-2024, significantly outpacing the KRX Index (8.8% and 10.0%, respectively) and NYC Middle-Market Banks (10.2% and 12.8%, respectively). Pre-tax, pre-provision net revenue grew at a 19.6% CAGR during the same period, while earnings per share increased at a 14.2% CAGR.

This strong performance has translated to tangible book value per share growth from $27.04 in 2017 to $65.80 in Q1 2025, representing a 13.2% CAGR since the IPO. During the earnings call, CEO Mark DiFazio noted that Q1 2025 marked "our ninth consecutive quarter of book value accretion."

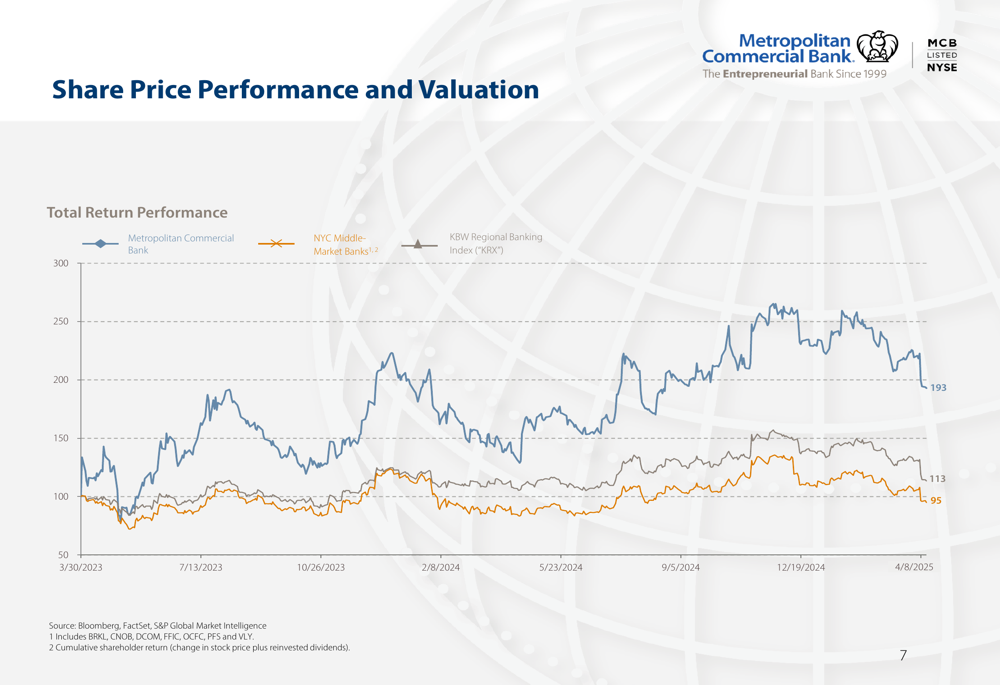

The bank’s share price has also outperformed its peers, as illustrated in this total return performance chart:

Detailed Financial Analysis

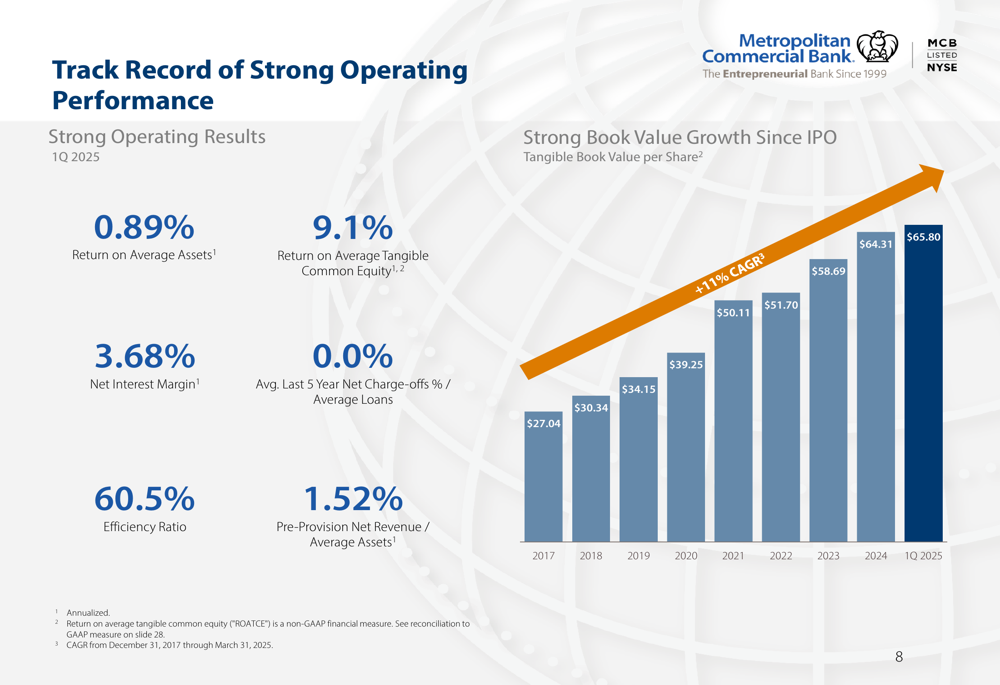

Metropolitan Bank reported solid Q1 2025 operating results with a Return on Average Assets of 0.89%, Return on Average Tangible Common Equity of 9.1%, and Net Interest Margin of 3.68%. The efficiency ratio stood at 60.5%, with Pre-Provision Net Revenue to Average Assets at 1.52%.

The bank has successfully managed its net interest margin despite the challenging rate environment. As shown below, MCB’s NIM expanded to 3.68% in Q1 2025, marking the sixth consecutive quarter of margin expansion according to CFO Dan Daughtry:

During the earnings call, management guided that the full-year NIM is expected to be 3.7% to 3.75%, with additional rate cuts potentially benefiting the NIM by approximately 5 basis points for each 25 basis point cut.

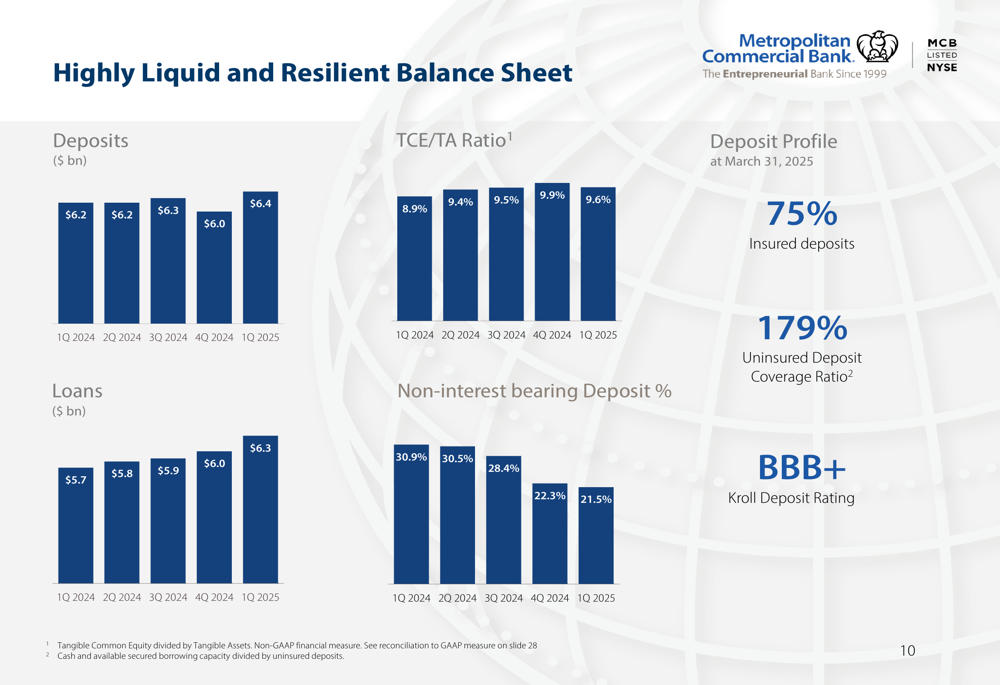

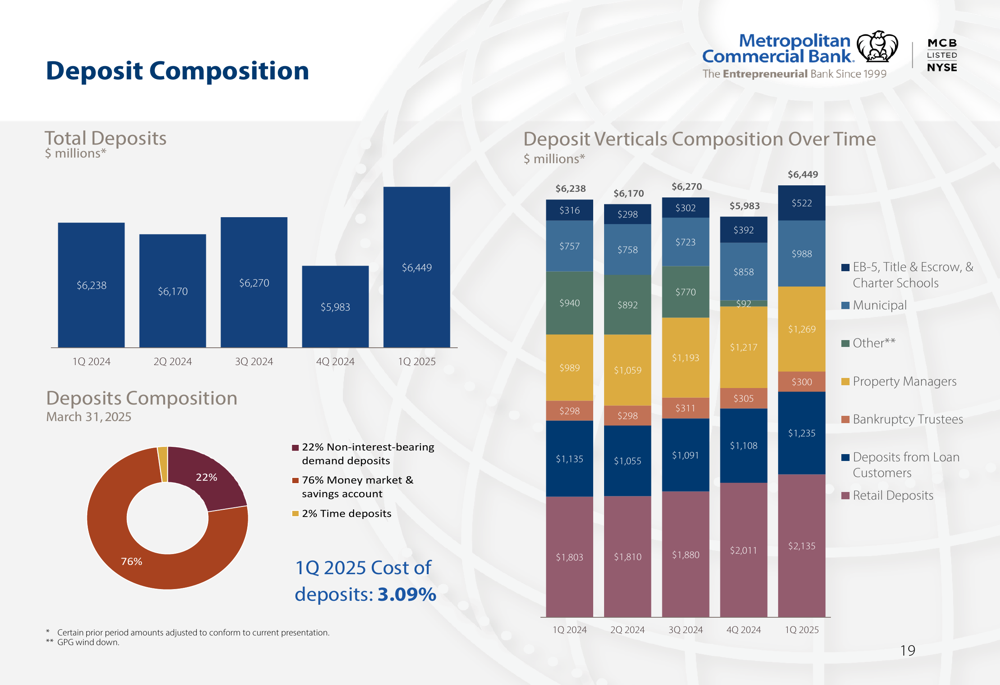

Metropolitan Bank maintains a highly liquid and resilient balance sheet with $6.4 billion in deposits as of Q1 2025, representing growth from $6.2 billion in Q1 2024. The TCE/TA ratio improved to 9.6% from 8.9% year-over-year, while loans increased to $6.3 billion from $5.7 billion:

The bank’s deposit profile features 75% insured deposits and a 179% uninsured deposit coverage ratio. During the earnings call, management highlighted that Q1 deposit growth of $465 million (7.8%) was broad-based, with contributions from all deposit verticals, particularly municipal, EB-5, and lending customers.

Loan Portfolio Diversification

Metropolitan Bank’s $6.4 billion gross loan portfolio (as of March 31, 2025) is well-diversified across various sectors. The presentation detailed the growth and composition of the loan portfolio:

The loan portfolio is heavily weighted toward Commercial Real Estate (CRE), with Skilled Nursing Facilities (SNF) representing 33% of the total. C&I loans account for 16% of the portfolio, while Consumer & 1-4 Family loans make up just 2%. The average Q1 2025 yield on the loan portfolio was 7.25%.

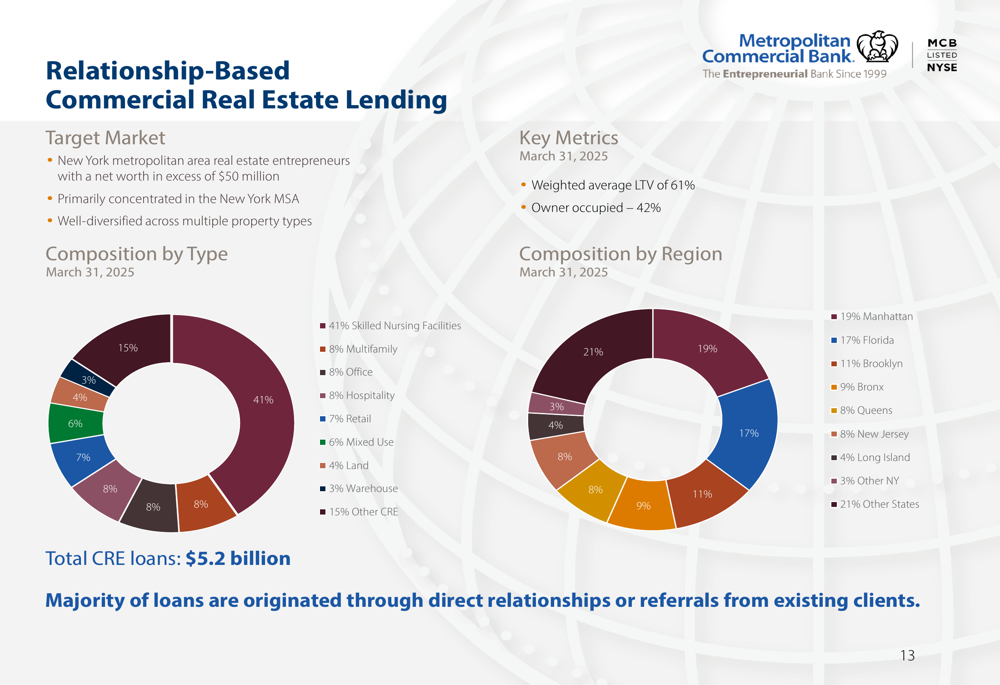

The bank’s CRE lending is relationship-based and primarily focused on the New York metropolitan area, targeting real estate entrepreneurs with a net worth exceeding $50 million. The CRE portfolio maintains a conservative weighted average LTV of 61% and is diversified by property type and geography:

Metropolitan Bank has developed expertise in healthcare lending, particularly in the Skilled Nursing Facility sector. The total healthcare portfolio stood at $2.5 billion as of March 31, 2025:

During the earnings call, management emphasized that asset quality remains strong, with no broad-based negative trends identified in any loan segment, geography, or sector. The Q1 provision expense of $4.5 million supported continued loan growth and included a $1 million specific reserve for a $2 million unsecured line of credit.

Strategic Initiatives

A key focus of Metropolitan Bank’s strategy is its digital transformation initiative, which is expected to be completed by the end of 2025. The project aims to modernize the bank’s core, payments, and online banking systems:

Total (EPA:TTEF) estimated project costs are $17 million (including a 10% contingency), with Q1 2025 digital transformation costs at $219,000. During the earnings call, CFO Dan Daughtry noted that approximately $11 million of IT project-related expenses are expected to be recognized over the remaining three quarters of 2025.

The bank is implementing this digital transformation while maintaining its relationship-driven commercial banking model. As CEO Mark DiFazio stated during the earnings call: "We’re not acquiring teams, bringing on that cost of compensation, and we’re a branch-light franchise as well. So it’s fairly efficient strategy."

Forward-Looking Statements

Metropolitan Bank has updated its 2025 guidance, projecting loan growth of 10-12% (higher than previous guidance) and a full-year NIM of 3.7-3.75%. Management is modeling one 25 basis point rate cut in July, with additional rate cuts expected to benefit the NIM by approximately 5 basis points for each 25 basis point cut.

The bank’s strong capital position (TCE/TA ratio above 9%) provides flexibility for continued growth and capital management. During the earnings call, CEO Mark DiFazio indicated that the board is actively discussing the potential introduction of a dividend, which could help broaden the shareholder base.

Management remains confident in the bank’s ability to navigate the current economic environment. As DiFazio stated: "MCB operates from a position of strength and robust levels of liquidity, capital, and earnings. Our strength is a reflection of our staunch and enduring commitment to safe and sound banking practices."

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.