cathie wood’s ARK sells Tesla stock, buys Baidu and Trade Desk

Introduction & Market Context

Nomura Micro Science Co., Ltd. (TYO:6254), a leading provider of ultra-pure water technology solutions primarily for the semiconductor industry, presented its financial results for the fiscal year ended March 2025 on May 22, 2025. The company operates in a semiconductor market expected to continue growing, driven by memory sector recovery and AI integration, though global economic concerns persist due to trade issues, currency fluctuations, and geopolitical risks.

Quarterly Performance Highlights

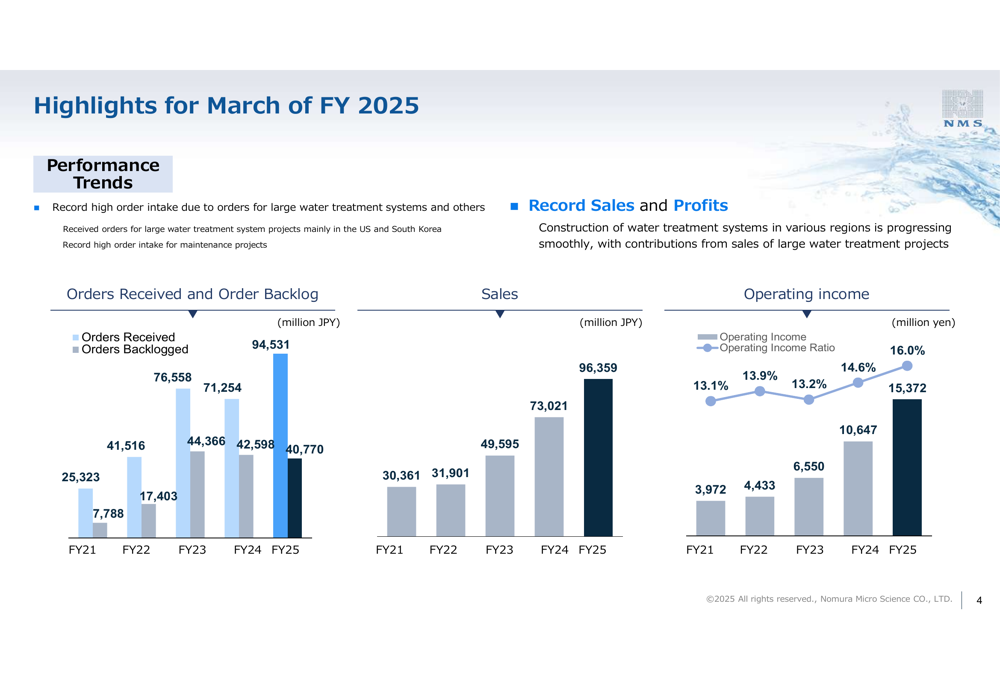

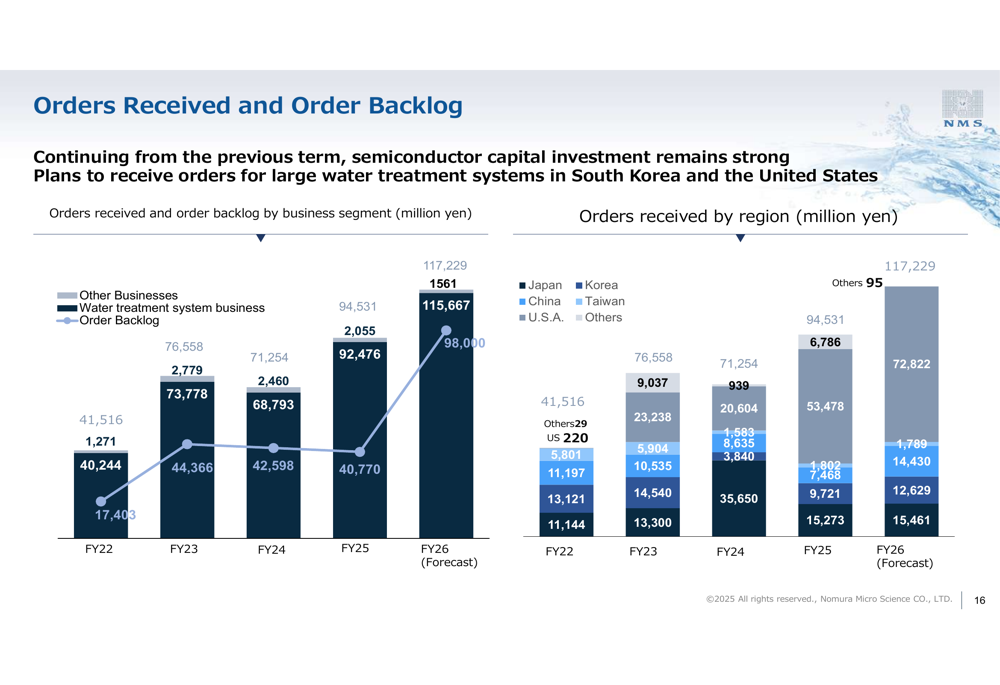

Nomura Micro Science reported exceptional financial performance for FY2025, achieving record highs across key metrics. The company saw substantial growth driven primarily by large water treatment system projects in the United States and South Korea.

As shown in the following chart highlighting FY2025 performance, the company achieved significant year-over-year growth across orders received, sales, and operating income:

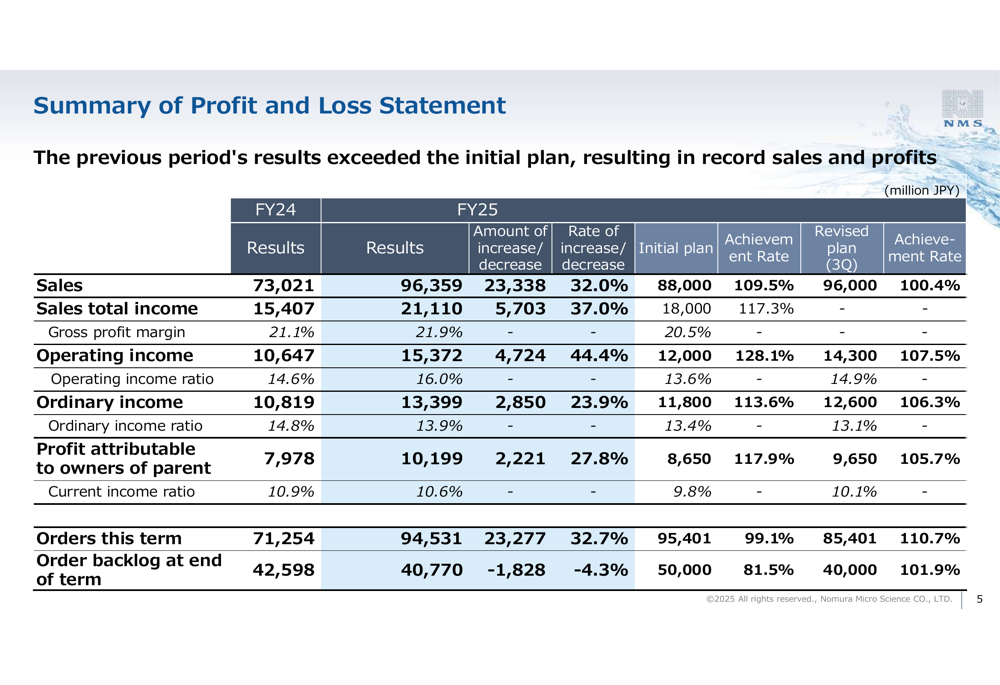

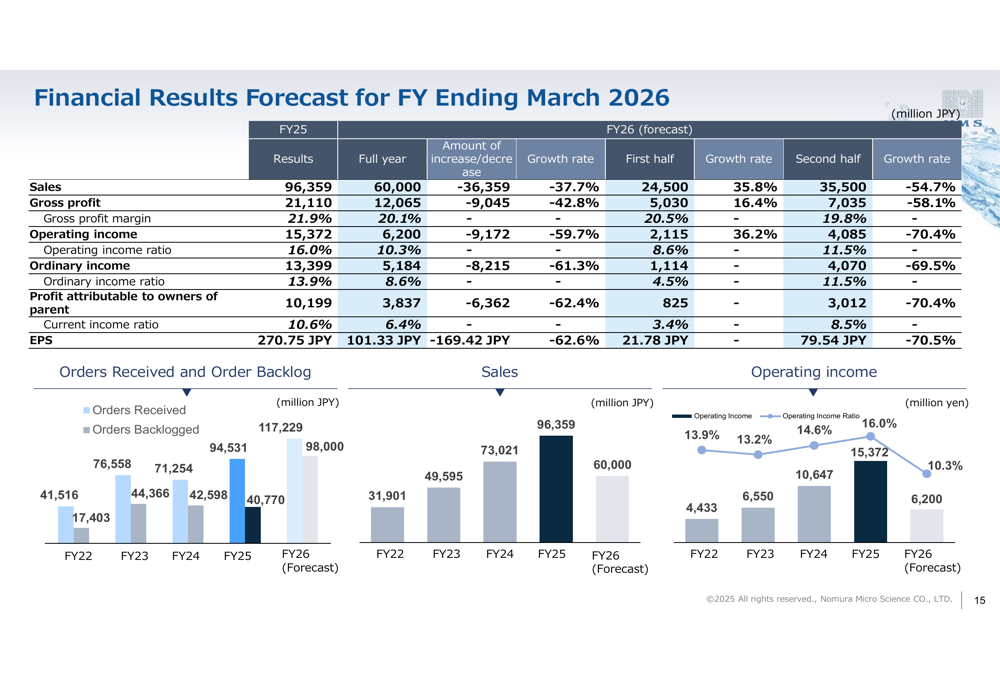

The company's profit and loss statement further illustrates this strong performance, with results exceeding both initial and revised plans:

Sales increased 32.0% to 96,359 million JPY, while operating income jumped 44.4% to 15,372 million JPY. The operating income ratio improved to 16.0%, up from 14.6% in the previous fiscal year. Ordinary income rose 23.9% to 13,399 million JPY, and profit attributable to owners of parent grew 27.8% to 10,199 million JPY.

Detailed Financial Analysis

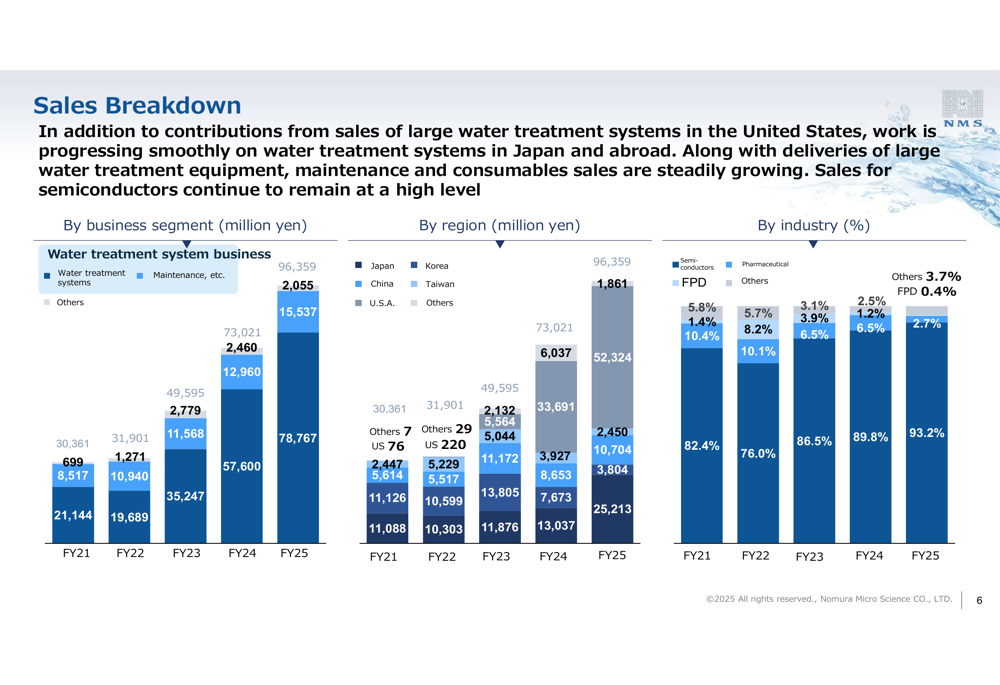

The company's business is heavily concentrated in the semiconductor industry, which accounted for 93.2% of sales in FY2025, up from 82.4% in FY2021. This increasing dependency on semiconductors highlights both the company's specialized expertise and its vulnerability to cyclical fluctuations in that sector.

Breaking down sales by business segment reveals the dominance of water treatment systems:

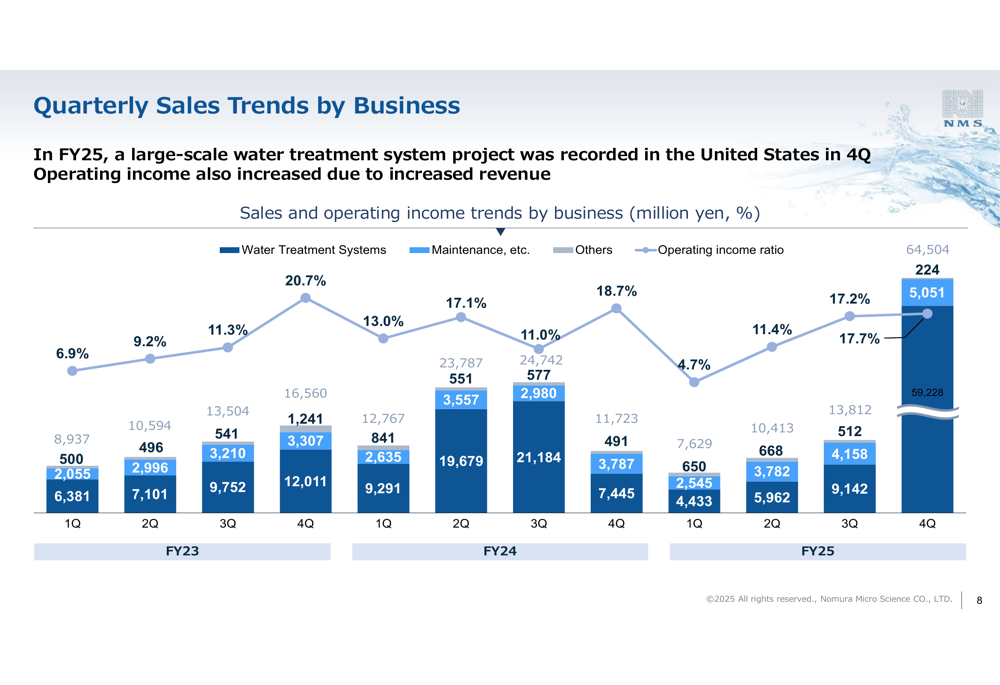

The quarterly sales trends show a significant spike in the fourth quarter of FY2025, particularly in the United States, where a large-scale water treatment system project was recorded:

The regional breakdown of orders received demonstrates the company's global reach, with notable new business in India (TATA project) and new customers in Korea recorded in Q4:

Forward-Looking Statements

Despite the record performance in FY2025, Nomura Micro Science forecasts a significant decline for FY2026, reflecting the cyclical nature of large project-based business:

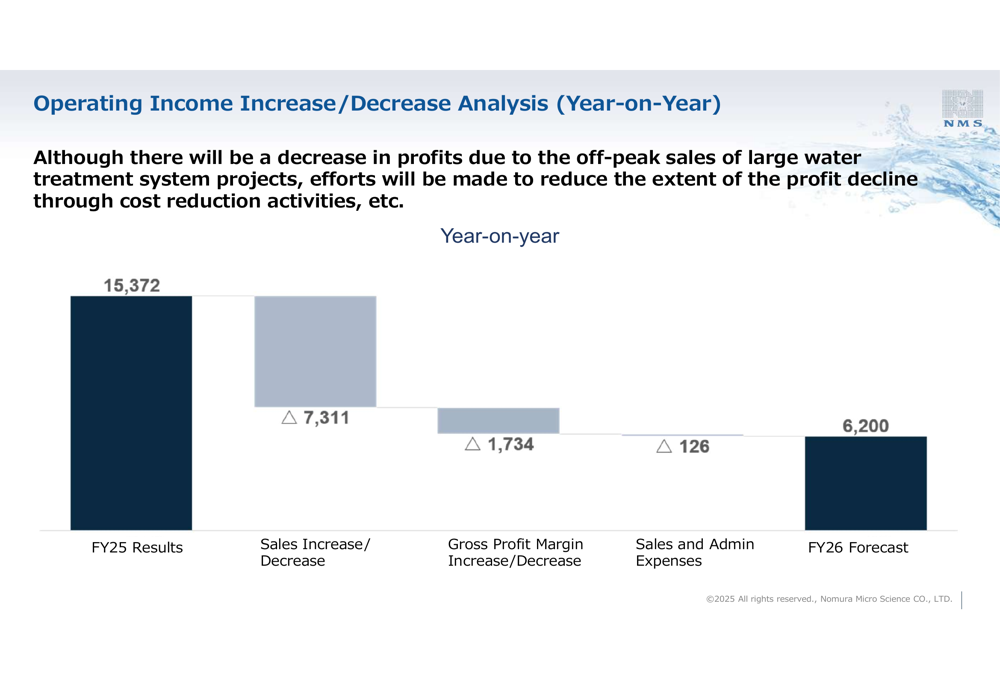

The company projects sales to decrease 37.7% to 60,000 million JPY and operating income to fall 59.7% to 6,200 million JPY. This substantial decline is attributed to the "off-peak sales of large water treatment system projects," though management notes they will "make efforts to reduce the extent of the profit decline through cost reduction activities."

The expected changes in operating income are analyzed in the following waterfall chart:

Strategic Initiatives

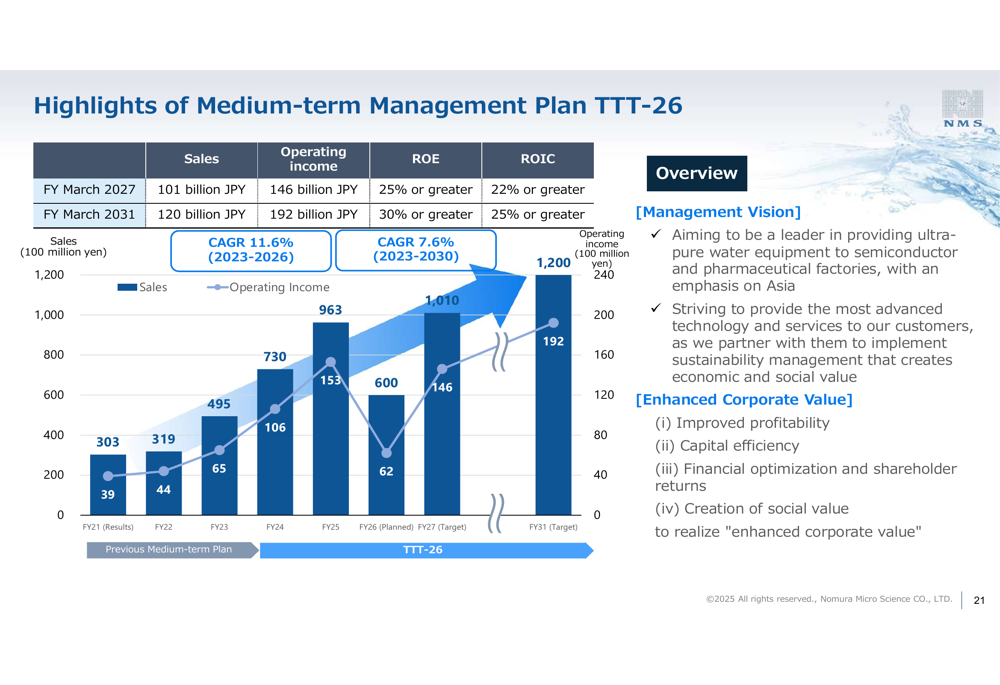

To navigate these cyclical challenges and drive long-term growth, Nomura Micro Science outlined its medium-term management plan "TTT-26" (Together Toward Transformation-26):

The plan focuses on enhancing corporate value through improved profitability, capital efficiency, financial optimization, and creation of social value. The company targets sales of 110 billion JPY and operating income of 16.5 billion JPY by FY March 2027.

Nomura Micro Science is implementing several strategic initiatives to achieve these goals:

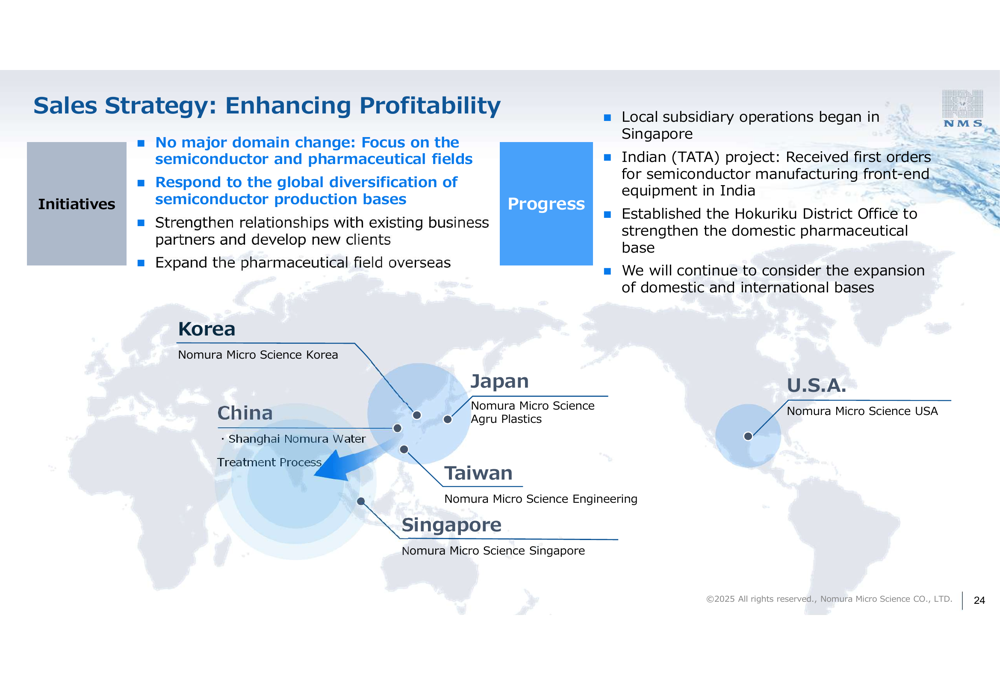

1. Global Sales Strategy: The company is expanding its geographical reach while focusing on enhancing profitability:

2. Engineering Process Reform: Implementation of equipment skid mounting and piping prefabrication to reduce on-site work and improve efficiency.

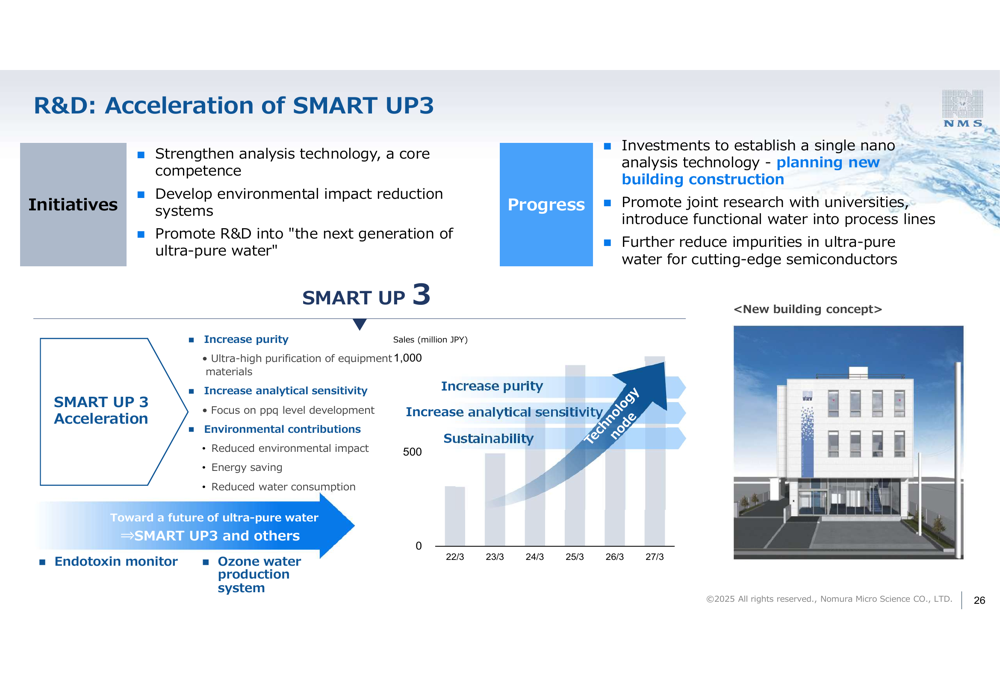

3. R&D Acceleration: The company is advancing its SMART UP3 program, focusing on strengthening analysis technology, developing environmental impact reduction systems, and promoting next-generation ultra-pure water research:

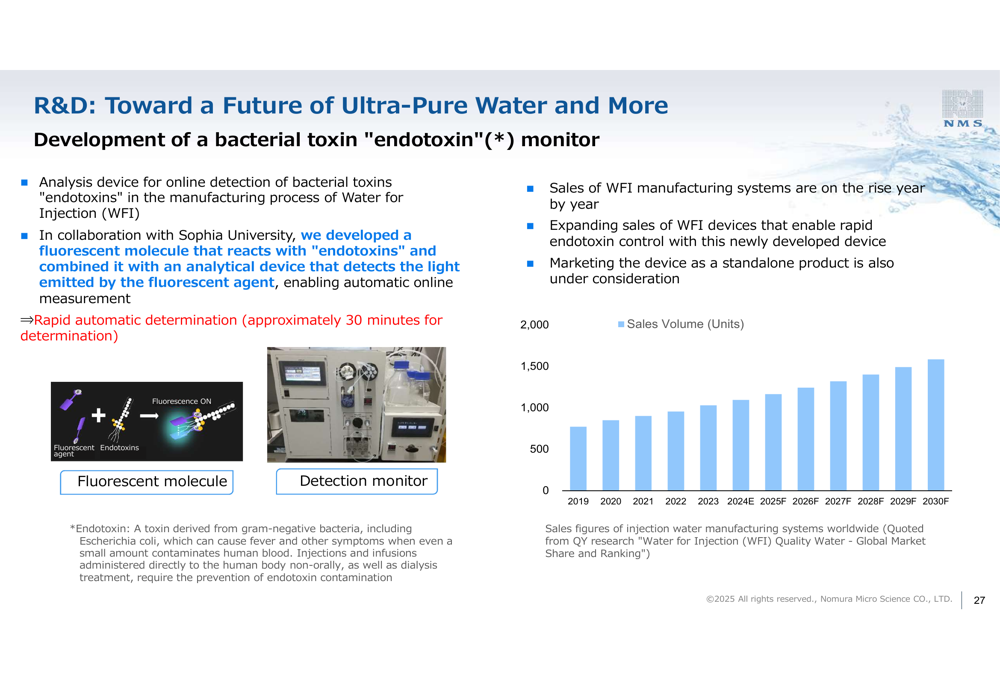

4. Innovation in Water for Injection: Development of a bacterial toxin "endotoxin" monitor for pharmaceutical applications, with sales of WFI manufacturing systems increasing year by year:

Shareholder Returns

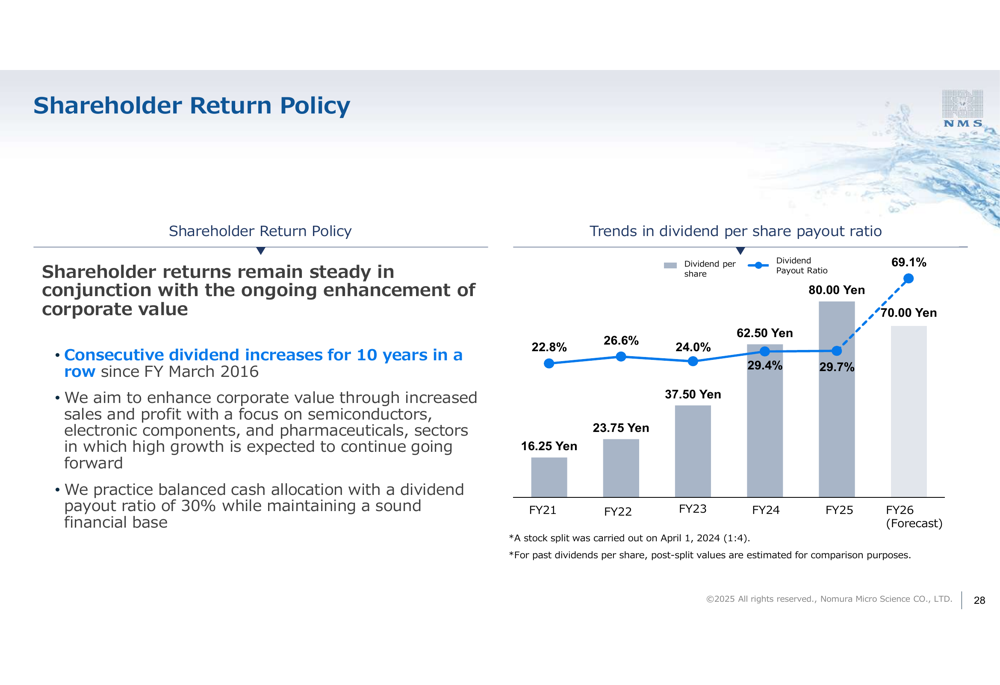

Despite the projected decline in FY2026 performance, Nomura Micro Science remains committed to its shareholder return policy, having achieved consecutive dividend increases for 10 years:

The company aims to balance shareholder returns with ongoing enhancement of corporate value, maintaining its track record of increasing dividends even as it navigates the upcoming challenging fiscal year.

In conclusion, while Nomura Micro Science achieved record results in FY2025, investors should prepare for a significant decline in FY2026 as the company moves through its project cycle. The medium-term outlook remains positive, supported by semiconductor industry growth and the company's strategic initiatives under its TTT-26 plan.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.