S&P 500 jumps as AMD rally leads tech higher

Introduction & Market Context

Open Lending Corp (NASDAQ:LPRO) released its Q1 2025 earnings presentation on May 7, showing signs of stabilization following a disastrous Q4 2024 that saw the company report a significant earnings miss. The automotive lending solutions provider’s stock closed at $1.36 before the earnings release and rose 3.23% in after-hours trading to $1.60, suggesting cautious optimism from investors despite continued year-over-year declines in key metrics.

The Q1 results come after a tumultuous Q4 2024 when Open Lending reported a staggering negative revenue of $56.9 billion and an EPS of -$1.21, which sent the stock plummeting. While the latest quarter shows sequential improvement, the company continues to face headwinds in its profit share revenue stream and overall profitability compared to the same period last year.

Quarterly Performance Highlights

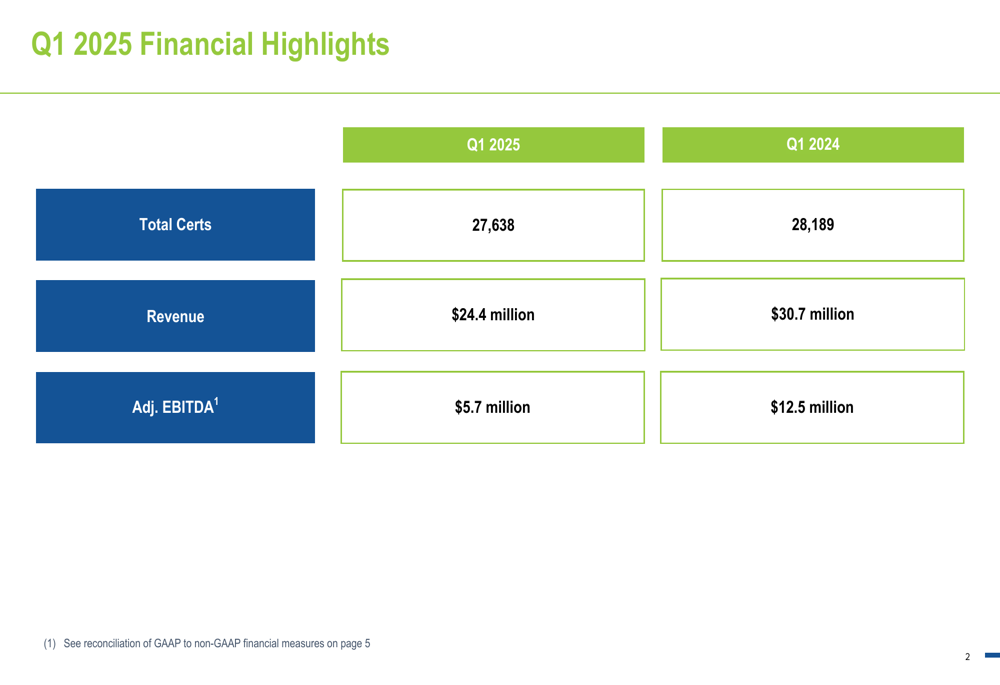

Open Lending’s Q1 2025 financial results revealed a mixed performance with total certifications (certs) reaching 27,638, slightly down from 28,189 in Q1 2024. Revenue came in at $24.4 million, representing a 20.7% decline from $30.7 million in the same quarter last year. Adjusted EBITDA saw an even steeper drop, falling 54.9% year-over-year to $5.7 million from $12.5 million.

As shown in the company’s financial highlights:

The decline in revenue and profitability occurred despite the total number of certifications remaining relatively stable year-over-year. This points to challenges in the company’s unit economics, particularly in its profit share revenue model, which has been a significant contributor to earnings volatility.

Detailed Financial Analysis

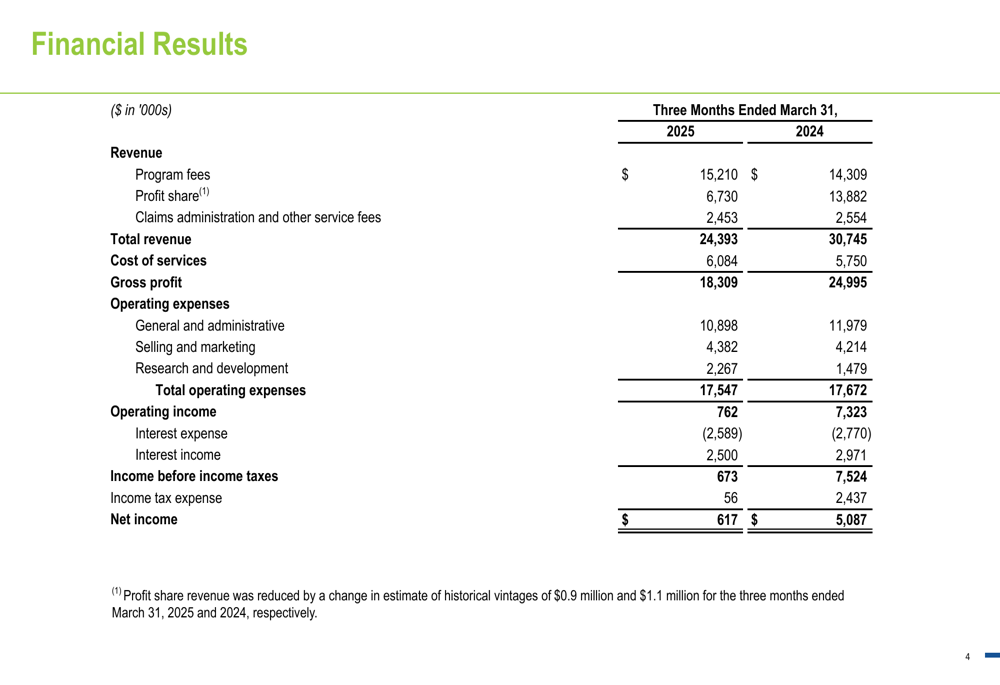

A deeper look into Open Lending’s financial results reveals the primary drivers behind the company’s performance challenges. The most notable issue continues to be the dramatic decline in profit share revenue, which fell to $6.73 million in Q1 2025 from $13.88 million in Q1 2024 – a 51.5% decrease. This was partially offset by a modest 6.3% increase in program fees to $15.21 million.

The detailed breakdown of the company’s financial performance shows:

The sharp decline in profit share revenue has significantly impacted Open Lending’s bottom line, with net income falling 87.9% year-over-year to just $617,000 in Q1 2025 from $5.09 million in Q1 2024. Operating income showed a similar trend, declining 89.6% to $762,000.

On a positive note, the company managed to slightly reduce its total operating expenses to $17.55 million from $17.67 million in the prior year period, with notable decreases in general and administrative expenses. However, research and development costs increased by 53.3% to $2.27 million, suggesting continued investment in technology and product development despite financial pressures.

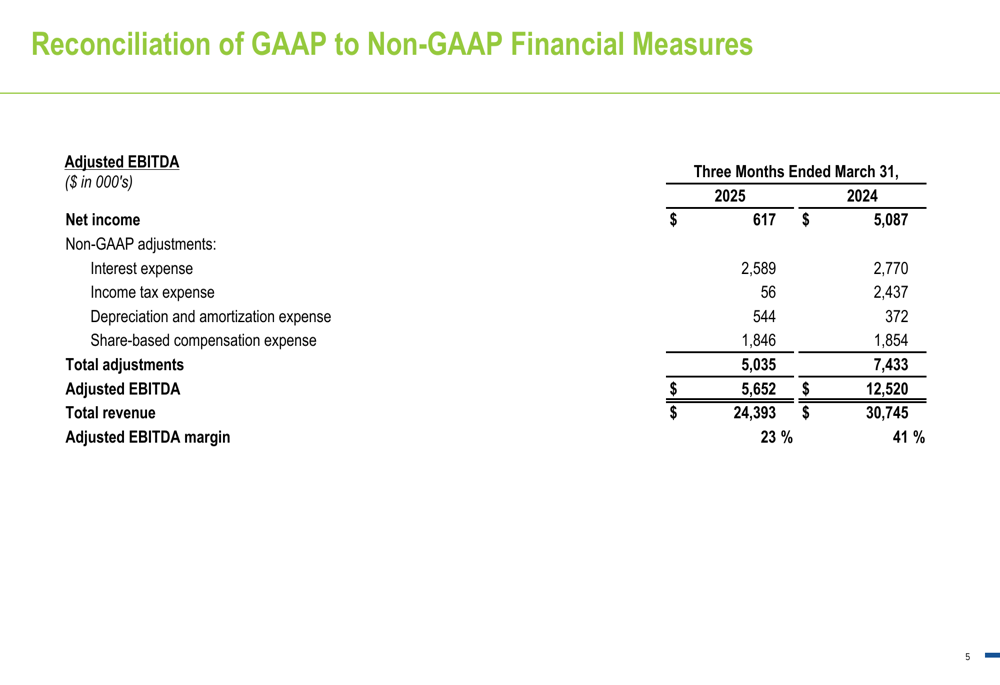

The reconciliation of GAAP to non-GAAP measures provides further insight into the company’s adjusted performance:

The adjusted EBITDA margin contracted significantly to 23% in Q1 2025 from 41% in Q1 2024, reflecting the challenges in maintaining profitability amid declining profit share revenue.

Strategic Initiatives & Business Mix

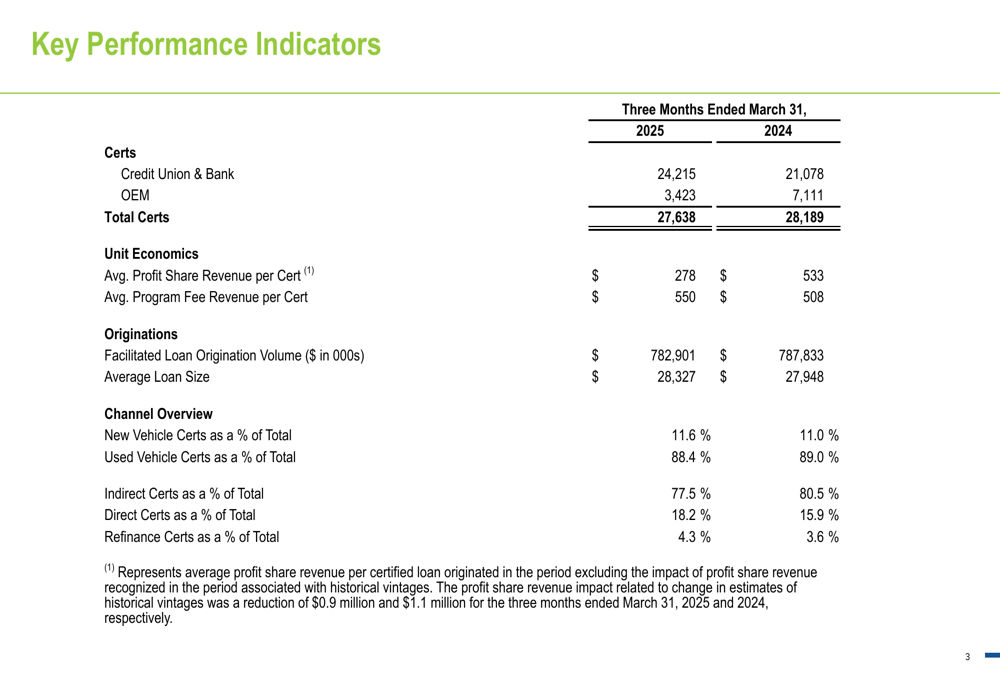

Open Lending’s Q1 2025 results indicate a strategic shift in its business mix, with a notable increase in certifications from credit unions and banks, which rose to 24,215 from 21,078 in Q1 2024. This growth was offset by a sharp decline in OEM certifications, which fell to 3,423 from 7,111 in the prior year period.

The company’s key performance indicators reveal these changing dynamics:

The data shows Open Lending is pivoting toward direct and refinance channels, which increased as a percentage of total certifications to 18.2% and 4.3% respectively, up from 15.9% and 3.6% in Q1 2024. Meanwhile, indirect certifications declined to 77.5% of the total from 80.5% a year earlier.

Another concerning trend is the significant drop in average profit share revenue per certification, which fell to $278 in Q1 2025 from $533 in Q1 2024 – a 47.8% decrease. This decline was partially offset by a 8.3% increase in average program fee revenue per certification to $550.

Forward-Looking Statements

While Open Lending’s Q1 2025 presentation doesn’t explicitly provide forward guidance, the company’s performance suggests it is working to stabilize its business following the significant challenges faced in Q4 2024. The shift toward credit unions and banks, along with increased focus on direct and refinance channels, indicates a strategic realignment to reduce dependence on OEM partnerships and potentially stabilize profit share revenue.

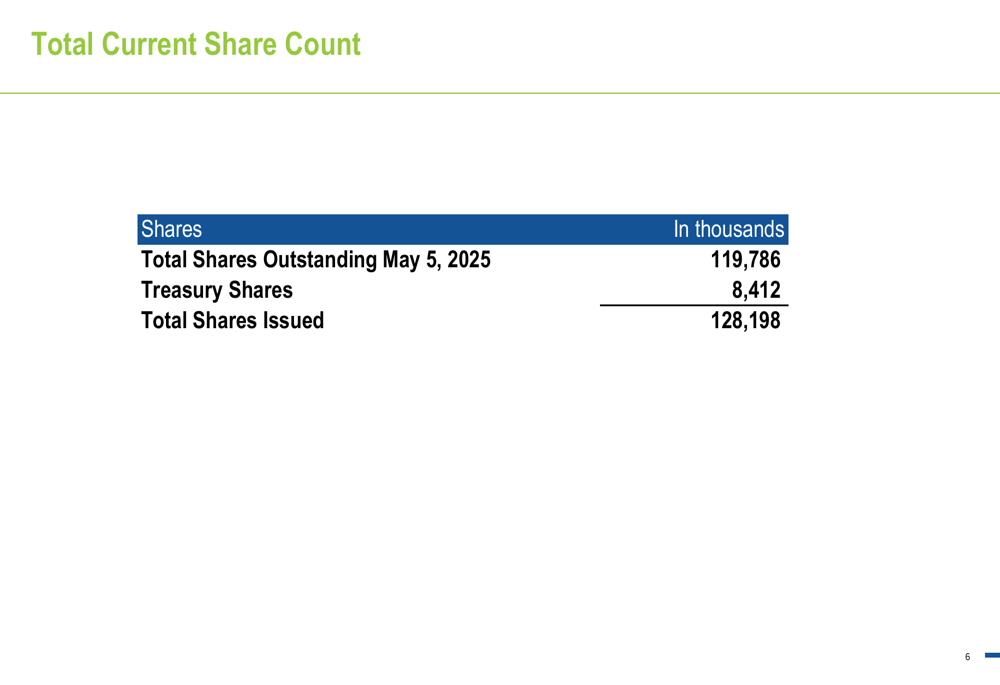

The company’s share count as of May 5, 2025, stands at approximately 119.8 million outstanding shares, with 8.4 million treasury shares:

Looking ahead, investors will likely focus on whether Open Lending can reverse the declining trend in profit share revenue and improve its unit economics. The increased investment in research and development suggests the company may be developing new solutions to address these challenges, potentially including the "more sophisticated real-time pricing model" mentioned in previous communications to reduce volatility in profit share revenue.

Given the company’s recent history of earnings volatility and the continued year-over-year declines in key metrics, Open Lending faces significant challenges in rebuilding investor confidence. However, the sequential improvement from Q4 2024 and the modest after-hours stock price increase suggest the market sees potential for recovery if the company can successfully execute its strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.