Procore signs multi-year strategic collaboration agreement with AWS

Penn Entertainment (NASDAQ:PENN) presented its first quarter 2025 earnings results on May 8, highlighting significant year-over-year improvements in its interactive segment and resilience in its retail business. The company’s stock was down 2.99% in premarket trading to $15.24, reflecting continued market skepticism despite operational improvements.

Quarterly Performance Highlights

Penn Entertainment’s retail segment demonstrated resilience in Q1 2025, with gaming volumes rebounding in March after weather-related challenges earlier in the year. The company reported that these positive trends continued through April and early May. Meanwhile, the interactive segment generated record gaming revenue with significant year-over-year improvements in both adjusted revenue and adjusted EBITDA.

The company also reported that it has repurchased $35 million of shares year-to-date and remains committed to its previously stated goal of repurchasing at least $350 million of shares in 2025.

Interactive Segment Progress

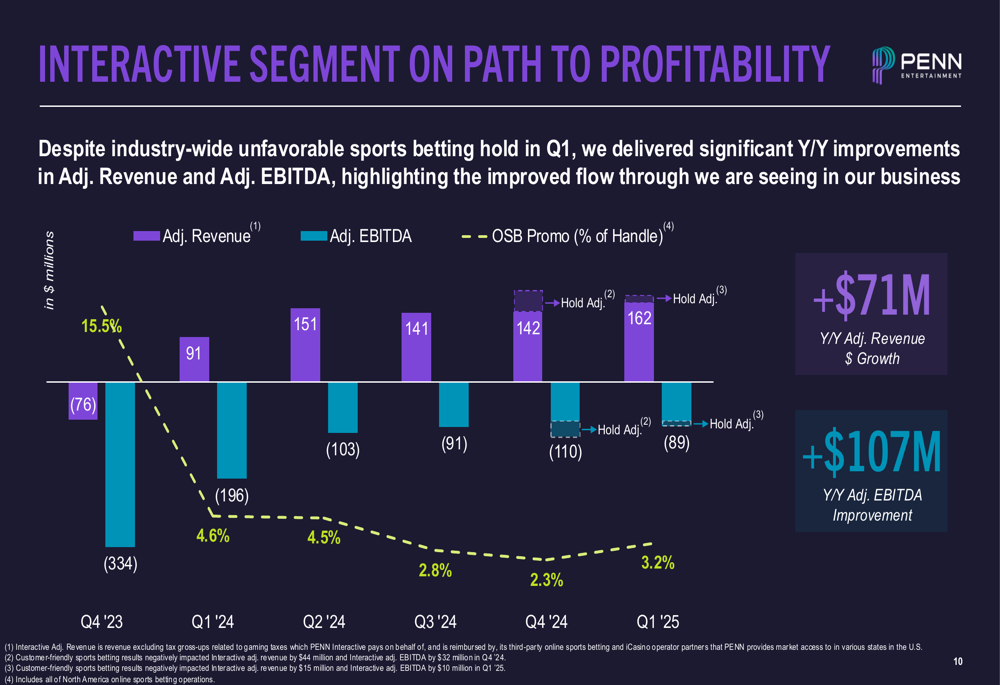

The interactive segment showed substantial progress toward profitability, with adjusted revenue improving from -$196 million in Q1 2024 to $91 million in Q1 2025, representing a $71 million year-over-year improvement. More importantly, adjusted EBITDA improved by $107 million year-over-year, from -$103 million to $162 million, despite industry-wide unfavorable sports betting hold in Q1.

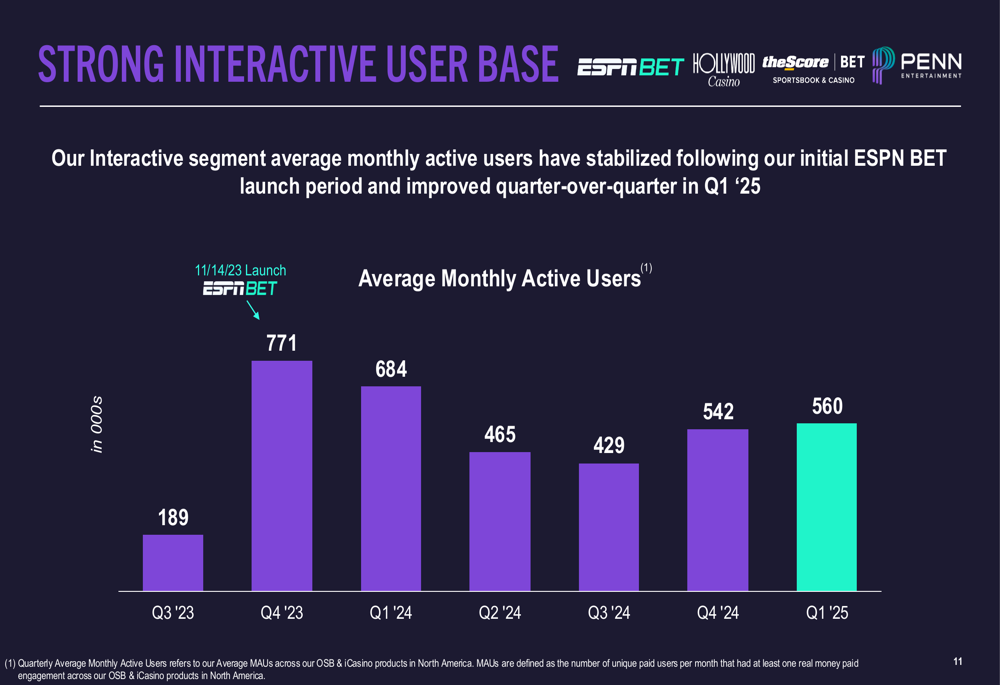

The average monthly active users for Penn’s interactive segment stabilized at 560,000 in Q1 2025, up from 542,000 in Q4 2024, following the initial surge after the ESPN BET launch.

This performance marks a significant turnaround from the company’s Q4 2024 results, which showed an EPS of -$0.44 that missed analyst expectations of -$0.29, with the interactive segment reporting a notable EBITDA loss at that time.

Retail Business Resilience

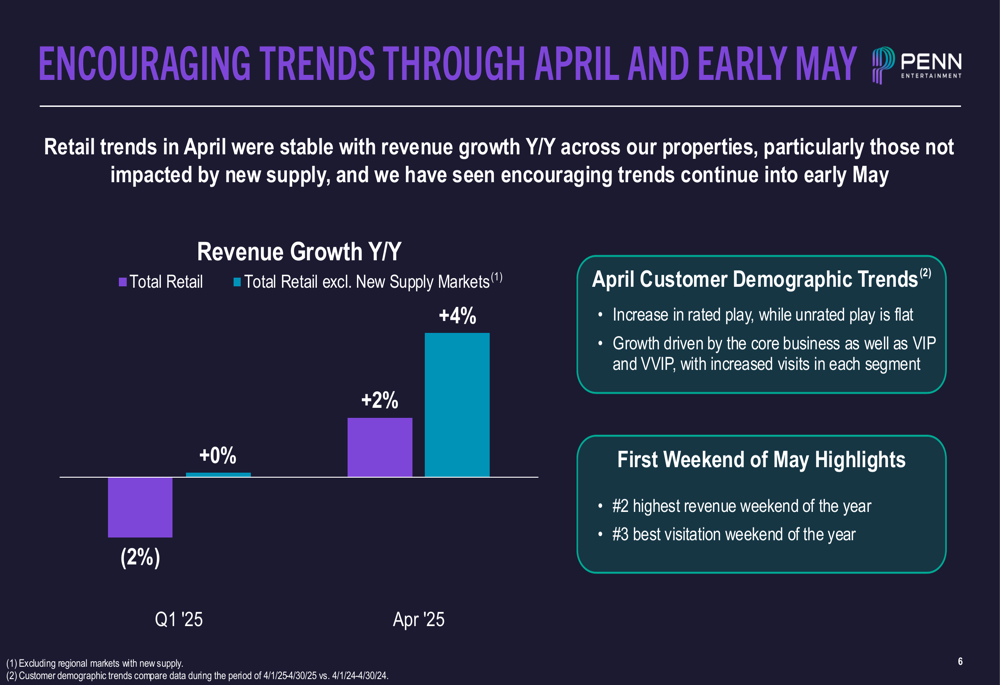

Penn’s retail business showed encouraging trends through April and early May, with total retail revenue growth of 2% year-over-year when excluding new supply markets. The company noted increased rated play in April, with growth driven by core business as well as VIP and VVIP segments.

The company is investing in its retail portfolio with several development projects. A key initiative is the landside relocation of Ameristar Council Bluffs in Iowa, which will be rebranded as Hollywood. The project has an estimated budget of $180-200 million, with Gaming and Leisure Properties, Inc. (NASDAQ:GLPI) providing funding of up to $150 million at a 7.10% cap rate. Construction is expected to take approximately 18-24 months.

Additional development projects on track include the Hollywood Joliet Relocation (Q4 2025), Hollywood Columbus (WA:CLC) Hotel Tower (1H 2026), Hollywood Aurora Relocation (1H 2026), and M Resort Hotel Tower (1H 2026).

iCasino Growth and Omni-Channel Strategy

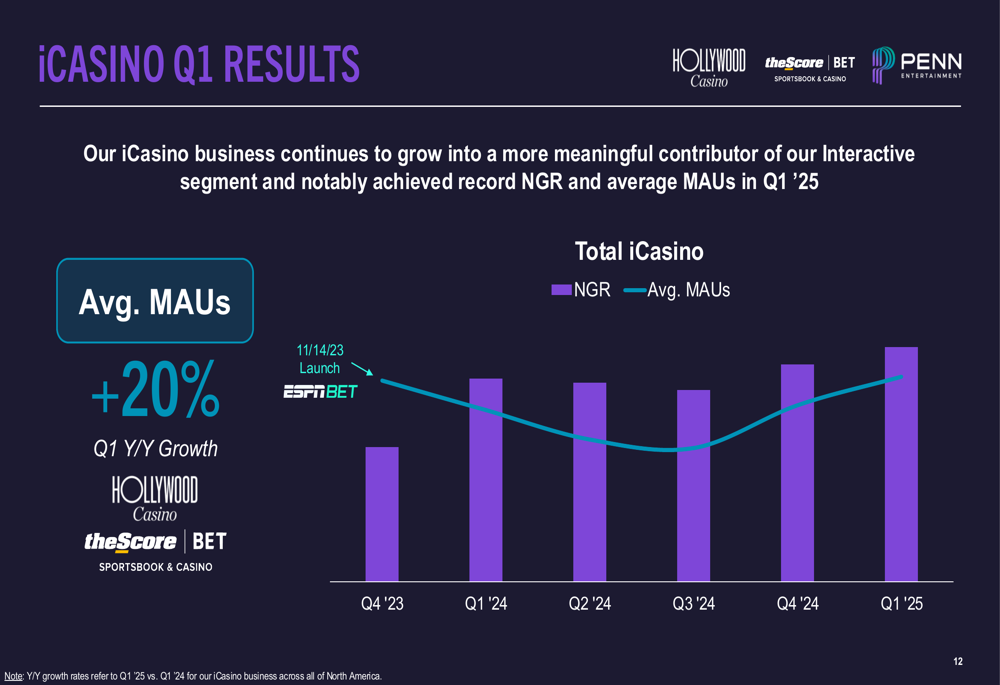

Penn’s iCasino business continues to show strong momentum, achieving record Net Gaming Revenue (NGR) and average Monthly Active Users (MAUs) in Q1 2025, with a 20% year-over-year growth in average MAUs.

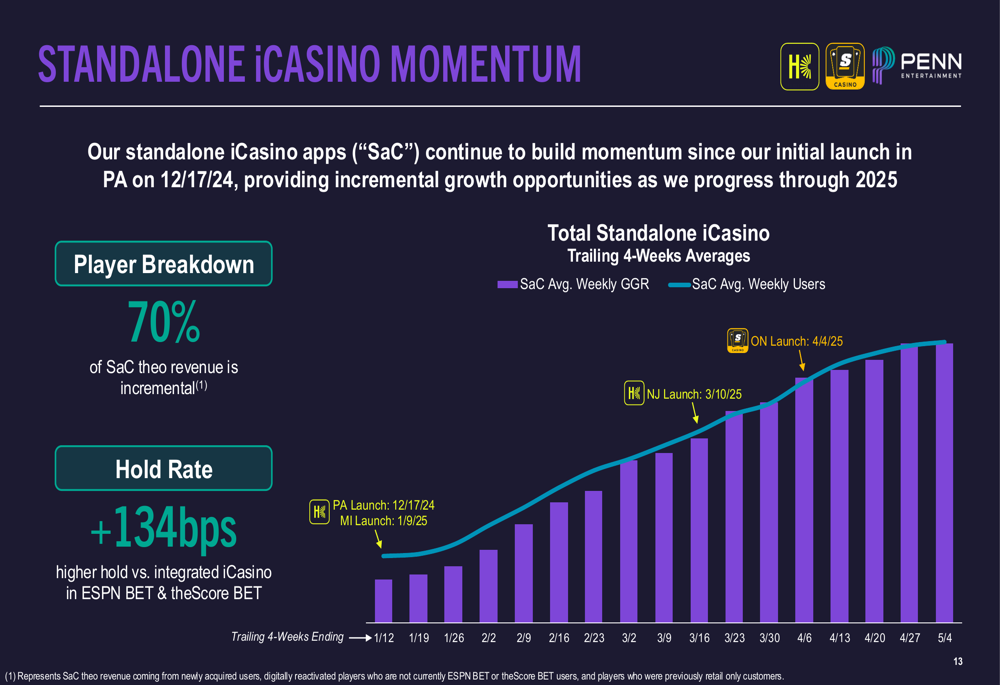

The company’s standalone iCasino apps are building momentum following launches in Pennsylvania, Michigan, New Jersey, and Ontario. Penn reported that 70% of standalone iCasino theoretical revenue is incremental, with a hold rate 134 basis points higher versus integrated iCasino in ESPN BET and theScore BET.

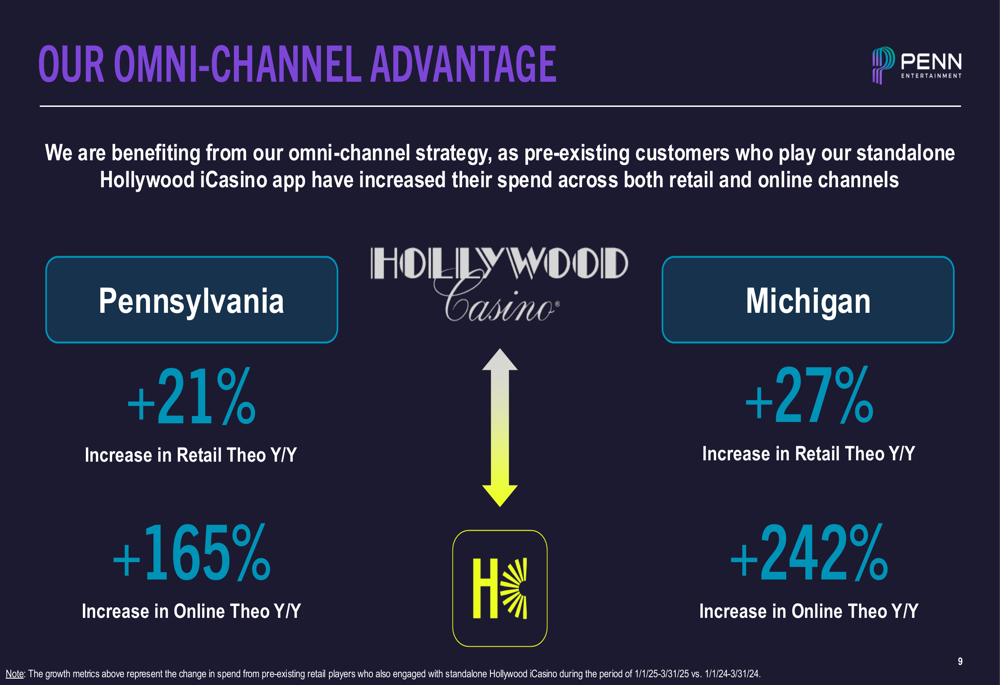

Penn’s omni-channel strategy is showing promising results, with pre-existing customers who play the standalone Hollywood iCasino app increasing their spend across both retail and online channels. In Pennsylvania, these customers increased their retail theoretical win by 21% and online theoretical win by 165%, while in Michigan, the increases were 27% and 242% respectively.

Forward-Looking Statements

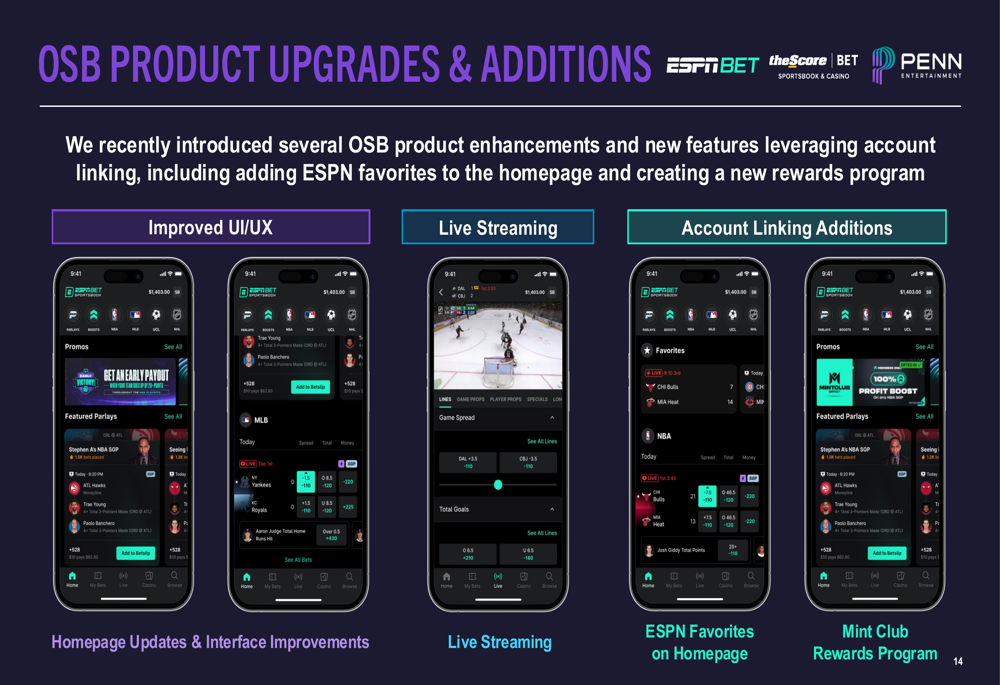

Penn Entertainment continues to focus on its path to profitability for the interactive segment while investing in its retail properties to maintain competitiveness. The company recently introduced several online sports betting product enhancements, including improved UI/UX, live streaming, account linking additions, and the Mint Club rewards program.

These developments come as Penn navigates a challenging market environment. The company’s stock has declined from around $20 in the previous quarter to $15.71 at the last close before the earnings presentation, suggesting continued market skepticism despite the operational improvements highlighted in the Q1 2025 presentation.

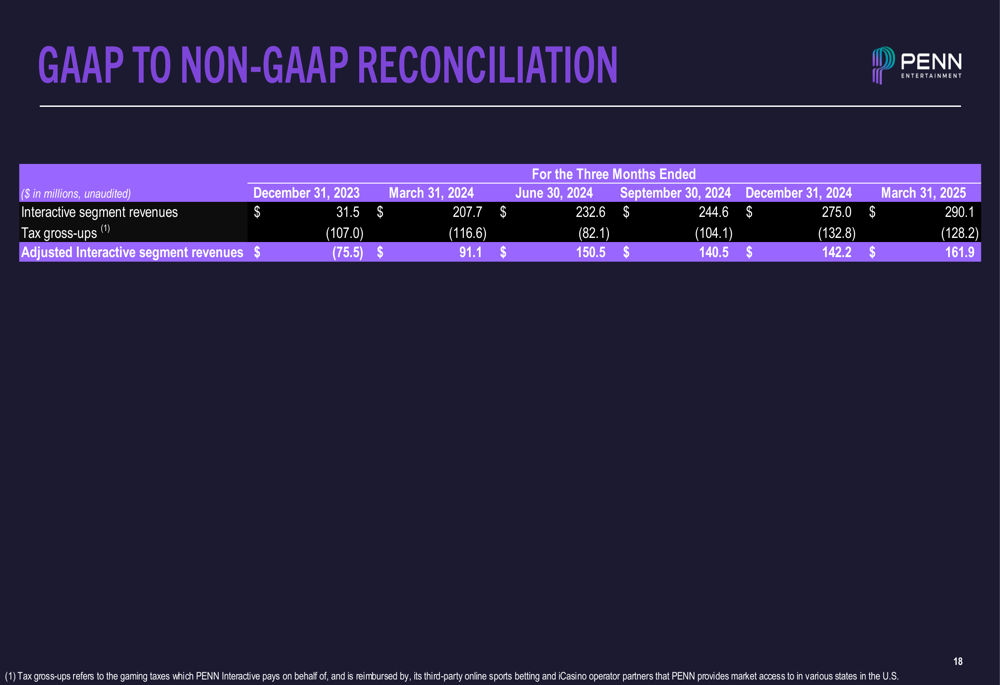

The reconciliation of GAAP to non-GAAP measures shows the company’s progress in improving its interactive segment’s financial performance, with adjusted interactive segment revenues improving from $91.1 million in Q1 2024 to $161.9 million in Q1 2025.

As Penn Entertainment continues its multi-year growth strategy, investors will be watching closely to see if the operational improvements highlighted in this presentation translate into sustainable profitability and stock price recovery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.