Gold prices edge higher with focus on Ukraine-Russia, Jackson Hole

Introduction & Market Context

Postal Realty Trust (NYSE:PSTL), a REIT focused on properties leased to the United States Postal Service, presented its latest investor deck in August 2025, highlighting its unique position in a fragmented market and strong financial trajectory. The company’s stock closed at $13.70 on August 4, 2025, up 1.97% for the day, according to market data.

The presentation emphasizes PSTL’s role in "investing in America’s logistics network" through its portfolio of postal properties, positioning the USPS as a critical infrastructure provider supporting e-commerce and last-mile delivery operations. With Amazon (NASDAQ:AMZN), UPS, FedEx (NYSE:FDX), and DHL all utilizing the USPS logistics network daily, PSTL frames its real estate holdings as essential to modern commerce.

Growth Strategy & Market Opportunity (SO:FTCE11B)

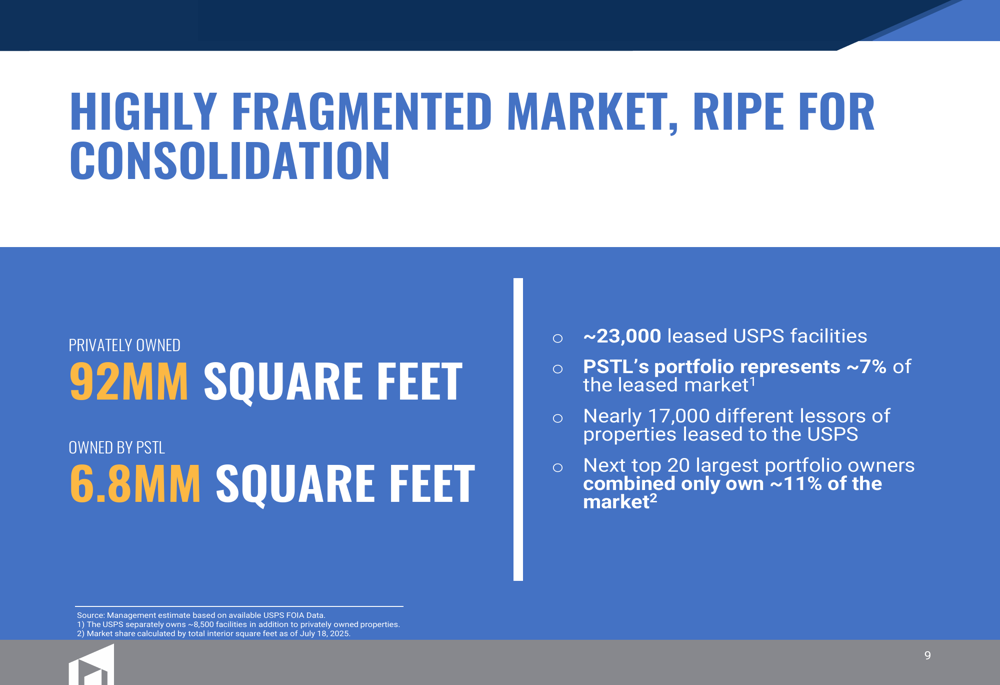

A central theme of the presentation is the highly fragmented nature of the USPS real estate market, which PSTL views as a significant growth opportunity. According to the company, there are approximately 23,000 leased USPS facilities nationwide, with nearly 17,000 different lessors.

PSTL currently owns about 7% of this leased market, while the next 20 largest portfolio owners combined control only about 11%. This fragmentation creates a substantial consolidation opportunity that the company is actively pursuing through its acquisition strategy.

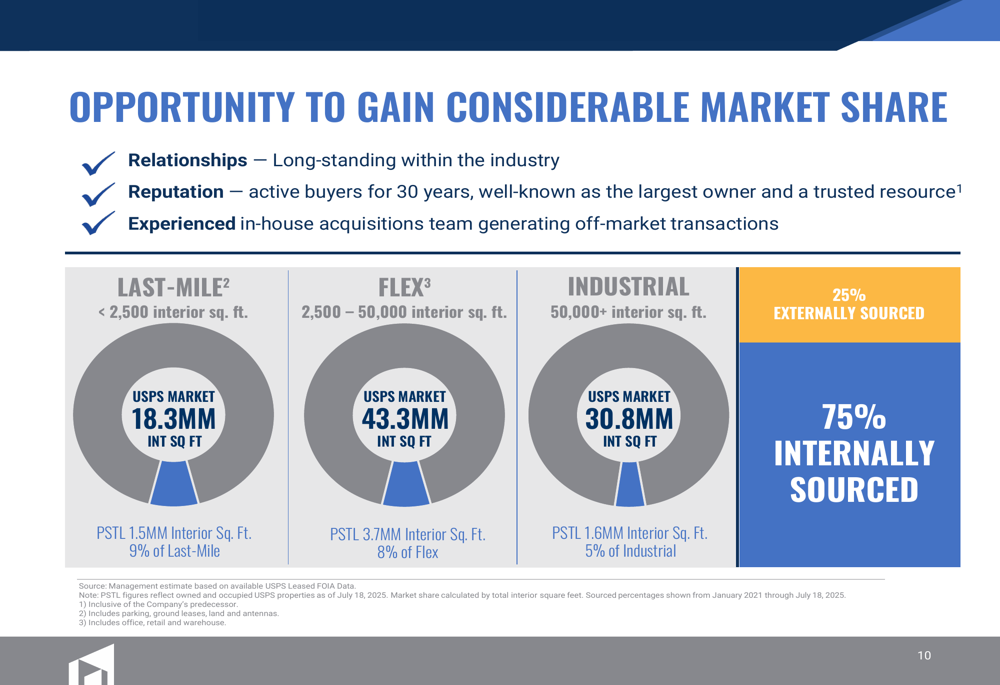

The company has developed a multi-pronged approach to capturing market share across three property categories: Last-Mile (under 2,500 sq ft), Flex (NASDAQ:FLEX) (2,500-50,000 sq ft), and Industrial (over 50,000 sq ft).

Financial Performance Highlights

The presentation showcases PSTL’s consistent financial growth since its IPO. The company reports impressive same-store cash NOI growth of 5.5% in 2023 and 4.4% in 2024, with projections of 7-9% for 2025. This acceleration in NOI growth represents a significant improvement in the company’s operating performance.

AFFO per share has shown steady improvement, increasing from $1.00 in 2020 to a projected $1.24-$1.26 for 2025. This represents a compound annual growth rate of approximately 4.5% over this period. The company’s quarterly dividend has grown by 73% since Q3 2019, reaching $0.2425 per share in Q1 2025, while maintaining an attractive yield of 6.7%.

The company’s acquisition strategy has been a key driver of growth, with annual acquisition volume ranging from $18 million to $57 million between 2020 and 2025. For 2025, the guidance indicates $48 million in acquisitions at a weighted average capitalization rate of 7.7%.

Portfolio Optimization

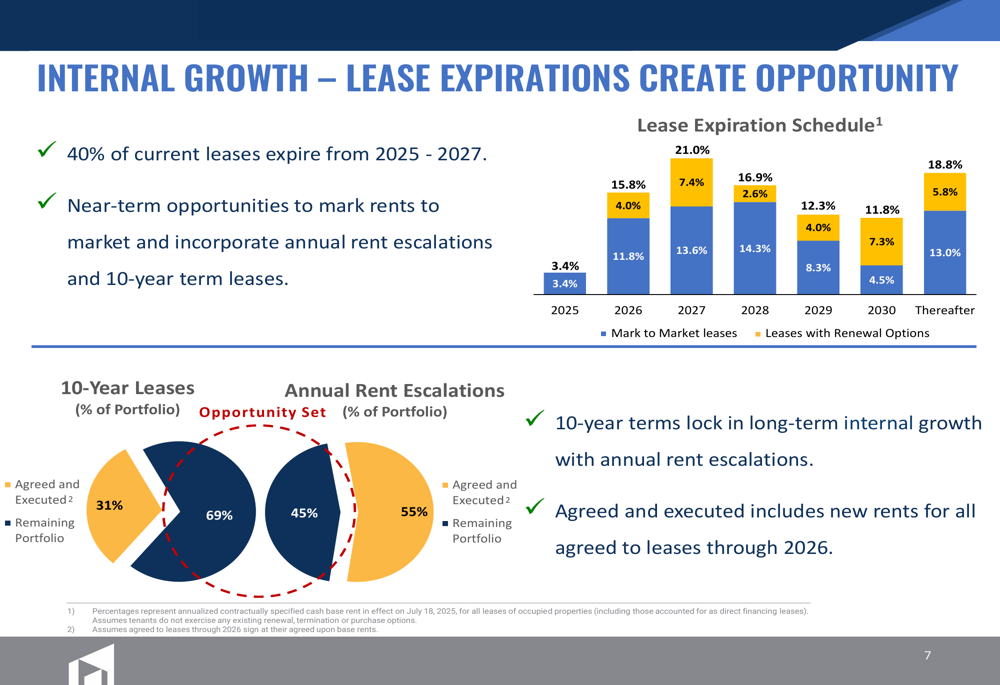

Beyond acquisitions, PSTL is focusing on internal growth through lease renewals and rent escalations. The company notes that 40% of its current leases expire from 2025-2027, creating near-term opportunities to mark rents to market and incorporate annual rent escalations into new 10-year term leases.

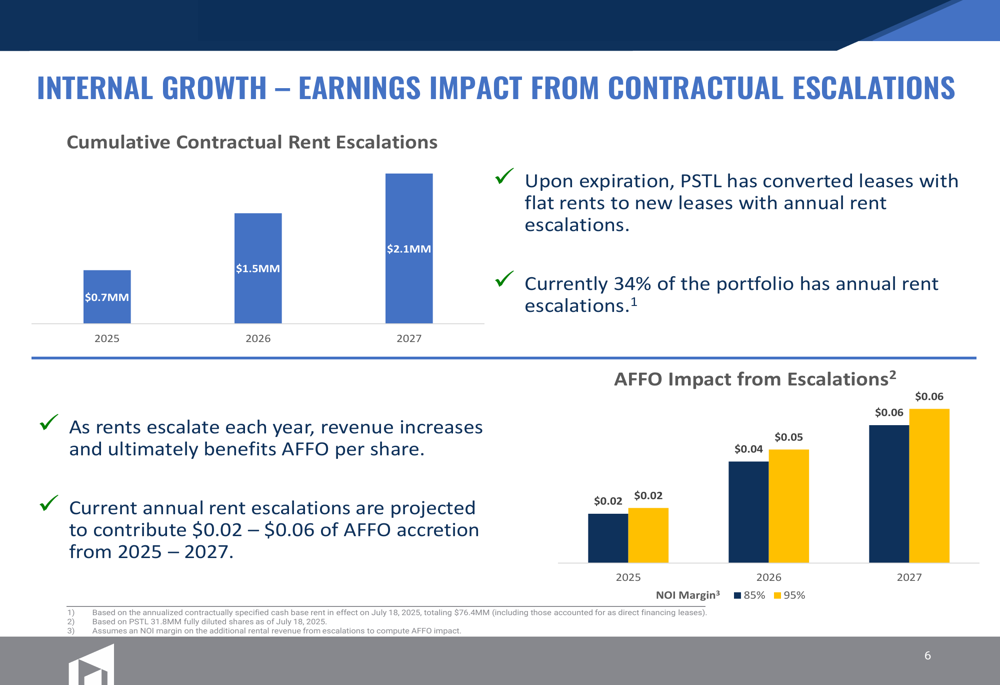

The company projects significant earnings impact from these contractual escalations, with cumulative rent increases of $0.7 million in 2025, $1.5 million in 2026, and $2.1 million in 2027. This is expected to translate to AFFO impact of $0.02, $0.04, and $0.06 per share in those respective years.

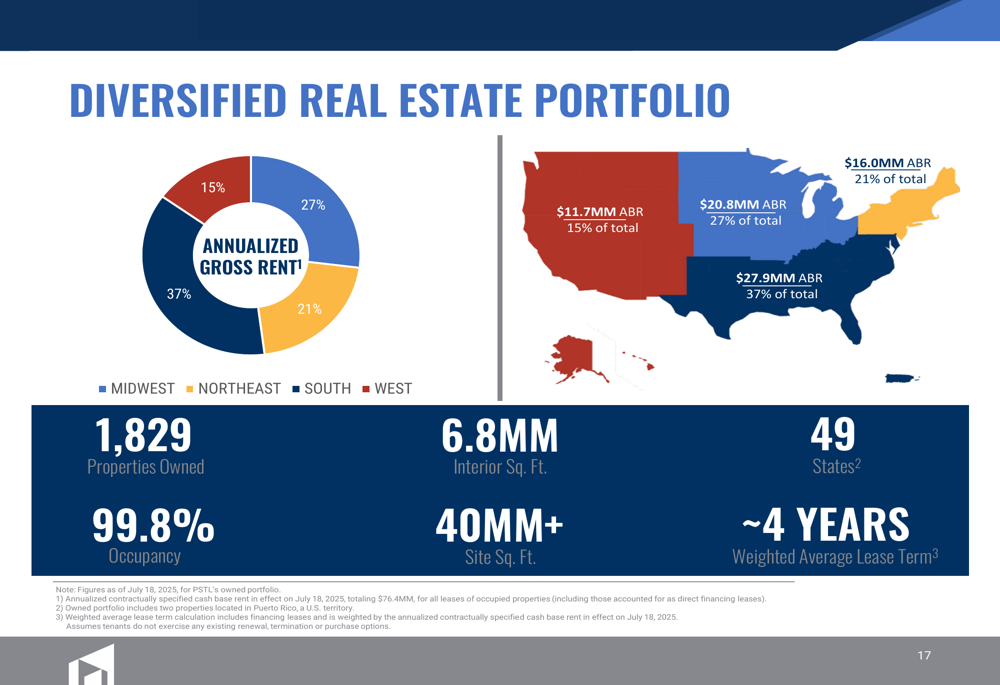

PSTL’s portfolio remains well-diversified geographically, with properties in 49 states maintaining a remarkable 99.8% occupancy rate. The portfolio is distributed across the Midwest (37% of annualized gross rent), South (27%), West (21%), and Northeast (15%).

Balance Sheet & Capital Structure

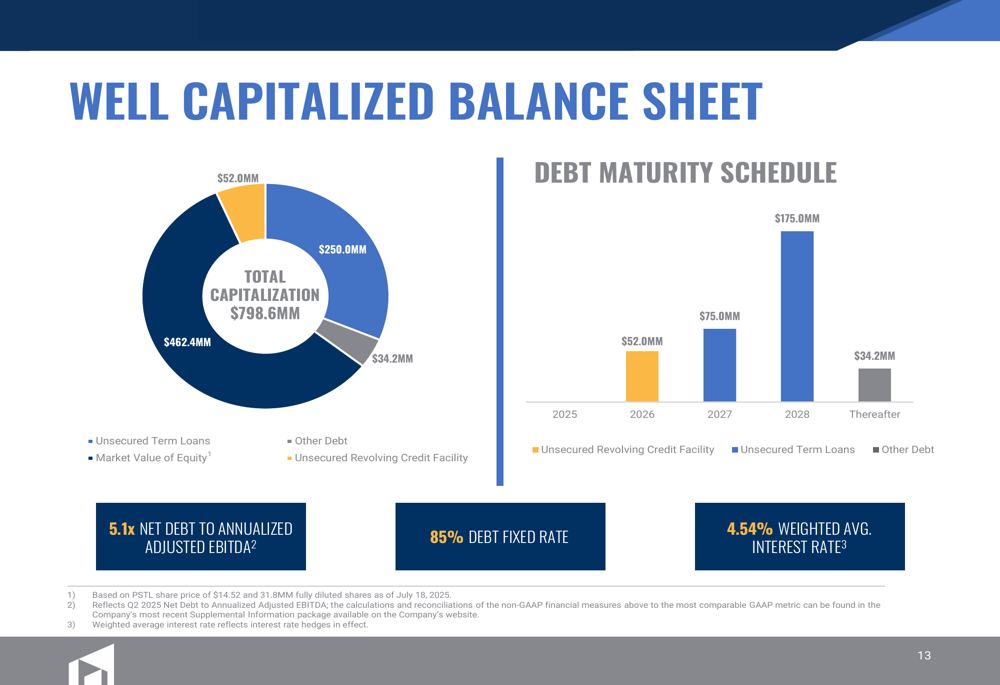

The presentation highlights PSTL’s well-capitalized balance sheet with a total capitalization of $798.6 million. The capital structure consists of $462.4 million in market value of equity, $250.0 million in unsecured term loans, $52.0 million in unsecured revolving credit facility, and $34.2 million in other debt.

Key financial metrics include a net debt to annualized adjusted EBITDA ratio of 5.1x, with 85% of debt at fixed rates and a weighted average interest rate of 4.54%. The debt maturity schedule is well-laddered, with no significant maturities until 2026.

Forward Outlook

Looking ahead, PSTL appears well-positioned to continue its growth trajectory through both acquisitions and internal growth drivers. The company’s strategy of consolidating the fragmented USPS property market while optimizing its existing portfolio through lease renewals and rent escalations provides multiple avenues for growth.

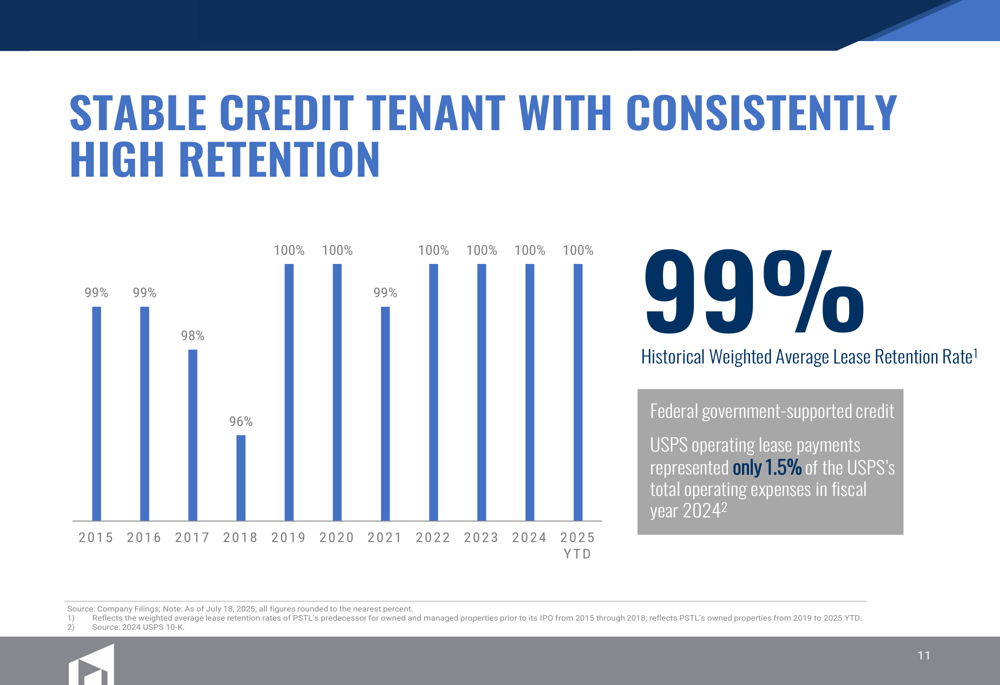

The stability of the USPS as a tenant is a key factor in PSTL’s investment thesis. The presentation emphasizes the consistently high retention rate, which has ranged from 96% to 100% since 2015 and stands at 99% for YTD 2025.

In its Q1 2025 earnings call, CEO Andrew Spodek emphasized the company’s strategic positioning, stating, "We very much view this as critical American infrastructure that we’re investing in." He highlighted the company’s high occupancy rate and visibility into future leasing activities.

However, investors should note some discrepancies between the August presentation and earlier guidance. The presentation projects AFFO of $1.24-$1.26 per share for 2025, while the Q1 earnings report mentioned guidance of $1.20-$1.22. Similarly, the presentation indicates $48 million in acquisitions for 2025, whereas the Q1 report anticipated $80-90 million. These differences suggest potential adjustments to the company’s outlook during the year.

With its focused strategy, stable tenant base, and multiple growth drivers, PSTL continues to position itself as a unique player in the REIT sector, offering investors exposure to the essential logistics infrastructure supporting e-commerce and last-mile delivery.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.