MicroVision MOVIA lidar gains support on NVIDIA DRIVE AGX platform

Introduction & Market Context

S4 Capital PLC (LSE:SFOR) released its Q1 2025 Trading Update on May 8, showing significant revenue declines across all business segments and geographies. Despite the challenging start to the year, the company maintained its full-year guidance, pinning hopes on a stronger second half. The stock traded down 1.24% following the presentation, reflecting investor concerns about the company’s near-term growth trajectory.

The digital advertising and marketing services company reported that market conditions remain difficult, with technology clients prioritizing capital expenditures over marketing spend, economic uncertainty heightened by tariffs, and advertising forecasts being downgraded across the industry.

Quarterly Performance Highlights

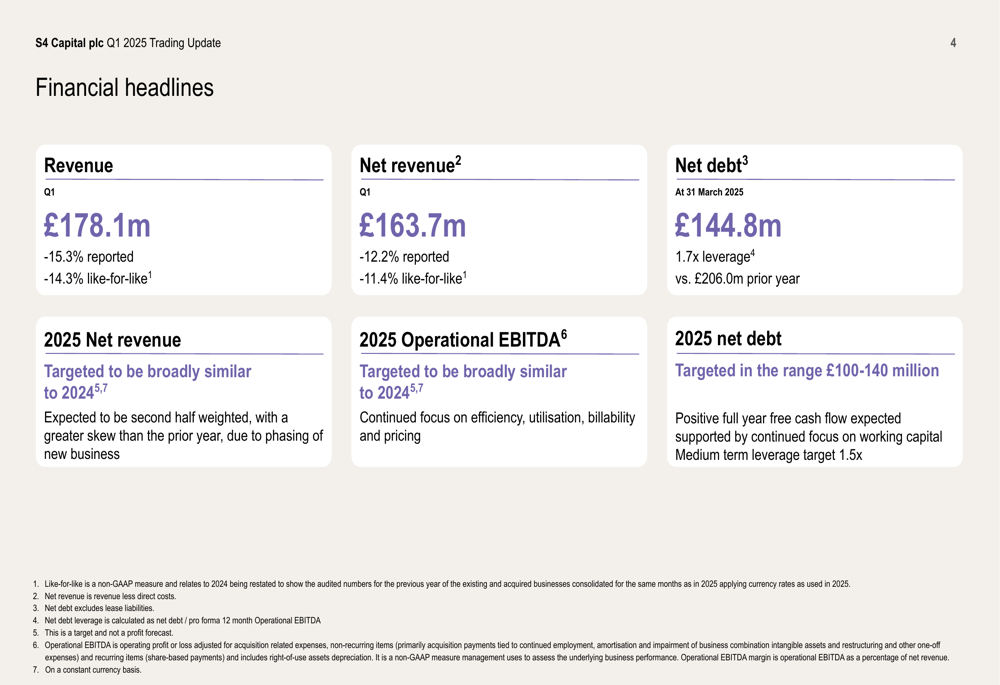

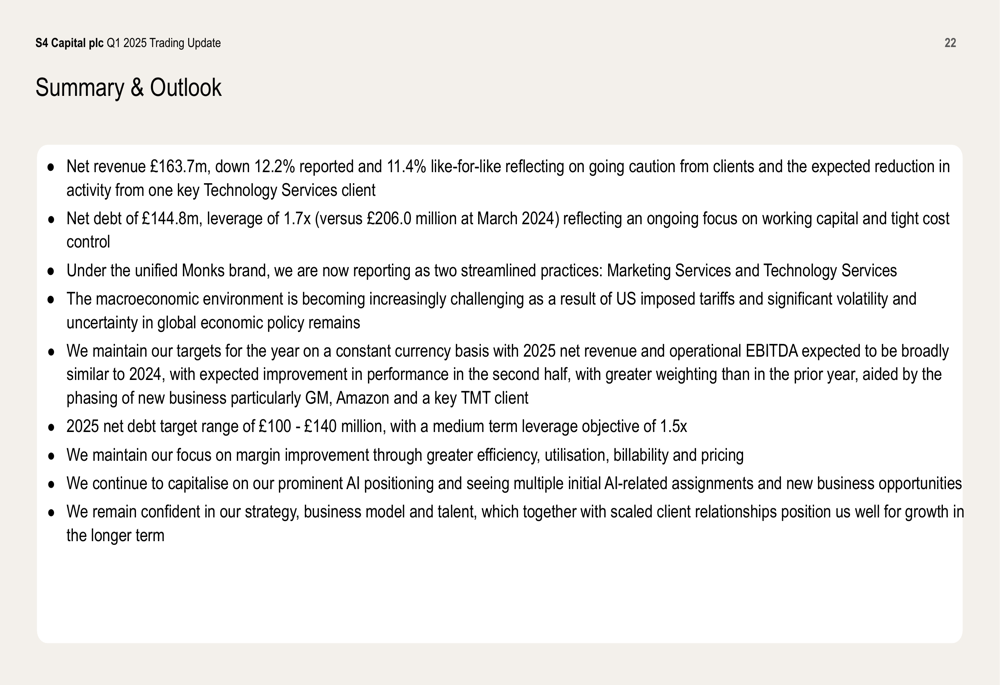

S4 Capital reported Q1 2025 revenue of £178.1 million, representing a substantial decline of 15.3% on a reported basis and 14.3% on a like-for-like basis compared to the same period last year. Net revenue, which the company uses as its primary performance metric, fell to £163.7 million, down 12.2% reported and 11.4% like-for-like.

As shown in the following financial headlines:

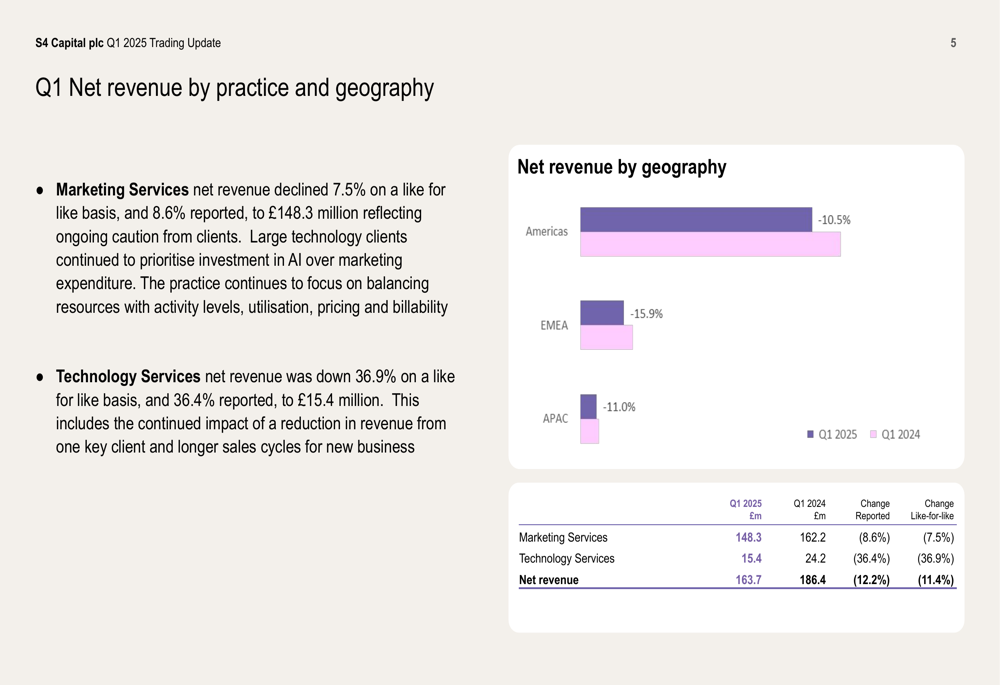

The company’s performance breakdown revealed divergent results between its two main service lines. Marketing Services, which accounts for the bulk of S4’s business, saw net revenue decline by 7.5% like-for-like to £148.3 million. However, Technology Services experienced a much steeper drop of 36.9% like-for-like to £15.4 million, which the company attributed partly to reduced activity from one key client.

The geographic breakdown shows revenue declines across all regions, with EMEA experiencing the sharpest contraction at 15.9%, followed by APAC at 11.0% and the Americas at 10.5%, as illustrated in this revenue breakdown:

Detailed Financial Analysis

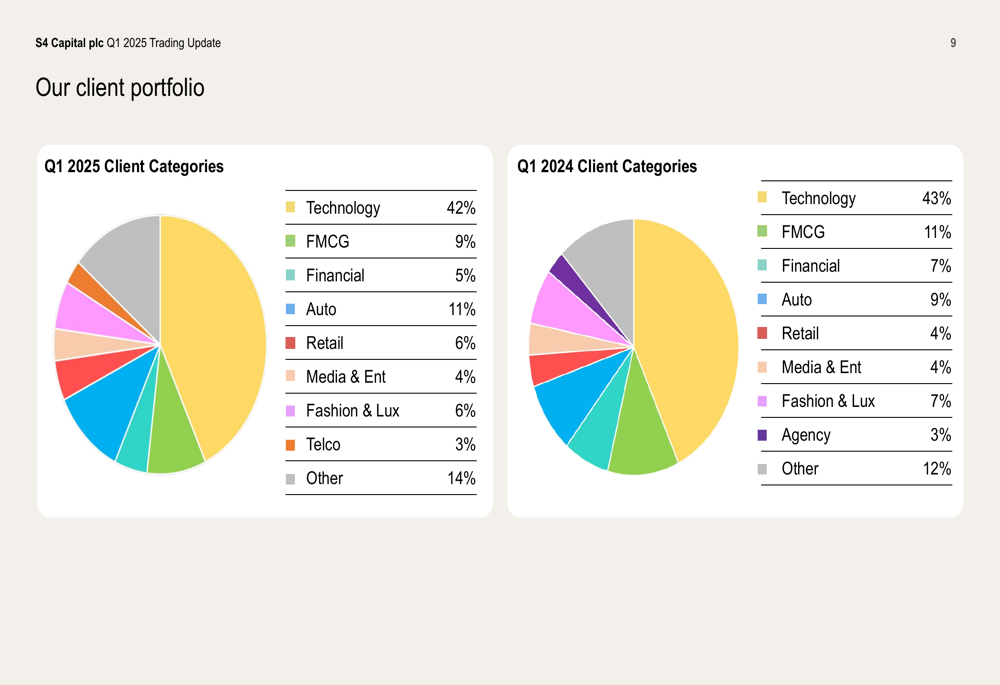

S4 Capital’s client portfolio remains heavily weighted toward the technology sector, which represented 42% of revenue in Q1 2025, down slightly from 43% in Q1 2024. The automotive sector increased its share from 9% to 11%, while FMCG declined from 11% to 9%, suggesting some shifts in the company’s client mix.

The following chart illustrates the company’s client portfolio composition:

Average revenue per client declined across all categories compared to the previous year. For the top 10 clients, average revenue fell from £10.2 million to £9.0 million, while the top 20 clients averaged £5.2 million, down from £6.2 million. This trend indicates that even S4’s largest clients are reducing their spending.

The client revenue breakdown shows that while the company maintained three clients with annual revenue exceeding £10 million, there was a reduction in clients in the £1-5 million bracket, from 21 to 16:

On a positive note, S4 Capital reported progress in reducing its debt burden. Net debt stood at £144.8 million at the end of Q1 2025, with leverage at 1.7x, an improvement from £206.0 million in the prior year. The company has targeted further debt reduction, with a 2025 net debt target range of £100-140 million and a medium-term leverage target of 1.5x.

Strategic Initiatives

Despite the challenging quarter, S4 Capital highlighted several strategic initiatives and client wins that it expects will drive improved performance in the second half of the year. The company emphasized its "Real-Time Brands" strategy, which aims to bridge the gap between brand strategies and media effectiveness in an increasingly digital world.

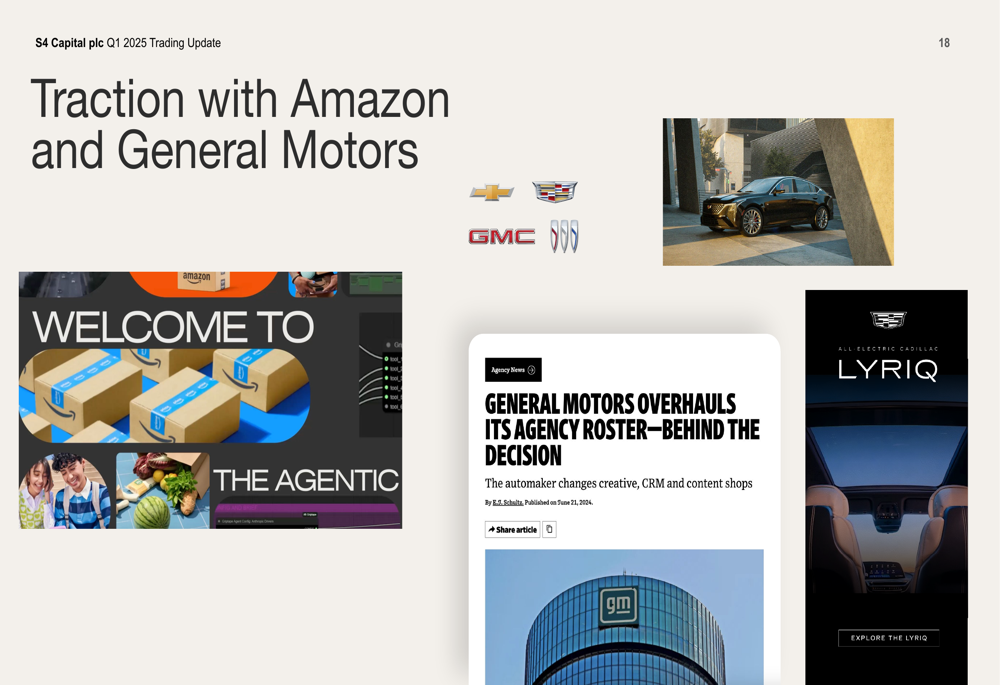

S4 Capital pointed to significant traction with major clients including Amazon (NASDAQ:AMZN) and General Motors (NYSE:GM), which it expects will positively impact second-half performance as these relationships continue to ramp up:

The company also showcased its strong regional presence, particularly in the Middle East and Africa (MEA) region, where it has assembled a diverse team with expertise across multiple markets. This regional strength has contributed to a growing client roster that includes major brands such as Google (NASDAQ:GOOGL), Etihad, Hilton, and NEOM.

The following slide demonstrates the company’s expanding client relationships:

Forward-Looking Statements

Despite the weak Q1 performance, S4 Capital maintained its guidance for 2025, targeting net revenue and operational EBITDA to be broadly similar to 2024 levels, with a second-half weighted skew. The company expects to generate positive free cash flow for the full year.

Management identified several focus areas to improve performance, including:

- Enhancing technology and processes to better manage pipeline and forecasting

- Improving productivity through better utilization and billability

- Leveraging AI and hub strategy

- Focusing on pricing and cost management

The company’s summary and outlook slide provides additional context for its forward-looking statements:

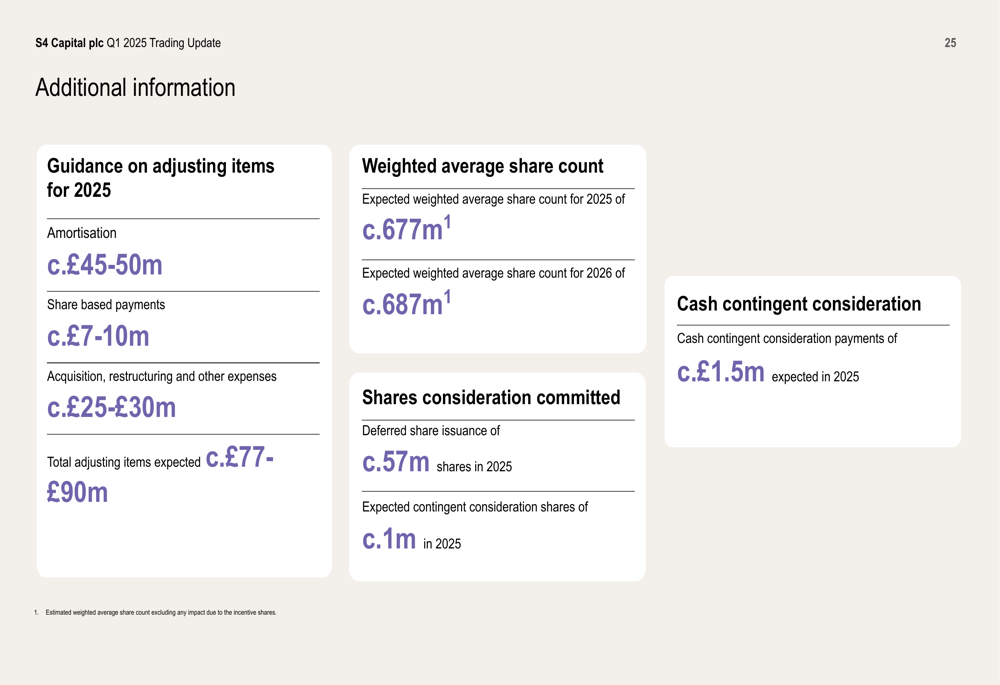

S4 Capital also provided detailed guidance on adjusting items for 2025, including amortization of £45-50 million, share-based payments of £7-10 million, and acquisition, restructuring and other expenses of £25-30 million, bringing total adjusting items to approximately £77-90 million:

While S4 Capital faces significant headwinds in the current market environment, management expressed confidence in the company’s strategy, business model, and talent to drive long-term growth. Investors will be watching closely to see if the anticipated second-half recovery materializes and whether the company can deliver on its maintained full-year guidance despite the challenging start to 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.