Broadcom named strategic vendor for Walmart virtualization solutions

Introduction & Market Context

SoFi Technologies (NASDAQ:SOFI) released its Q1 2025 investor presentation on April 29, showcasing record financial performance across multiple metrics as the fintech company continues to expand its digital banking ecosystem. The stock is currently trading at $13.20, up 2.48% in the most recent session, with premarket activity showing further gains of 3.56% to $13.67.

The Q1 results build on SoFi’s momentum from 2024, which CEO Anthony Noto previously described as the company’s "best year ever" when they achieved their first full year of GAAP profitability. The latest presentation demonstrates continued execution of SoFi’s strategy to diversify revenue streams and increase capital-light, fee-based income.

Quarterly Performance Highlights

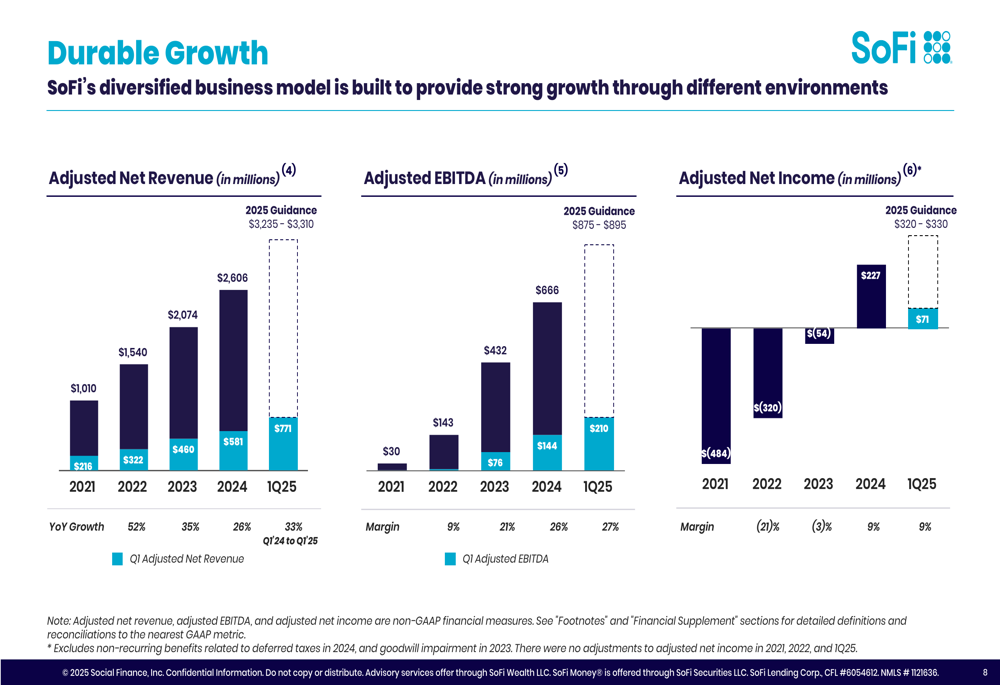

SoFi reported record adjusted net revenue of $771 million for Q1 2025, representing a 33% year-over-year increase. The company achieved record adjusted EBITDA of $210 million with a 27% margin, while GAAP net income reached $71 million (9% margin). This marks the sixth consecutive quarter of profitability for SoFi, with adjusted earnings per share of $0.06, an increase of $0.04 compared to Q1 2024.

As shown in the following chart of SoFi’s financial performance, the company has demonstrated consistent growth in revenue, EBITDA, and net income:

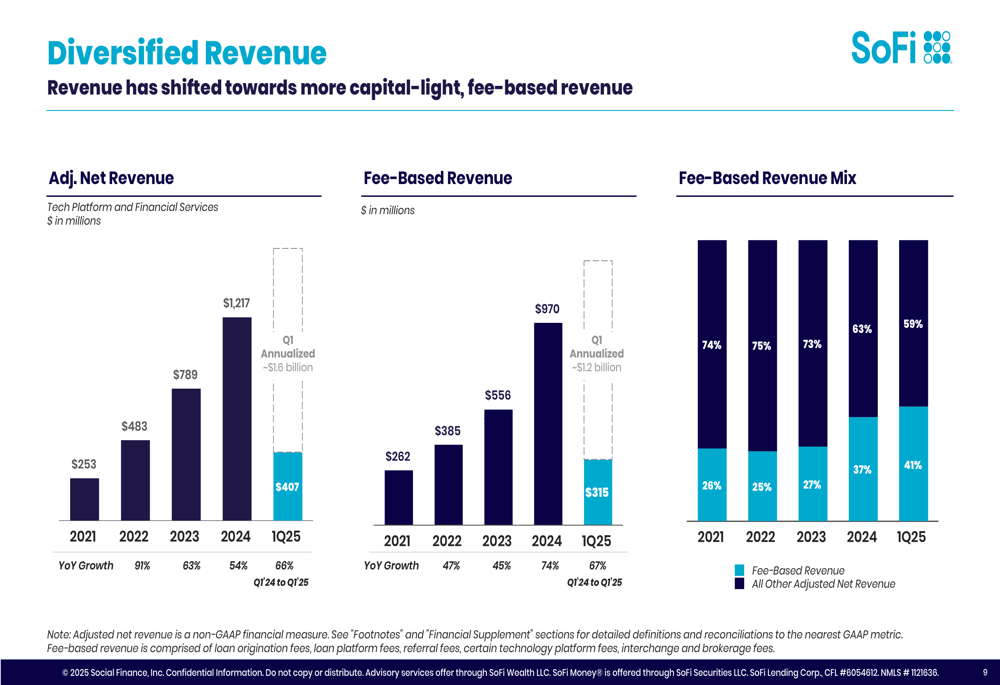

A key highlight of the quarter was the significant growth in fee-based revenue, which increased 67% year-over-year to $315 million, now representing 41% of adjusted net revenue. This shift toward more capital-light revenue streams is part of SoFi’s strategic evolution from its lending-focused origins.

The following chart illustrates SoFi’s revenue diversification and the growing contribution of fee-based revenue:

Member and Product Growth

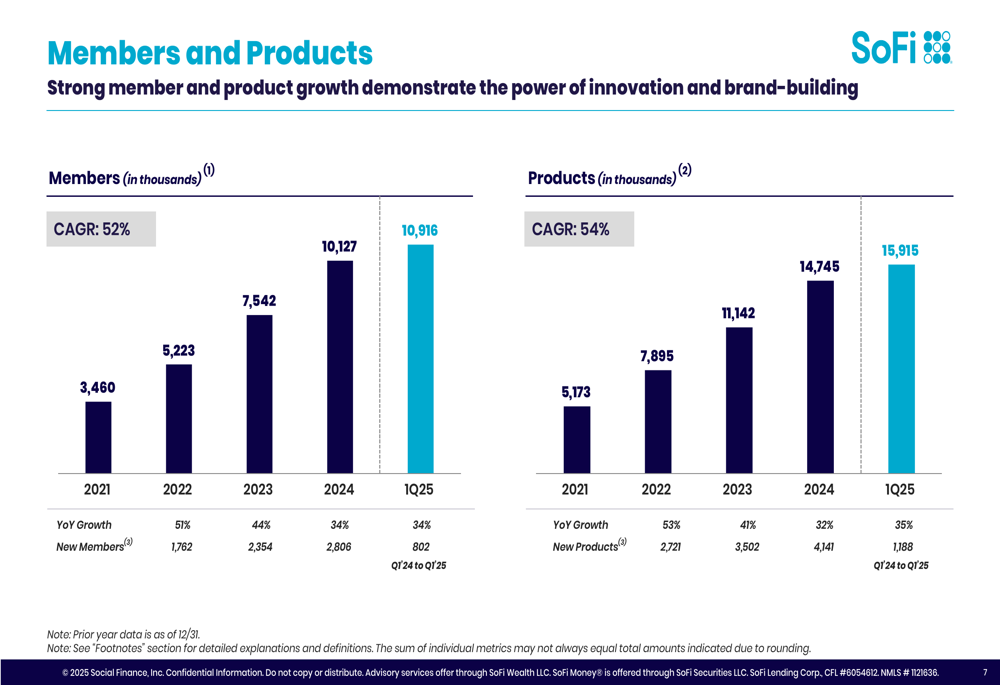

SoFi continues to expand its customer base at an impressive rate, adding 800,000 new members in Q1 2025 to reach a total of 10.9 million members, representing 34% year-over-year growth. The company also added 1.2 million new products during the quarter, bringing the total to 15.9 million products (35% year-over-year growth).

The following chart shows SoFi’s consistent member and product growth trajectory since 2021:

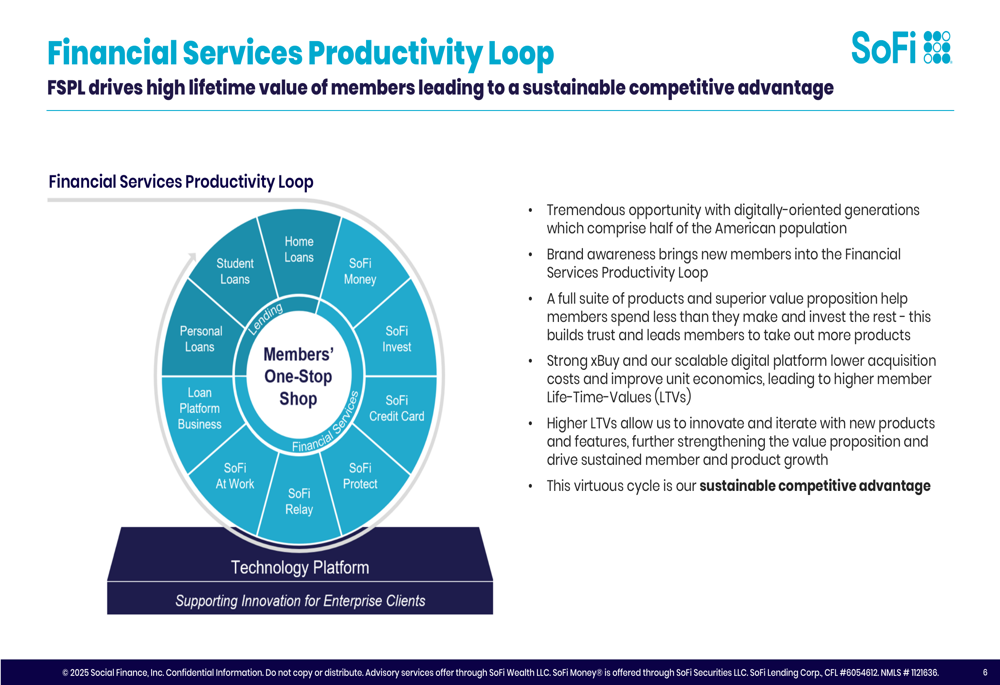

SoFi’s "Financial Services Productivity Loop" (FSPL) remains central to its growth strategy, designed to drive lifetime value and create a sustainable competitive advantage. The company positions itself as a "One-Stop Shop for Digital Financial Services," offering a comprehensive suite of products across banking, investing, lending, and other financial services.

As illustrated in the following diagram, SoFi’s strategy involves attracting members through various entry points and then cross-selling additional products to increase engagement and lifetime value:

Segment Performance Analysis

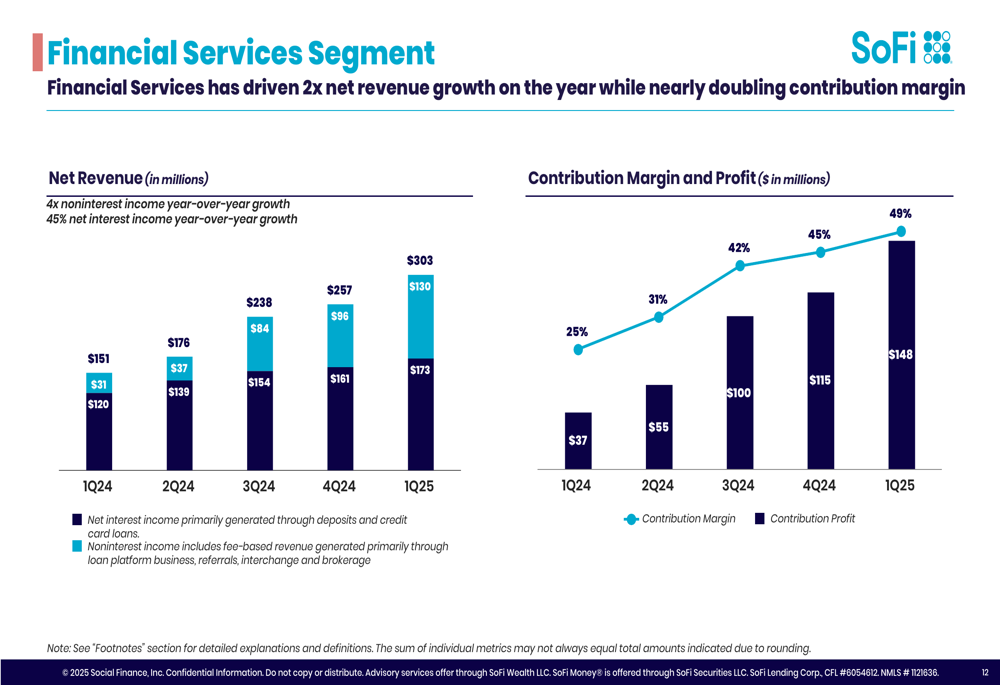

SoFi’s Financial Services segment showed particularly strong performance in Q1 2025, with revenue of $303 million, representing a doubling of non-interest income year-over-year. The segment’s contribution margin improved to 49%, generating $148 million in contribution profit.

The following chart details the Financial Services segment’s impressive growth trajectory:

The Lending segment also performed well, with adjusted net revenue of $361 million, a 27% year-over-year increase. The segment maintained a strong contribution margin of 66%, generating $239 million in contribution profit.

SoFi originated a record $7.2 billion in loans during the quarter, while also expanding its Loan Platform Business with over $8 billion in new commitments. The company finalized deals with Blue Owl, Fortress, and Edge Focus in early 2025 to further diversify its lending capabilities.

The Technology Platform segment showed more modest but still solid growth of 10% year-over-year, maintaining a consistent contribution margin of 33%.

Credit Quality and Balance Sheet Strength

SoFi reported improving credit quality metrics, with personal loan 90-day delinquencies declining 9 basis points sequentially to 46 basis points, while net charge-offs declined 6 basis points to 3.31%. The company attributes this performance to its time-tested credit model that underwrites to borrower cash flow.

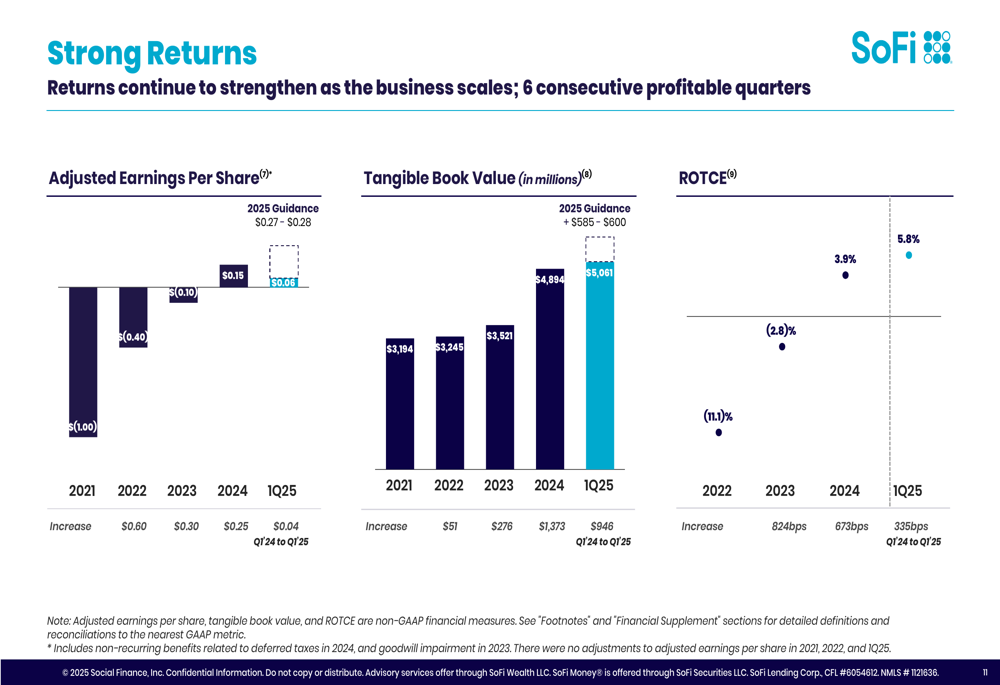

The company’s balance sheet continues to strengthen, with tangible book value increasing by $946 million year-over-year to $5.1 billion. SoFi’s return on tangible common equity (ROTCE) improved to 5.8%, an increase of 335 basis points from Q1 2024.

As shown in the following chart, SoFi has demonstrated consistent improvement in earnings per share, tangible book value, and ROTCE:

SoFi’s funding base has also improved, with member deposits growing by $2.2 billion during the quarter to over $27 billion. The company is now approximately 90% deposit-funded, with about 90% of deposits coming from durable direct deposit relationships. This shift toward more deposit funding has reduced SoFi’s funding expense by an estimated $515 million per year.

Forward-Looking Statements and Guidance

For full-year 2025, SoFi provided guidance of $3,235-$3,310 million in adjusted net revenue, $875-$895 million in adjusted EBITDA, and $320-$330 million in adjusted net income. The company expects to add at least 2.8 million new members in 2025, representing 28% growth from 2024 levels.

SoFi is targeting incremental adjusted EBITDA margins of approximately 30%, in line with its long-term investment philosophy. The company expects Financial Services adjusted net revenue to grow 60-65%, while both Lending and Technology Platform segments are projected to grow in the low double-digits to teens.

Looking beyond 2025, SoFi is targeting 20-25% annual EPS growth, continuing its strategy of balancing growth investments with improving profitability. The company plans to reinvest incremental revenue growth while maintaining its focus on strategic capital allocation.

As SoFi continues to execute on its diversification strategy and expand its digital financial ecosystem, the company appears well-positioned to capitalize on the ongoing shift toward digital banking services, particularly among digitally-oriented generations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.