U.S. stock futures slip lower; Cook’s firing increases Fed independence worries

Introduction & Market Context

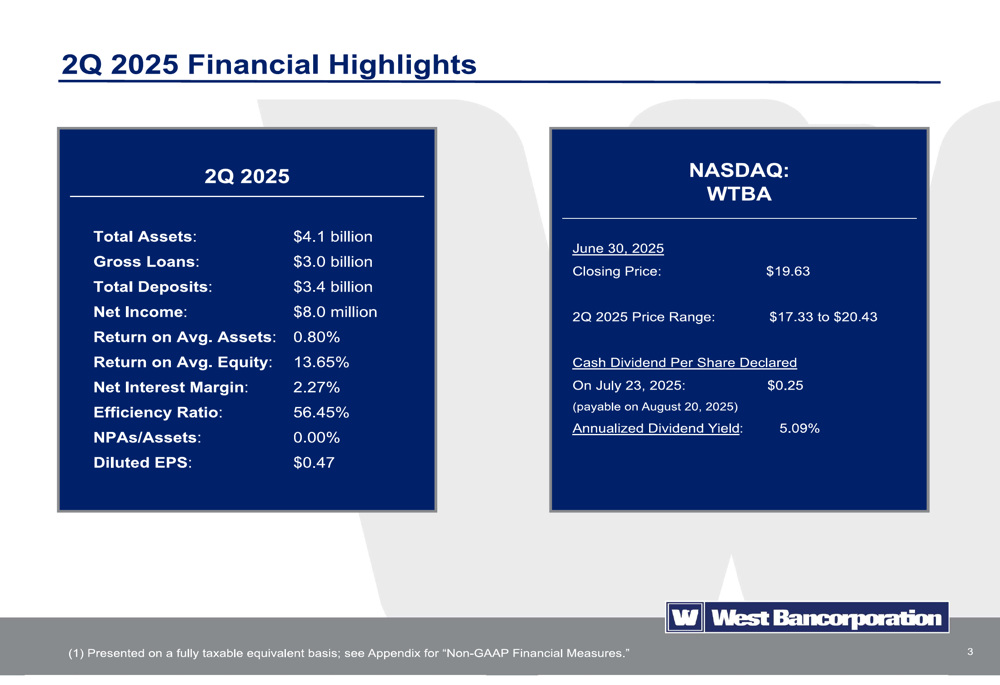

West Bancorporation (NASDAQ:WTBA) presented its second quarter 2025 earnings results on July 24, highlighting significant year-over-year improvement in profitability despite a challenging banking environment. The company reported net income of $8.0 million, up 54% from $5.2 million in the same quarter last year, while maintaining exceptional credit quality metrics.

Despite these strong fundamentals, WTBA stock has struggled, trading at $17.99 as of August 1, 2025, near its 52-week low of $17.33 and well below its 52-week high of $24.85. This disconnect between operational performance and stock price reflects broader market uncertainties in the banking sector.

Quarterly Performance Highlights

West Bancorporation’s Q2 2025 results showed significant improvement in key metrics compared to the prior year. The company reported diluted earnings per share of $0.47, slightly exceeding analyst expectations of $0.46.

As shown in the following financial highlights slide, the bank maintained a strong return on average equity of 13.65% and improved its net interest margin to 2.27%, up from 1.86% in Q2 2024:

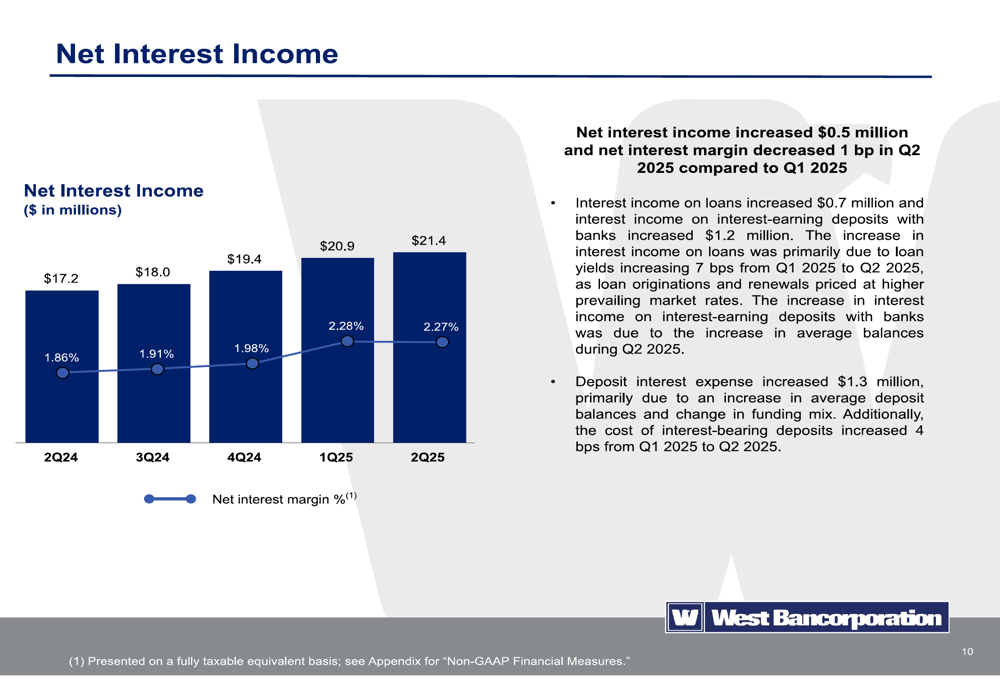

Net interest income reached $21.4 million in Q2 2025, representing a 24% increase from $17.2 million in Q2 2024. This improvement was primarily driven by higher loan yields and improved funding mix, though partially offset by increased deposit costs.

The following chart illustrates the steady improvement in net interest income and margin over the past five quarters:

CEO Dave Nelson commented during the earnings call, "Our journey back to top performing metrics is continuing as forecasted," reflecting the company’s strategic focus on relationship-based banking and disciplined growth.

Loan Portfolio and Credit Quality

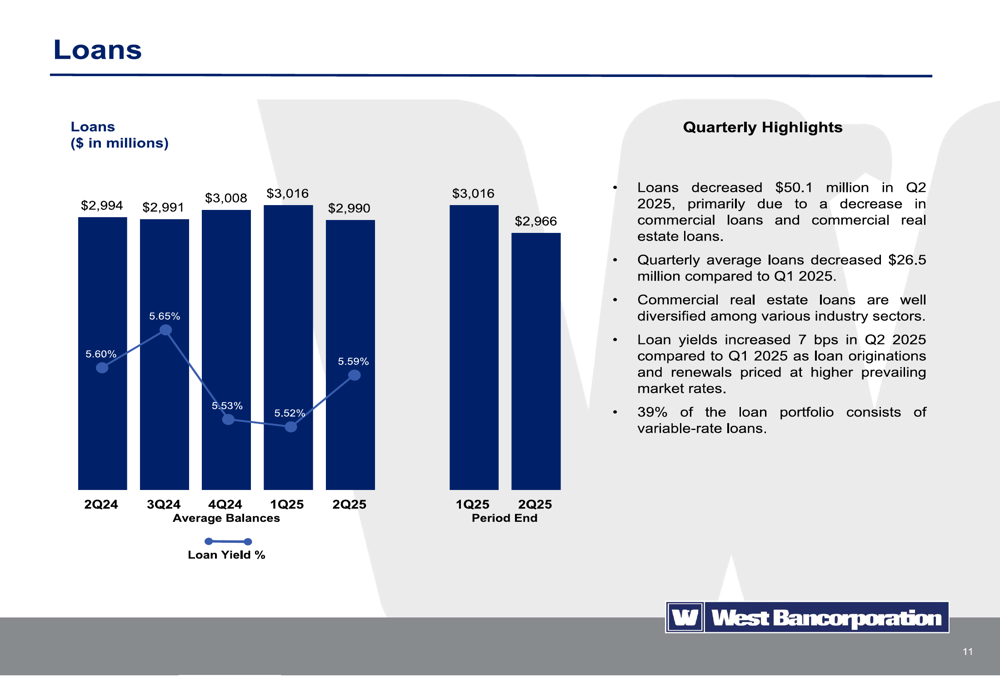

West Bancorporation’s loan portfolio contracted slightly in Q2 2025, with total loans decreasing by $50.1 million to $2.97 billion. This reduction was primarily in commercial and commercial real estate loans, as shown in the following chart:

Despite the contraction in loan balances, the bank’s loan yield improved to 5.59% in Q2 2025, up 7 basis points from the previous quarter and 39 basis points year-over-year. The company noted that 39% of its loan portfolio consists of variable-rate loans, providing some benefit from the higher interest rate environment.

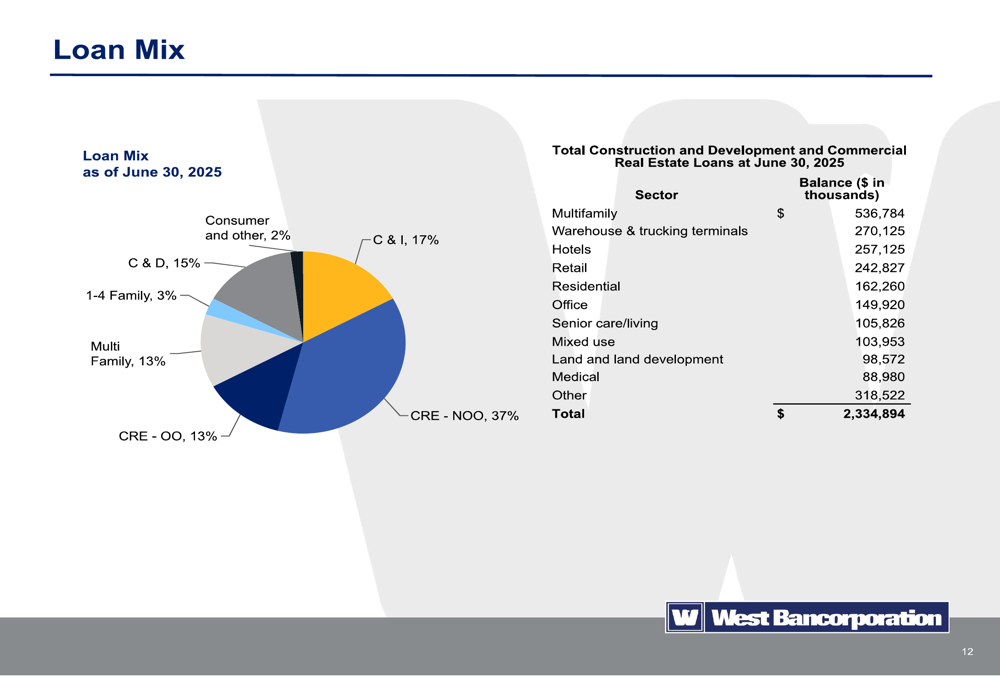

The loan portfolio remains well-diversified across various sectors, with commercial real estate representing the largest component at 63% of total loans:

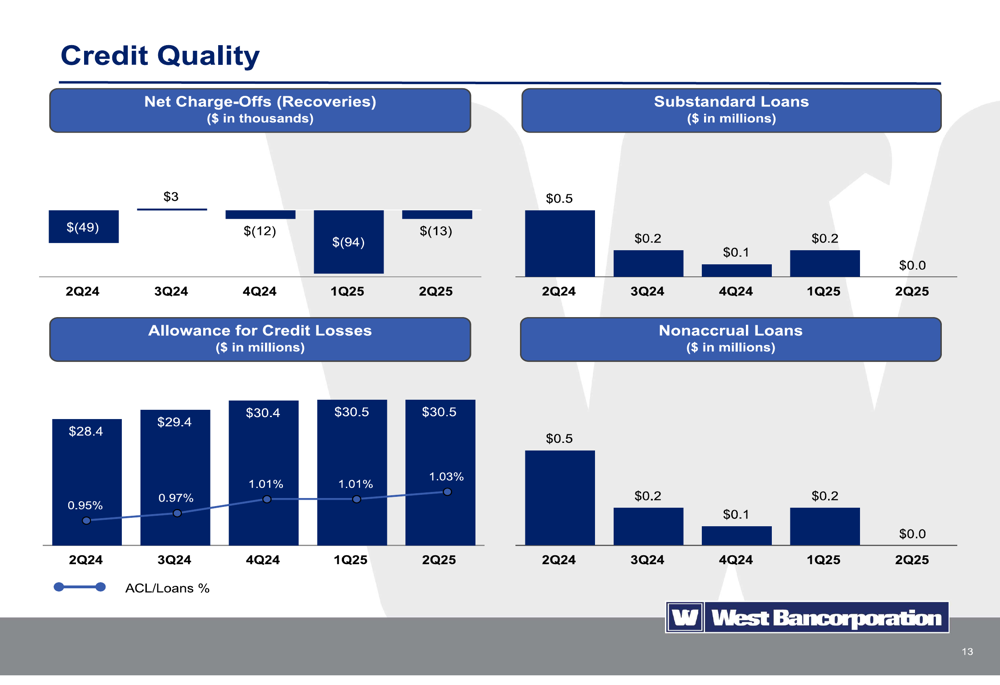

A standout feature of West Bancorporation’s performance is its exceptional credit quality. The bank reported zero nonperforming assets and zero substandard loans as of June 30, 2025, a remarkable achievement in the current economic environment:

Chief Risk Officer Harley Olufsen emphasized this point during the earnings call, highlighting the company’s "zero nonaccruals, and zero substandard loans." The allowance for credit losses remained stable at $30.5 million, representing 1.03% of total loans.

Deposit Growth and Funding Strategy

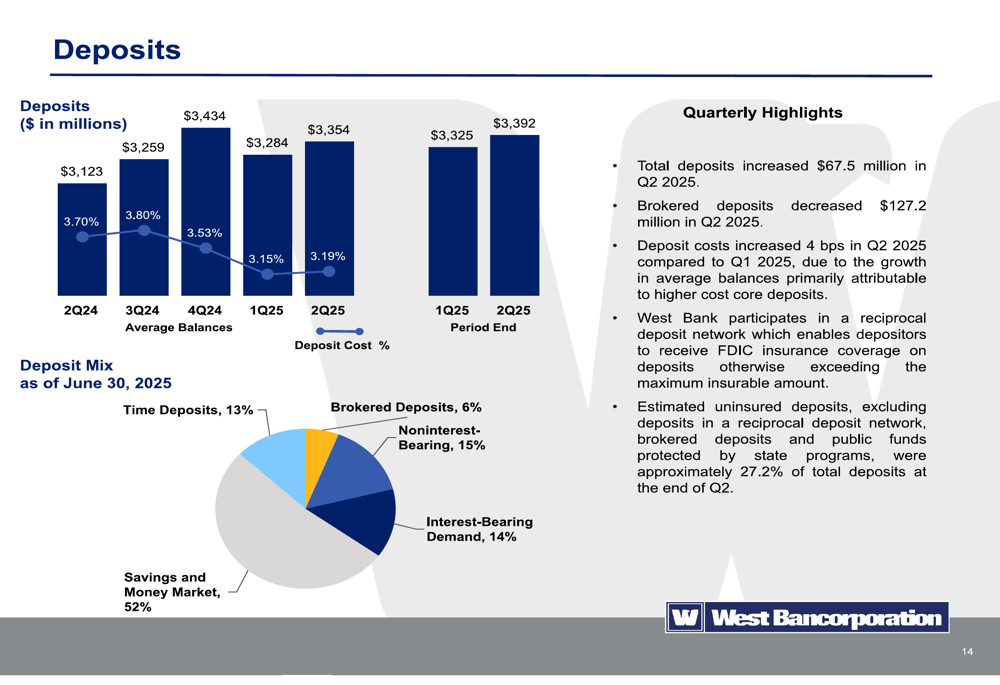

West Bancorporation reported total deposits of $3.39 billion as of June 30, 2025, an increase of $67.5 million during the quarter. The bank successfully reduced its reliance on brokered deposits, which decreased by $127.2 million, while growing core deposits.

The following chart shows the positive trend in deposit growth and the composition of the deposit base:

The deposit mix remains favorable, with 81% in core deposits (noninterest-bearing, interest-bearing demand, savings and money market accounts). Deposit costs increased slightly to 3.19% in Q2 2025, up 4 basis points from the previous quarter but significantly lower than the 3.70% cost in Q2 2024.

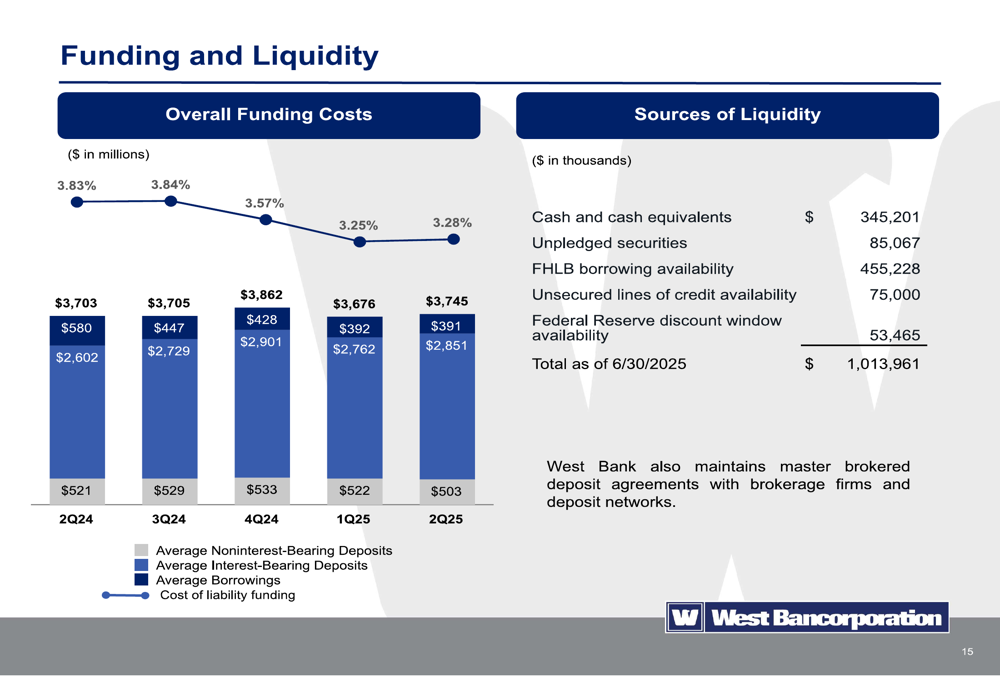

The bank maintains strong liquidity with over $1 billion in available funding sources, including $345.2 million in cash and cash equivalents:

Capital Position and Outlook

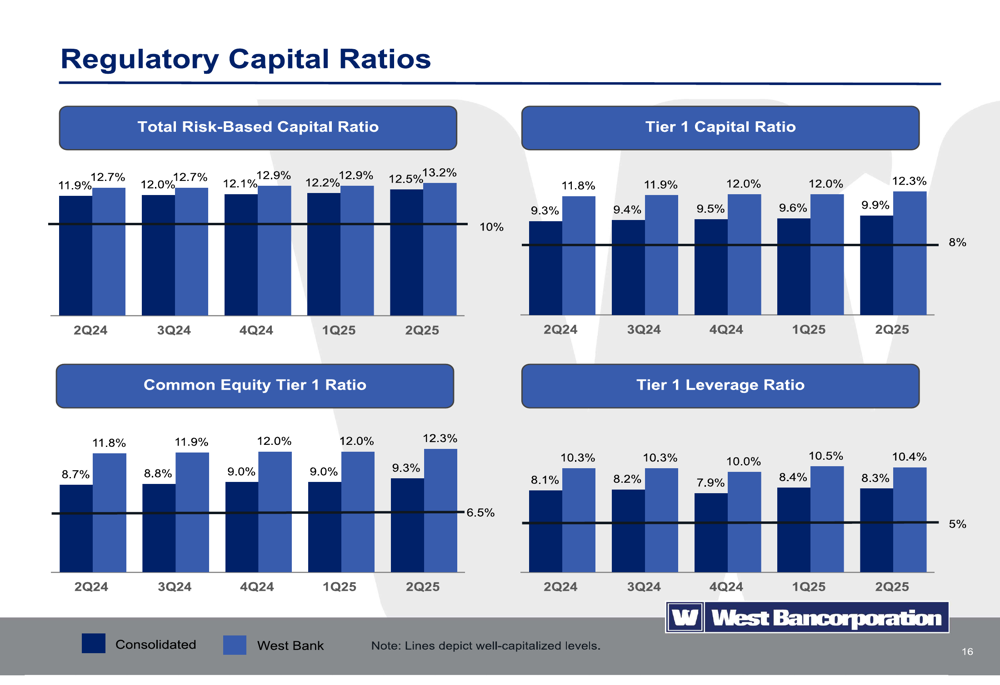

West Bancorporation’s regulatory capital ratios improved across all metrics compared to both the previous quarter and the same period last year. The consolidated total risk-based capital ratio reached 12.5% as of June 30, 2025, up from 12.2% in the previous quarter and 11.9% a year ago:

Looking forward, management anticipates continued asset repricing through 2025 and 2026, with further margin improvements expected. The company is focused on deposit growth and exploring opportunities arising from potential market consolidation.

Analysts project steady growth for West Bancorporation, with EPS forecasts of $0.48 for Q3 2025 and $0.52 for Q4 2025. With a current dividend of $0.25 per share (representing an annualized yield of approximately 5.3%) and 27 consecutive years of dividend payments, the bank continues to offer value to income-focused investors despite its recent stock price weakness.

Brad Peters, Minnesota Group President, emphasized the company’s strategic focus on "deposit-rich business banking opportunities" as a key driver for future growth. However, investors should monitor the bank’s ability to reverse the recent loan contraction and navigate the competitive banking landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.