5 big analyst AI moves: Apple lifted to Buy, AI chip bets reassessed

Introduction & Market Context

Wintrust Financial Corporation (NASDAQ:WTFC) reported record quarterly net income in its Q3 2025 earnings presentation, continuing its trend of strong financial performance. The company’s stock rose 1.22% following the announcement, closing at $126.74, as investors responded positively to results that exceeded analyst expectations.

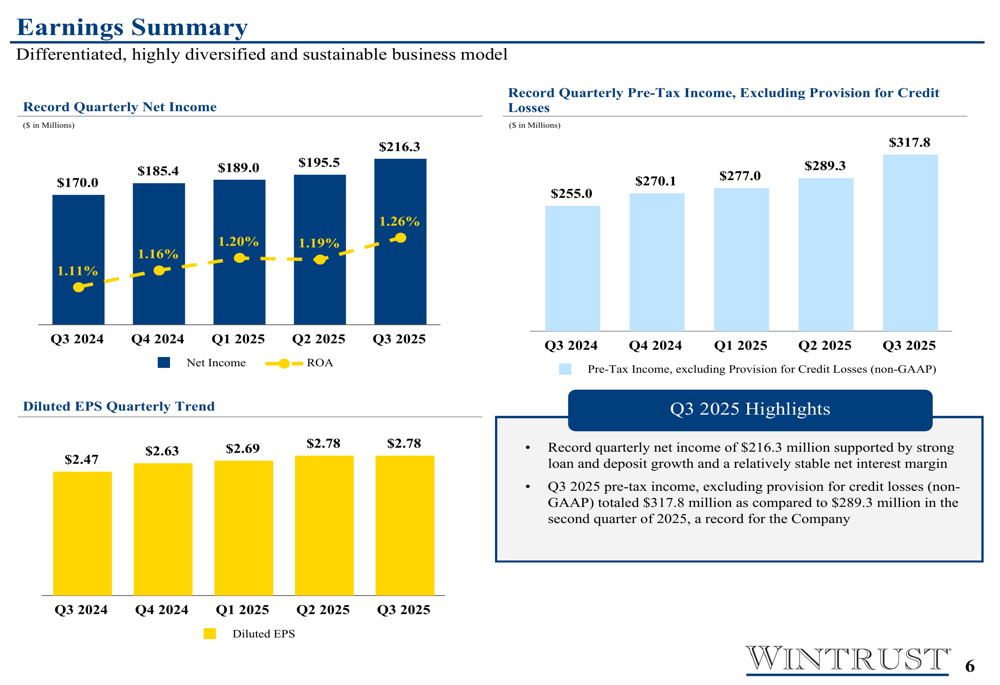

According to the company’s presentation slides, Wintrust achieved record quarterly net income of $216.3 million, up $20.7 million from the previous quarter. This performance was driven by robust loan and deposit growth, coupled with effective expense management and strong credit quality.

Quarterly Performance Highlights

Wintrust’s Q3 2025 results showed significant improvement across key metrics. The company reported a return on assets of 1.26%, up 7 basis points from the previous quarter, while maintaining a stable net interest margin of 3.50%.

As shown in the following chart of quarterly earnings, Wintrust has demonstrated consistent growth in both net income and pre-tax, pre-provision income over the past five quarters:

The company’s diluted earnings per share remained steady at $2.78 according to the presentation slides. However, the actual reported EPS was $3.06, significantly exceeding the forecasted $2.63, representing a 16.35% earnings surprise.

Efficiency improved substantially, with the efficiency ratio decreasing by 223 basis points to 54.69% (GAAP) and by 221 basis points to 54.47% (non-GAAP), reflecting the company’s success in managing expenses while growing revenue.

Loan and Deposit Growth

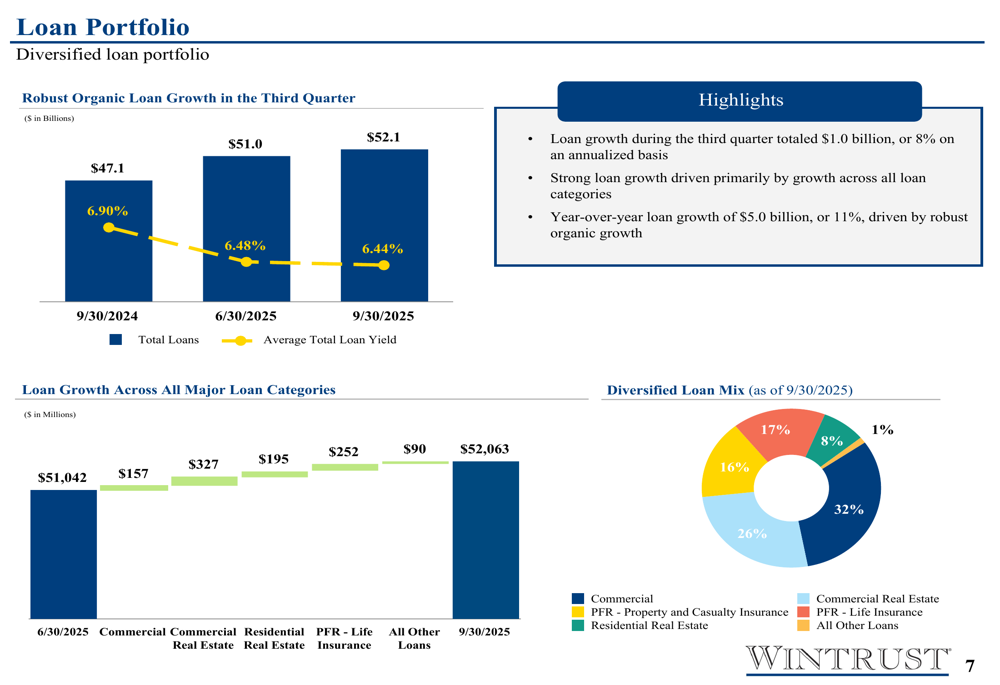

Wintrust reported strong loan growth across all major categories in Q3 2025. Total loans increased by $1.0 billion to $52.1 billion, representing an 8% annualized growth rate. Year-over-year, the loan portfolio expanded by $5.0 billion or 11%.

As illustrated in the following loan portfolio breakdown, the company maintains a well-diversified loan mix across commercial, real estate, and consumer segments:

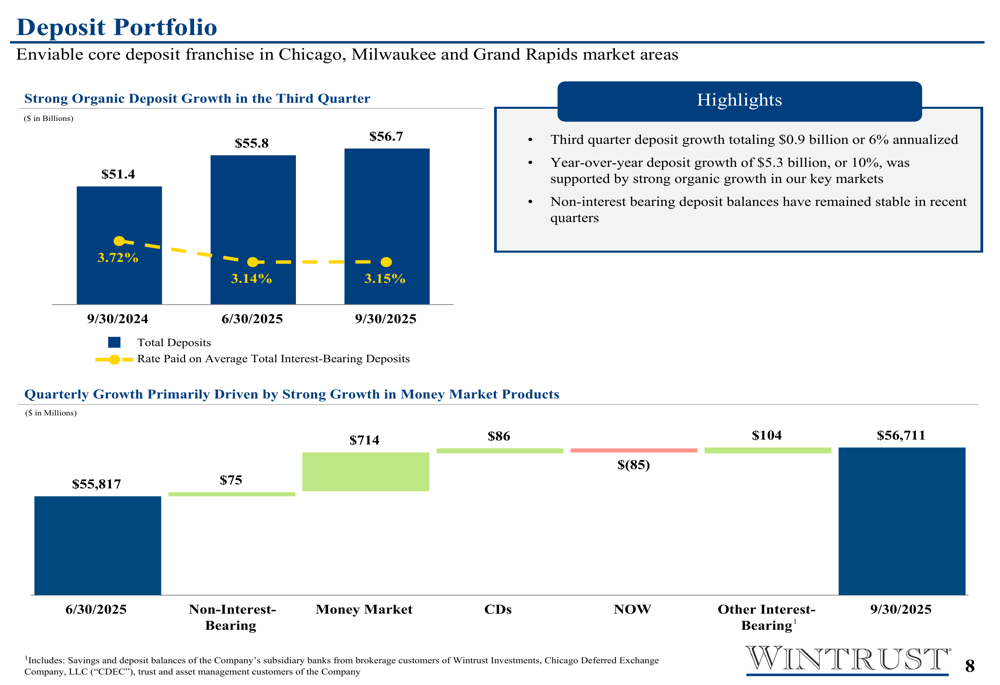

On the funding side, total deposits grew by $894.6 million to $56.7 billion, a 6% annualized growth rate. Year-over-year deposit growth reached $5.3 billion or 10%. The quarterly growth was primarily driven by money market products, as shown in the following chart:

During the earnings call, CEO Tim Crane emphasized the company’s disciplined approach to underwriting, while Chief Lending Officer Richard Murphy highlighted market share gains, noting, "We continue to take market share. We deliver a very good product for our customers."

Net Interest Income and Margin

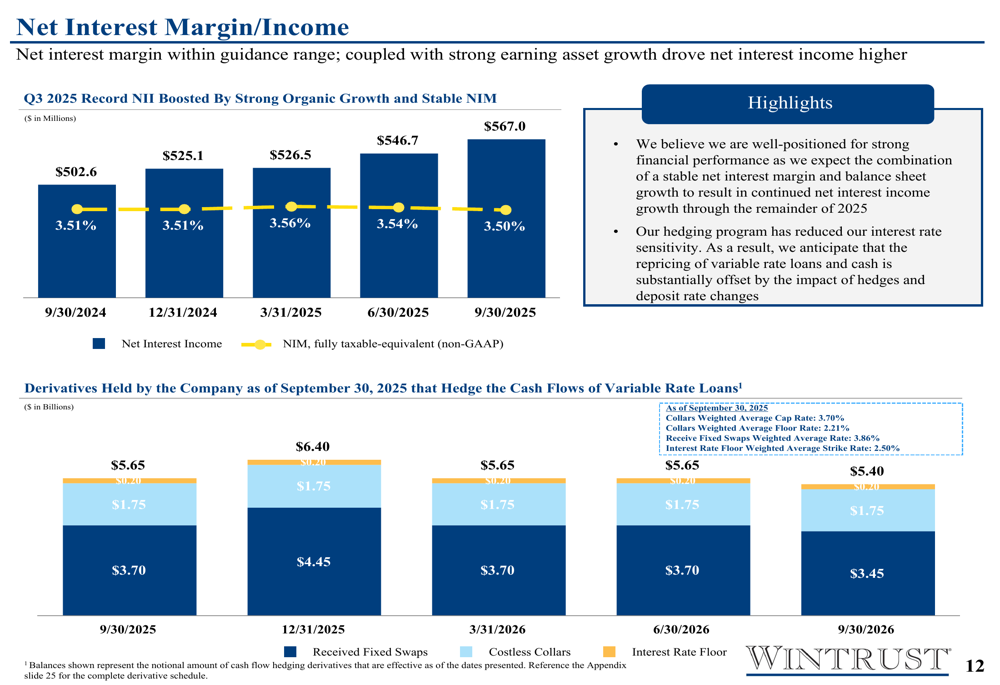

Net interest income, a critical revenue driver for banks, continued its upward trajectory in Q3 2025, reaching $567.0 million, up from $546.7 million in the previous quarter. This represents the fifth consecutive quarter of growth in this key metric.

The following chart shows the steady increase in net interest income, alongside a relatively stable net interest margin:

The net interest margin remained within the company’s target range at 3.50%, slightly down from 3.54% in the previous quarter. To manage interest rate risk, Wintrust maintains a hedging strategy that includes derivatives to protect against potential interest rate volatility, as detailed in the presentation.

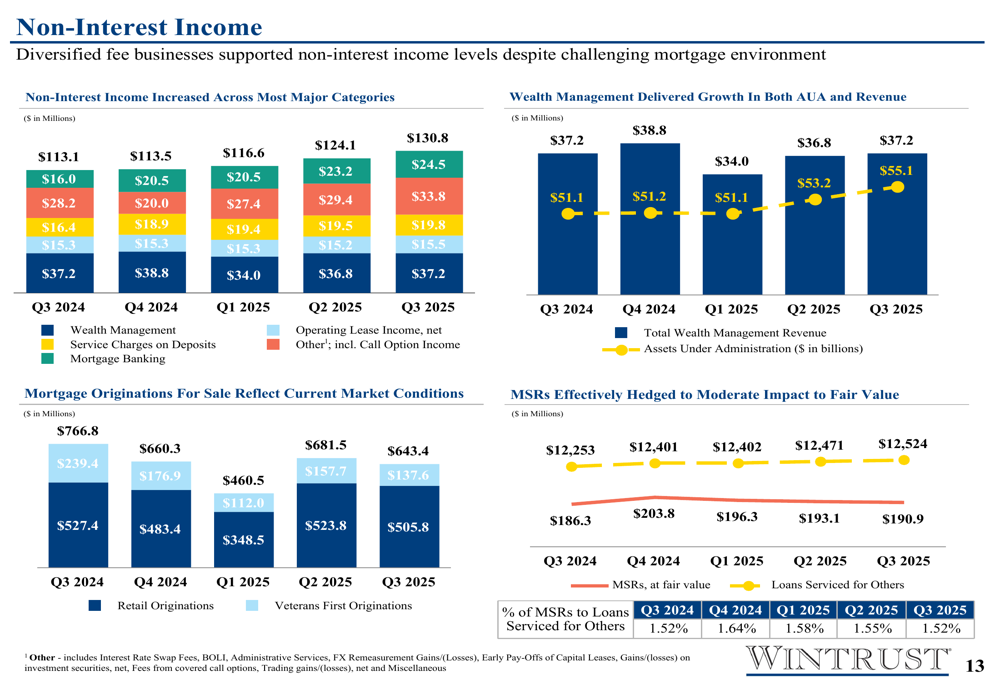

Non-Interest Income and Expense

Non-interest income showed improvement across most major categories in Q3 2025, contributing to the company’s strong overall performance. The following chart illustrates the trends in various non-interest income components:

Service charges on deposits showed healthy growth, while mortgage banking remained stable despite challenging market conditions. Wealth management revenue has been consistent, providing a reliable income stream.

On the expense side, Wintrust has demonstrated effective cost management while continuing to grow assets. The company’s non-interest expense as a percentage of average assets has declined steadily over time, reflecting improved operational efficiency.

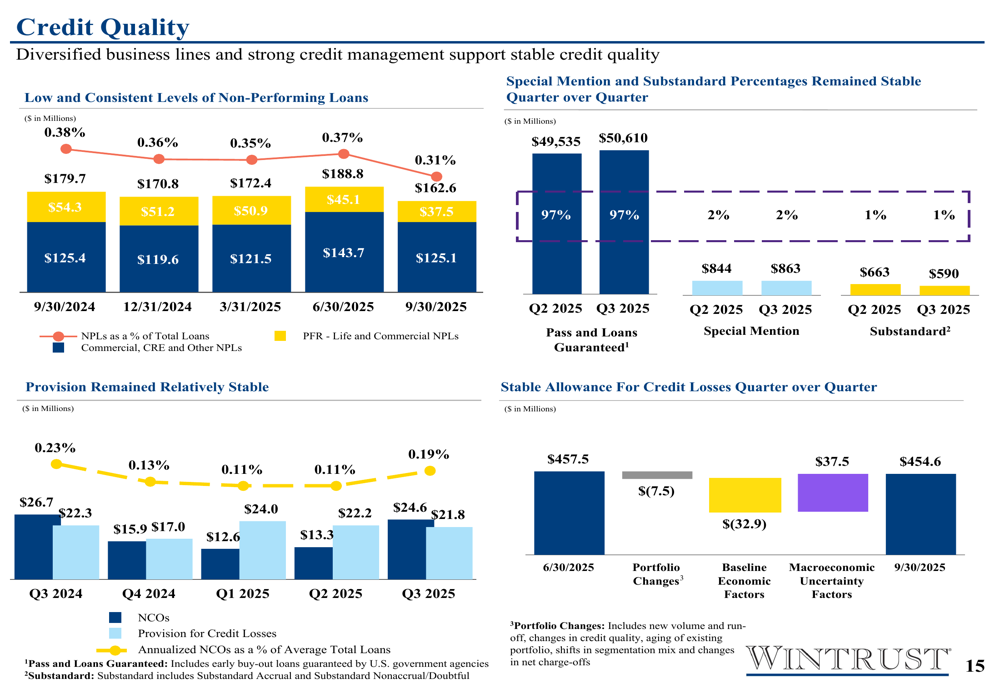

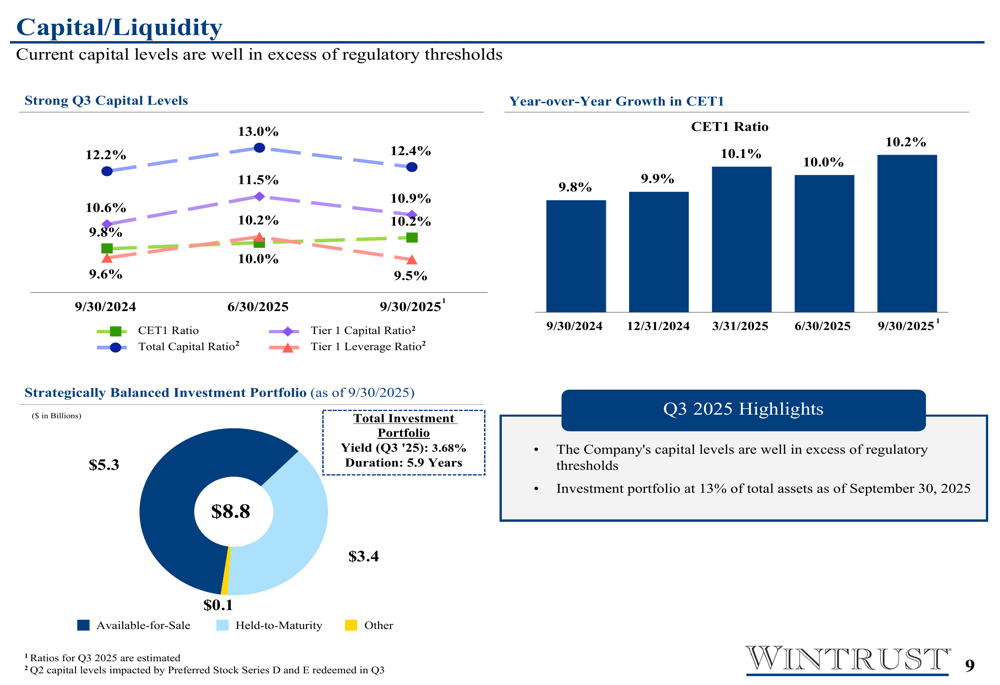

Credit Quality and Capital Position

Wintrust maintained strong credit quality in Q3 2025, with non-performing loans decreasing to 0.31% of total loans, down from 0.37% in the previous quarter. This represents a historically low level for the company, as illustrated in the following chart:

The allowance for credit losses stood at 1.34% of loans, providing appropriate coverage against potential loan losses. Net charge-offs were 19 basis points for the quarter, reflecting disciplined risk management.

Capital ratios remained robust, with the Common Equity Tier 1 (CET1) ratio at 10.2%, up from 9.8% a year earlier. The following chart shows the trend in capital ratios:

The company’s tangible book value per share has shown consistent growth over time, reaching $85.39 as of September 30, 2025, up from $76.15 a year earlier. This represents a 12.1% year-over-year increase, reflecting the company’s sustained profitability.

Shareholder Returns

Wintrust has outperformed the KBW Nasdaq Regional Banking Total Return Index (KRXTR) across all time horizons, delivering superior returns to shareholders. The company’s total shareholder return over the past five years was 349.56%, compared to 221.50% for the index.

Outlook & Guidance

Looking forward, Wintrust anticipates mid to high single-digit growth in loans and deposits, with a continued net interest margin of around 3.50%. The company remains open to modest mergers and acquisitions, emphasizing strategic and cultural alignment.

Organic growth continues to be a priority, supported by ongoing investments in capabilities to serve larger clients. The company’s relationship-based banking approach is expected to continue yielding positive results, with significant market share gains in key regions like Illinois, Wisconsin, and West Michigan.

Conclusion

Wintrust’s Q3 2025 presentation slides reveal a company with strong momentum, delivering record earnings while maintaining disciplined growth and risk management. The consistent improvement in key metrics, coupled with the company’s diversified business model and strong market position, positions Wintrust well for continued success in the competitive banking landscape.

The positive market reaction to the earnings announcement reflects investor confidence in the company’s strategy and execution. With strong capital levels, improving efficiency, and a proven track record of growth, Wintrust appears well-positioned to navigate potential economic challenges while capitalizing on market opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.