Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

American Airlines Group (NASDAQ:AAL) presented its second-quarter 2025 financial results on July 24, 2025, reporting record quarterly revenue but facing declining profitability compared to the previous year. Despite beating earnings expectations, the airline’s stock dropped 7.85% in pre-market trading, closing at $11.78, as investors reacted to operational challenges and a cautious outlook for the remainder of the year.

The carrier’s presentation highlighted its ongoing efforts to strengthen its balance sheet, grow its loyalty program, and enhance customer experience, while navigating a challenging operating environment. Trading between its 52-week range of $8.5 to $19.1, American Airlines continues to face market volatility with its stock down 25.2% over the past six months.

Quarterly Performance Highlights

American Airlines reported record quarterly revenue of $14.4 billion for Q2 2025, slightly above forecasts with a 0.4% increase year-over-year. The company posted GAAP earnings per diluted share of $0.91, while adjusted earnings per share reached $0.95, surpassing analyst expectations of $0.78 by 21.79%.

The airline generated substantial cash flow, with $3.4 billion in operating cash flow and free cash flow of $2.5 billion in the first half of 2025. The company ended the quarter with $12 billion of total available liquidity, providing a strong financial buffer.

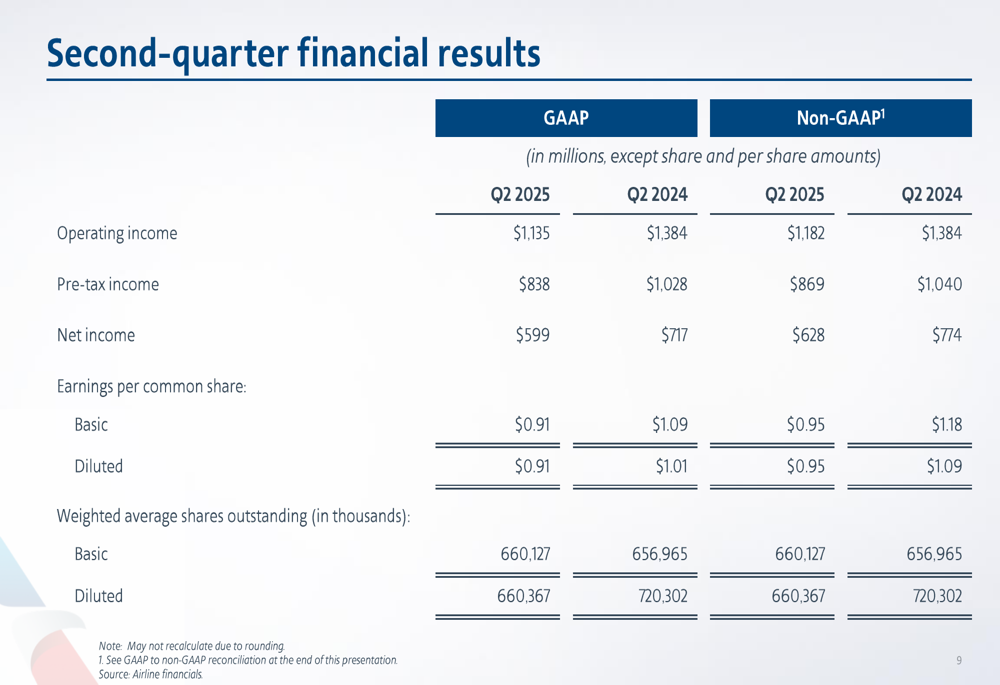

As shown in the following comprehensive financial results table:

However, despite the revenue growth, profitability metrics declined year-over-year. Operating income decreased to $1,135 million from $1,384 million in Q2 2024, while net income fell to $599 million from $717 million in the same period last year. This decline in profitability occurred despite the record revenue, suggesting cost pressures and operational challenges.

Detailed Financial Analysis

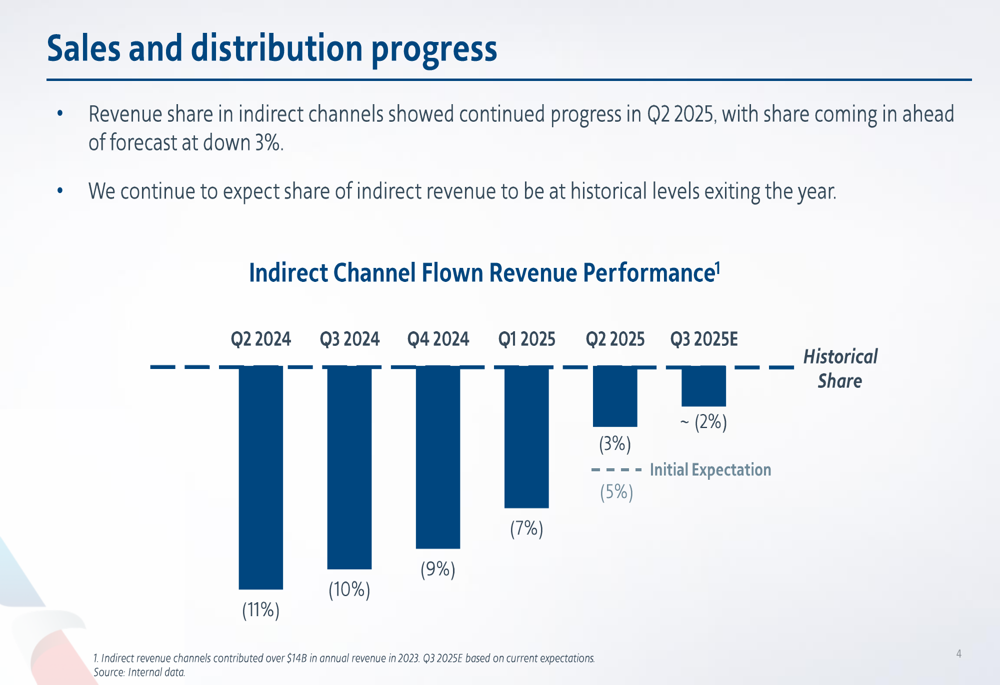

American Airlines’ presentation highlighted improvements in its indirect channel revenue performance, with Q2 2025 showing only a 3% decline, better than the company’s forecast. The airline expects indirect revenue channels, which contributed over $14 billion in annual revenue in 2023, to return to historical levels by the end of the year.

The following chart illustrates the improving trend in indirect channel revenue performance:

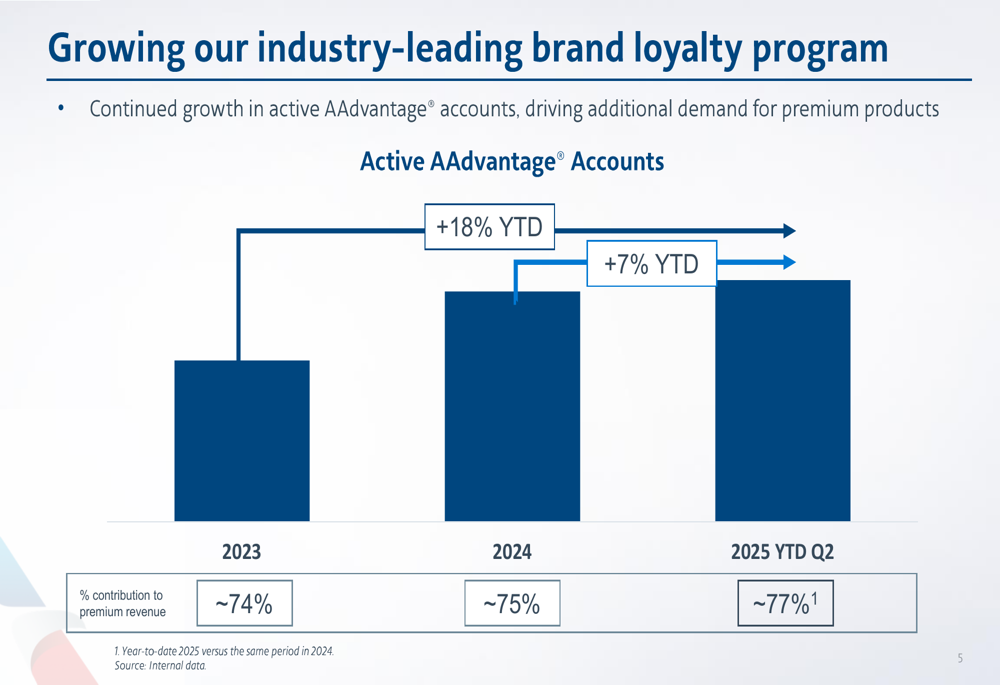

The company’s loyalty program continues to be a significant driver of premium revenue. The AAdvantage program contributed approximately 77% to premium revenue in the first half of 2025, up from 75% in 2024 and 74% in 2023. This growth underscores the strategic importance of the loyalty program to American’s revenue strategy.

As shown in the following chart of AAdvantage program contribution:

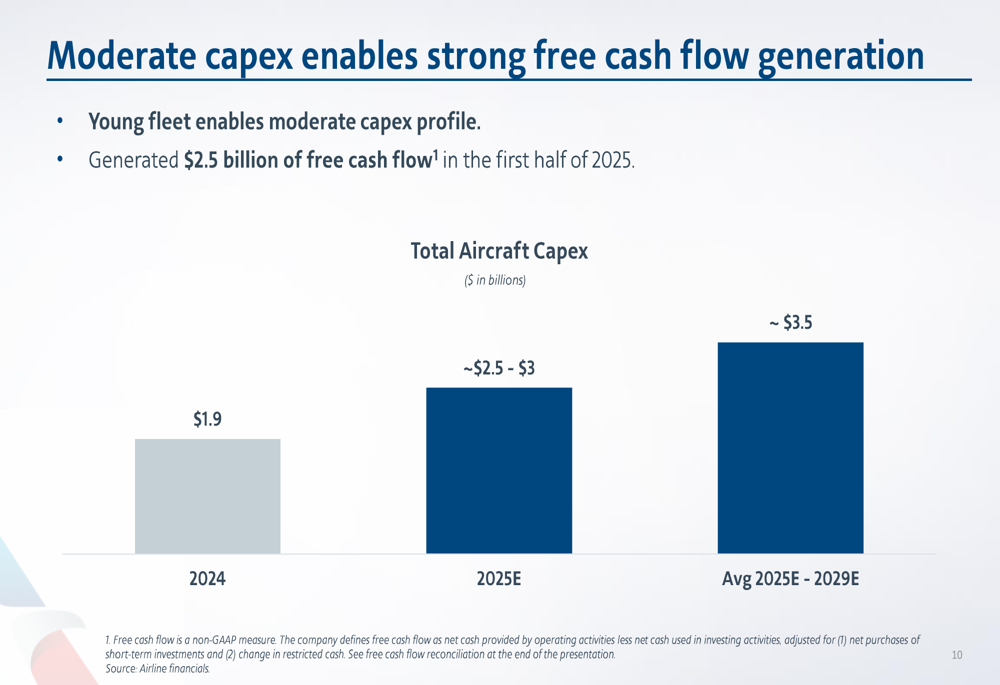

American Airlines’ capital expenditure remains moderate due to its relatively young fleet, enabling strong free cash flow generation. The company expects total aircraft capex of approximately $2.5-$3 billion in 2025, with an average of around $3.5 billion annually from 2025 to 2029.

The following chart illustrates the company’s capex profile:

Strategic Initiatives

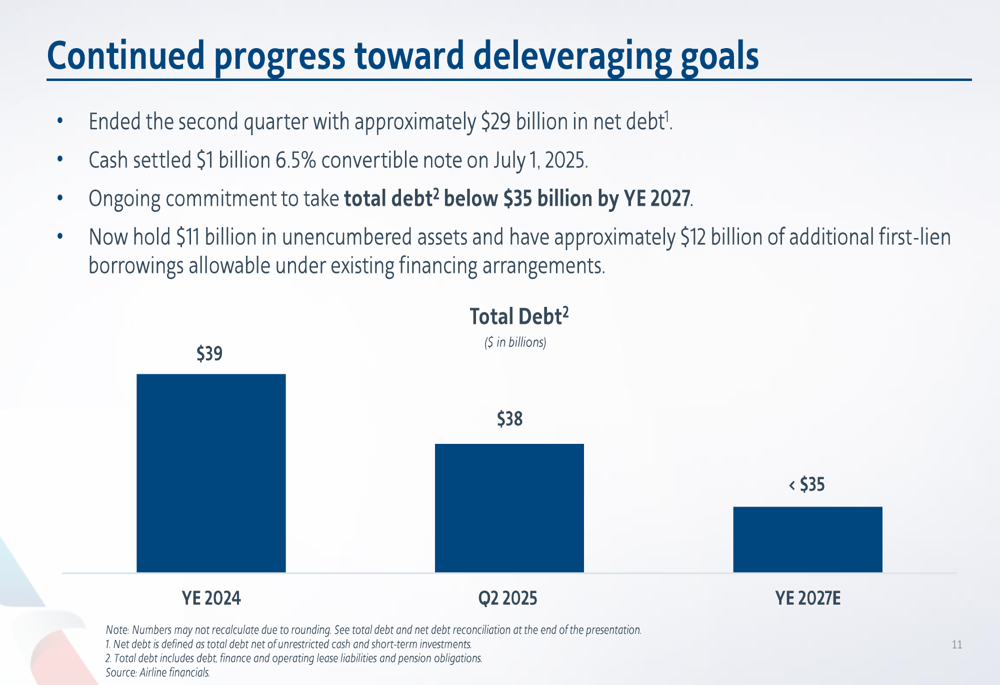

American Airlines continues to make progress on its deleveraging goals, ending the second quarter with approximately $29 billion in net debt. The company cash settled a $1 billion 6.5% convertible note on July 1, 2025, and maintains its commitment to reduce total debt below $35 billion by the end of 2027.

The following chart shows the company’s debt reduction progress:

The airline also emphasized its renewed focus on customer experience, introducing the Flagship Suite and expanding premium lounges in Philadelphia and Miami. Additional enhancements include One Stop Security for flights into the U.S., boarding process improvements, and the Connect Assist tool at DFW.

CEO Robert Isom expressed confidence in the company’s long-term initiatives during the earnings call, stating, "We’re confident that we’re delivering on the right long-term initiatives." He also highlighted the airline’s position to benefit from a recovery in domestic demand, saying, "We believe American is uniquely positioned to benefit as domestic demand recovers in the back half of the year."

Forward-Looking Statements

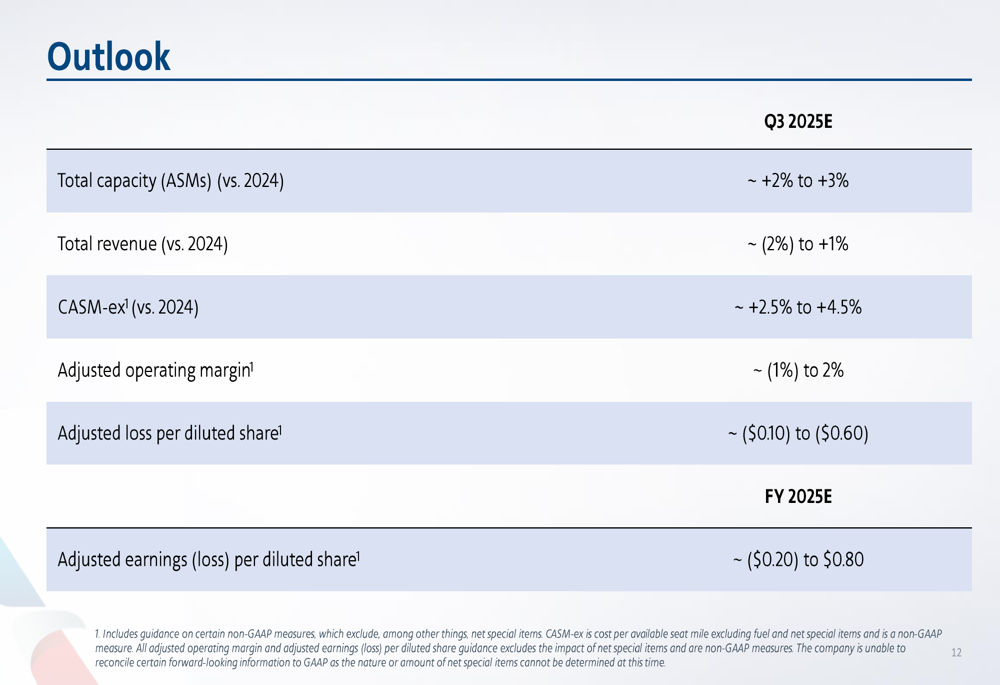

American Airlines provided a cautious outlook for the third quarter and full year 2025. For Q3, the company expects total capacity to increase by approximately 2% to 3% compared to 2024, while total revenue is projected to range between a 2% decline and a 1% increase. The adjusted operating margin is forecast to be between -1% and 2%, with an adjusted loss per diluted share between $0.10 and $0.60.

For the full year 2025, American Airlines expects adjusted earnings (loss) per diluted share to range from -$0.20 to $0.80, reflecting continued uncertainty in the domestic market.

The following slide details the company’s outlook:

Despite the earnings beat, investors appear concerned about the 36% increase in operational disruptions compared to last year, which wasn’t directly addressed in the presentation. These operational challenges, combined with the cautious outlook, likely contributed to the negative stock reaction following the earnings release.

Analysts remain cautiously optimistic with a consensus rating of 2.12, while price targets range from $8 to $20 per share. Seven analysts have recently revised their earnings expectations upward for the upcoming period, suggesting some confidence in the airline’s ability to navigate current challenges.

American Airlines’ ability to maintain its record revenue while addressing operational issues and continuing its debt reduction strategy will be crucial for investor confidence in the coming quarters. The company’s strong cash flow generation and growing loyalty program provide positive foundations, but the challenging outlook and operational disruptions present significant headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.