Trump announces trade deal with EU following months of negotiations

Introduction & Market Context

Baker Hughes Company (NASDAQ:BKR) released its first quarter 2025 results on April 23, showcasing record first-quarter adjusted EBITDA despite facing challenging market conditions. The company’s presentation highlighted strong year-over-year margin expansion while acknowledging headwinds from tariff impacts and softening upstream spending.

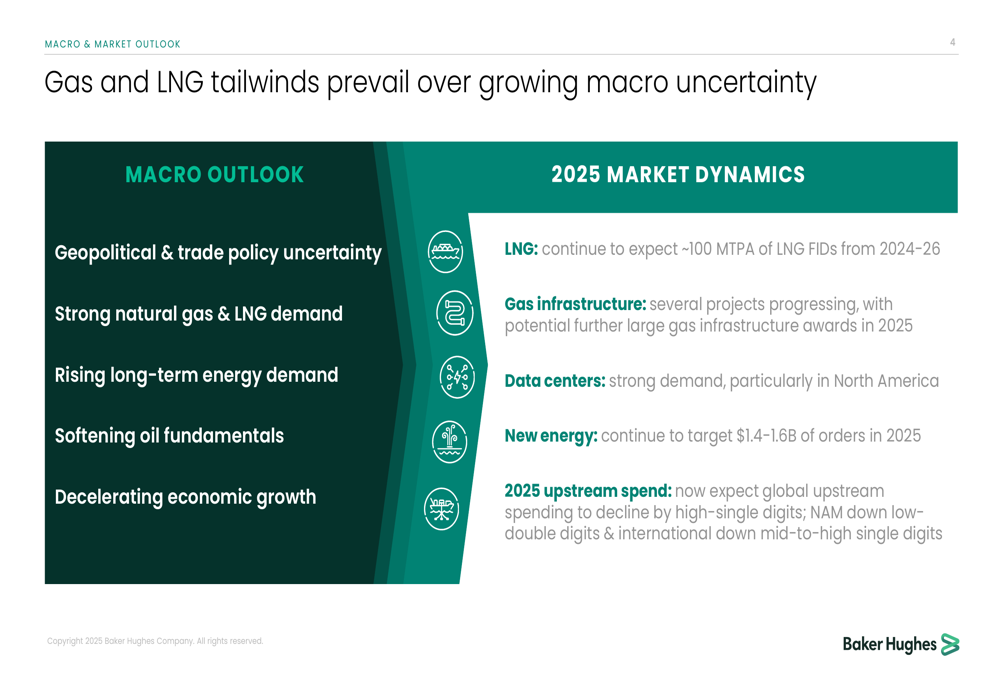

The broader market context remains complex, with Baker Hughes noting several key macro factors influencing its business: geopolitical and trade policy uncertainty, strong natural gas and LNG demand, rising long-term energy demand, softening oil fundamentals, and decelerating economic growth.

As shown in the following slide detailing the macro outlook and market dynamics for 2025, Baker Hughes continues to expect approximately 100 MTPA of LNG FIDs from 2024-26, while anticipating global upstream spending to decline by high-single digits:

Quarterly Performance Highlights

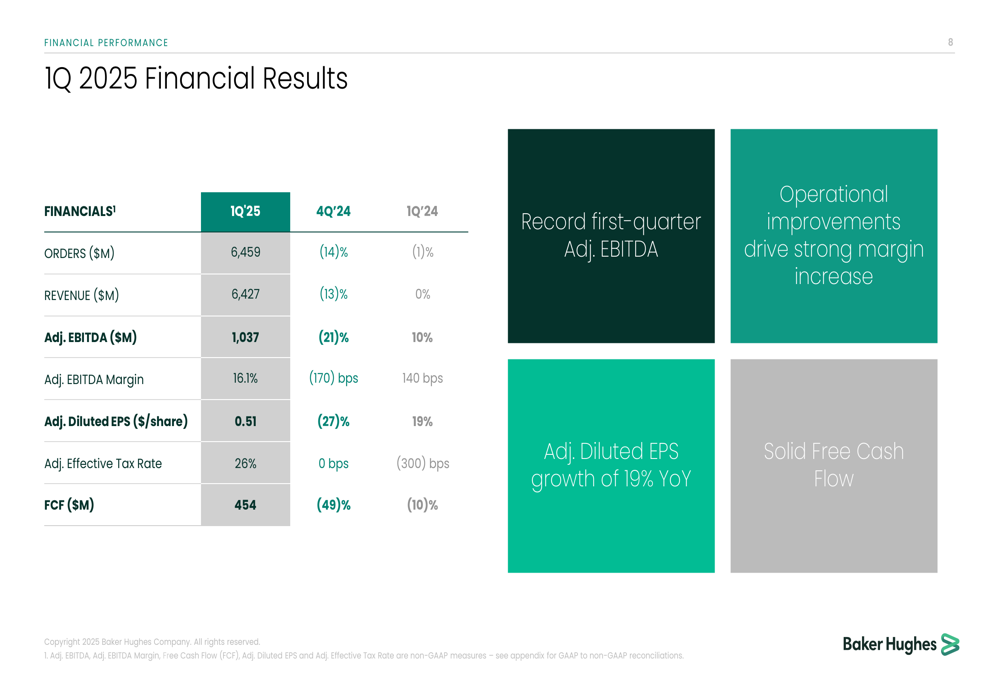

Baker Hughes reported orders of $6,459 million for Q1 2025, down 14% sequentially and 1% year-over-year. Revenue came in at $6,427 million, down 13% sequentially but flat compared to the same period last year. Despite these top-line challenges, the company achieved record first-quarter adjusted EBITDA of $1,037 million, representing a 10% increase year-over-year, with margins expanding by 140 basis points to 16.1%.

Adjusted diluted EPS reached $0.51, down 27% sequentially but up 19% year-over-year, demonstrating the company’s continued focus on operational improvements and margin enhancement. Free cash flow totaled $454 million, down 49% sequentially and 10% year-over-year.

The following financial results table provides a comprehensive overview of Baker Hughes’ Q1 2025 performance:

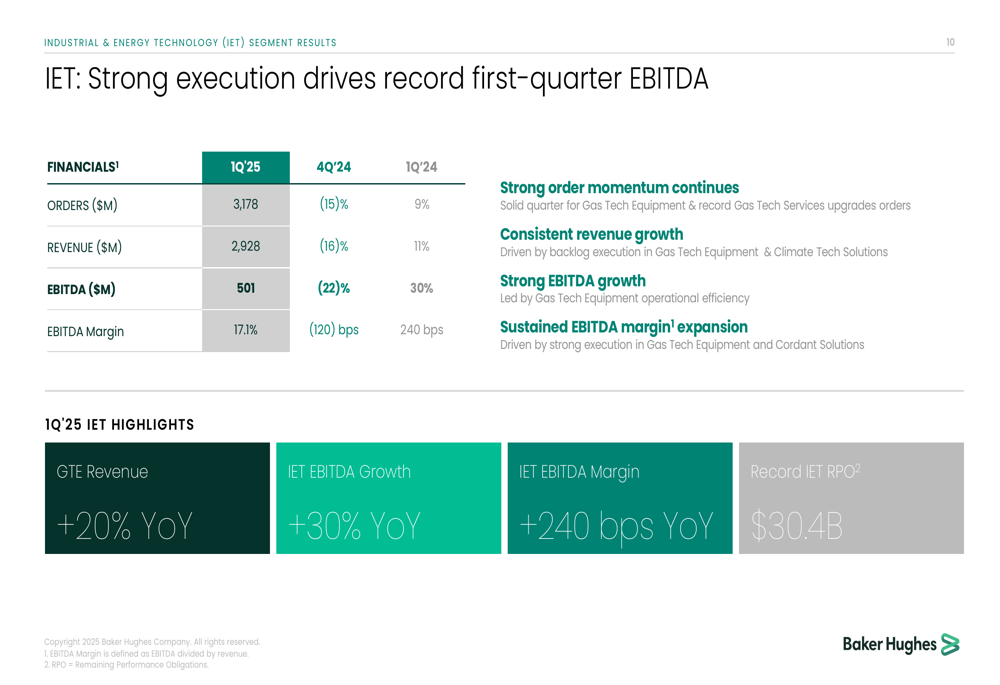

The company’s performance was driven by strong execution across both of its reporting segments. The Industrial & Energy Technology (IET) segment delivered particularly impressive results, with EBITDA growing 30% year-over-year to $501 million and margins expanding by 240 basis points to 17.1%, despite a 16% sequential revenue decline.

As illustrated in the IET segment performance slide below, the business continues to demonstrate strong order momentum, consistent revenue growth, and sustained margin expansion:

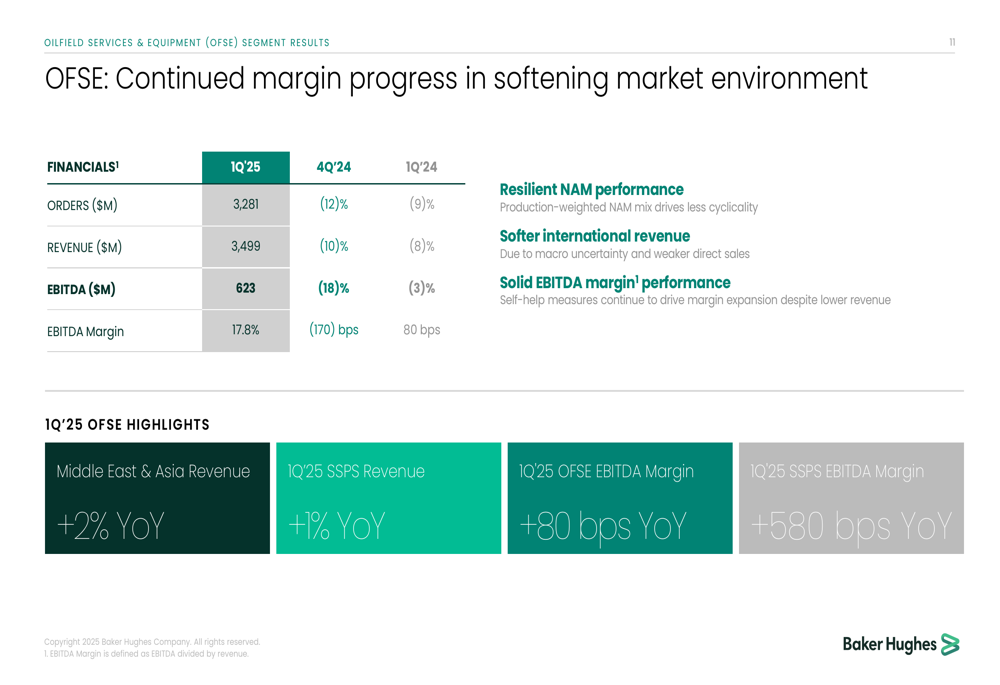

Meanwhile, the Oilfield Services & Equipment (OFSE) segment showed resilience in a softening market environment. While orders decreased 12% sequentially and 9% year-over-year to $3,281 million, and revenue declined 10% sequentially and 8% year-over-year to $3,499 million, the segment maintained solid EBITDA margin performance at 17.8%, representing an 80 basis point improvement year-over-year.

The following slide details OFSE’s performance amid challenging market conditions:

Strategic Initiatives

Baker Hughes highlighted several strategic wins during the quarter, demonstrating sustained commercial momentum across both new and existing end markets. A key development was the company’s entry into the data center market, securing orders for over 350 MW of Nova LT turbines.

The company also secured new long-term LNG commitments with NextDecade (NASDAQ:NEXT) and Argent LNG, providing enhanced visibility on future LNG orders. These agreements, along with significant upgrade awards in the Middle East and Algeria, underscore Baker Hughes’ strong positioning in the gas technology market.

The following slide outlines key awards and technology developments across various market segments:

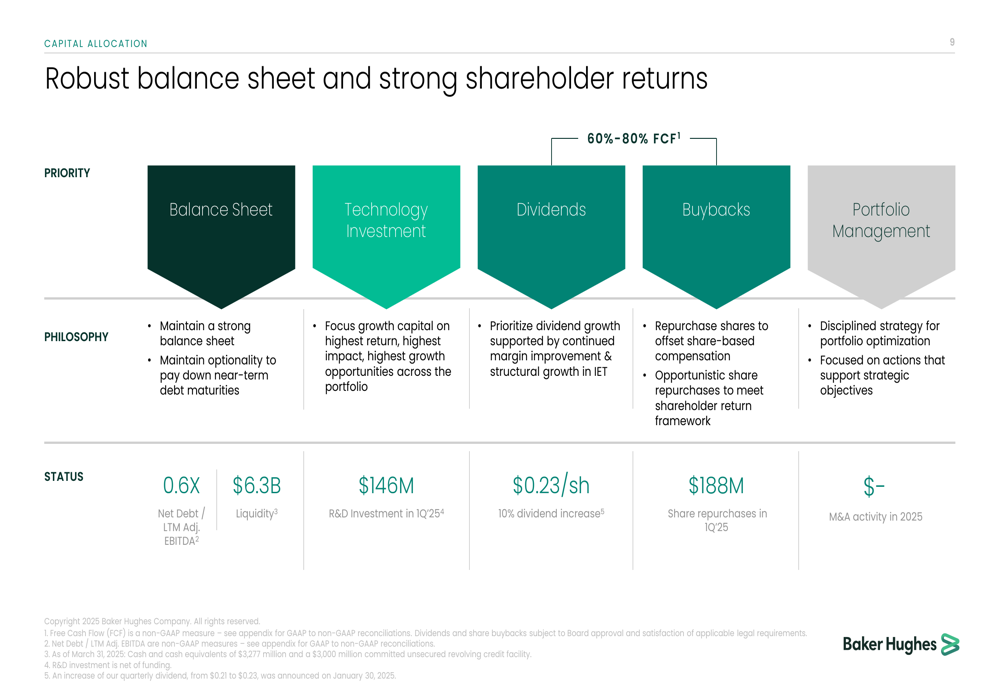

Baker Hughes continues to prioritize balanced capital allocation, focusing on maintaining a strong balance sheet while investing in technology and returning value to shareholders. In Q1 2025, the company repurchased $188 million of shares and commenced a higher quarterly dividend, demonstrating its commitment to shareholder returns.

The capital allocation framework is illustrated in the following slide:

Forward-Looking Statements

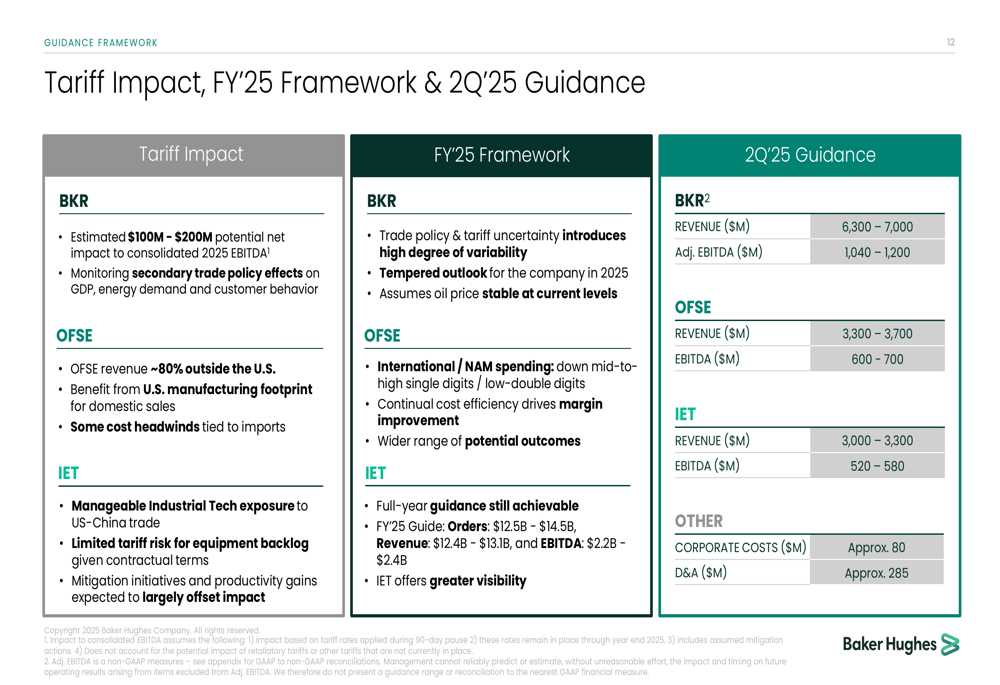

Looking ahead, Baker Hughes provided guidance for Q2 2025, projecting revenue of $6,300-7,000 million and adjusted EBITDA of $1,040-1,200 million. The company also addressed the potential impact of tariffs on its 2025 performance, estimating a $100-200 million potential net impact to consolidated EBITDA.

For the full year 2025, Baker Hughes acknowledged that trade policy and tariff uncertainty introduces a high degree of variability to its outlook. The company has tempered its expectations accordingly, while assuming stable oil prices.

The following slide details the tariff impact assessment, FY’25 framework, and Q2’25 guidance:

Conclusion

Baker Hughes’ Q1 2025 results demonstrate the company’s ability to drive margin expansion and operational improvements despite challenging market conditions. The diversification of its business portfolio, particularly the strong performance in the IET segment and expansion into data centers, is helping to offset softness in traditional upstream oil and gas markets.

While sequential declines in orders and revenue reflect current market headwinds, the year-over-year improvement in profitability metrics underscores the effectiveness of Baker Hughes’ strategic focus on high-margin, technology-driven solutions. The company’s balanced approach to capital allocation, with continued investment in technology while returning value to shareholders, positions it well to navigate the uncertain market environment in 2025.

Investors should monitor the impact of tariffs and the trajectory of upstream spending, which could present challenges to Baker Hughes’ growth outlook. However, the company’s strong positioning in natural gas, LNG, and new energy markets provides multiple growth avenues that could help mitigate these headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.