Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

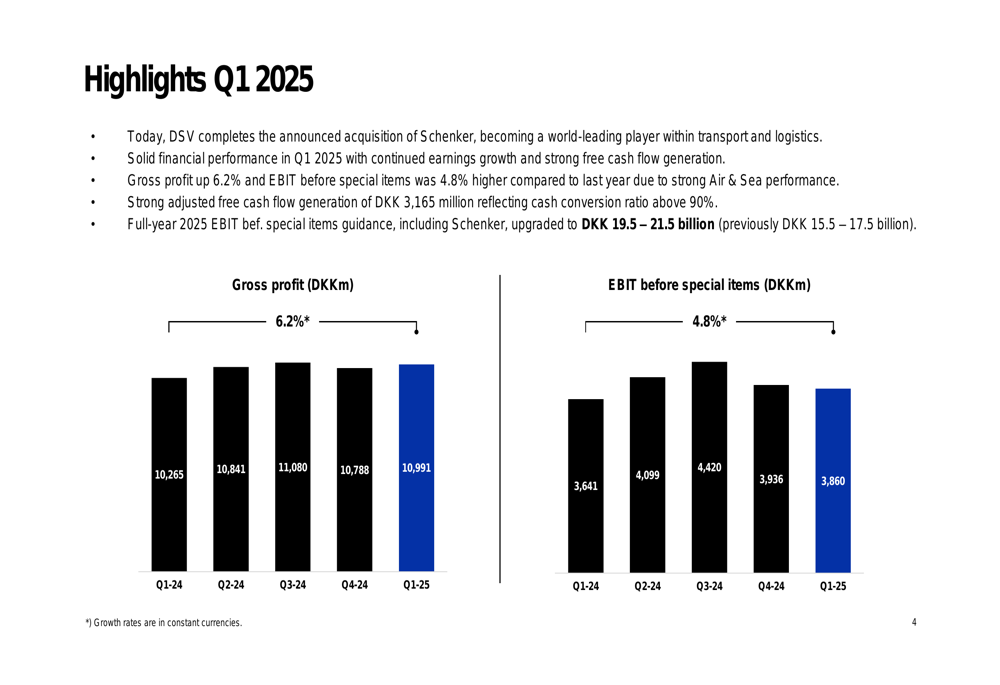

DSV A/S (CPH:DSV) announced the completion of its acquisition of Schenker alongside solid Q1 2025 financial results during its presentation on April 30, 2025. The landmark acquisition, valued at approximately DKK 106.7 billion (EUR 14.3 billion), transforms DSV into a global logistics powerhouse and prompted the company to significantly upgrade its full-year guidance.

The company reported continued earnings growth and strong free cash flow generation for the quarter, with performance primarily driven by the Air & Sea division, which offset challenges in the Road segment. The acquisition of Schenker marks a pivotal moment in DSV’s growth strategy, following its successful integration of previous acquisitions including UTi, Panalpina, and GIL.

Quarterly Performance Highlights

DSV delivered solid financial results in Q1 2025, with gross profit increasing by 6.2% and EBIT before special items rising by 4.8% compared to the same period last year. The company generated a strong adjusted free cash flow of DKK 3,165 million, reflecting a cash conversion ratio above 90%.

As shown in the following quarterly performance chart:

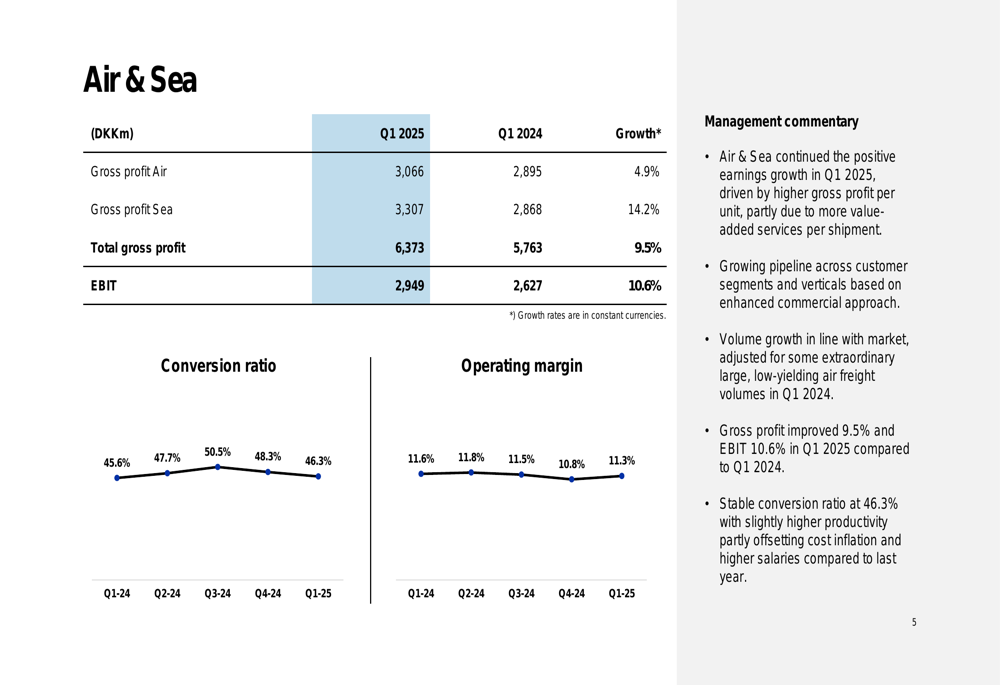

The Air & Sea segment was the standout performer, with gross profit increasing by 9.5% to DKK 6,373 million and EBIT rising by 10.6% to DKK 2,949 million compared to Q1 2024. The segment maintained a stable conversion ratio of 46.3%, with management noting that higher productivity partially offset cost inflation and increased salaries.

The detailed Air & Sea performance metrics reveal the strength of this division:

Breaking down the Air & Sea segment further, air freight volumes remained on par with the same period last year, while gross profit per unit increased by 5% in constant currencies. Management highlighted strong commercial momentum across several verticals, especially in technology.

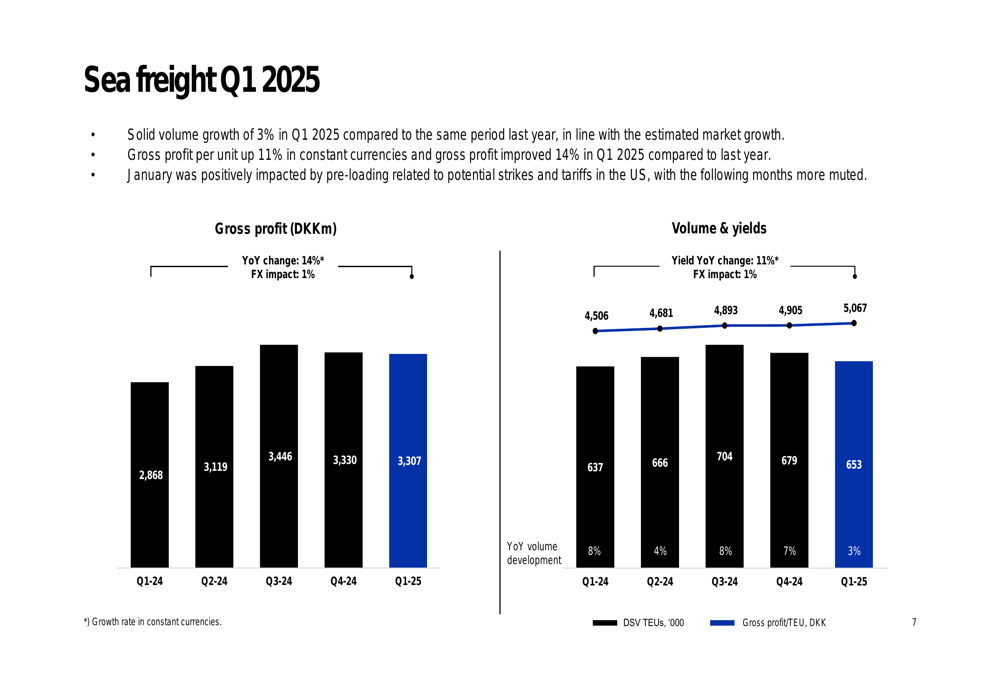

The sea freight business showed solid volume growth of 3% in Q1 2025, in line with estimated market growth. Gross profit per unit increased by 11% in constant currencies, leading to a 14% improvement in gross profit compared to last year.

In contrast, the Road segment faced challenges due to low activity levels, particularly in domestic groupage in some European markets. Revenue decreased by 3.0% to DKK 10,164 million, while EBIT declined by 16.9% to DKK 408 million. Management attributed the decrease to lower utilization, cost inflation, and higher depreciation related to new terminals.

The Solutions segment (to be renamed Contract Logistics following the Schenker transaction) experienced mixed results. Revenue increased by 4.9% to DKK 6,325 million and gross profit rose by 6.7% to DKK 2,578 million, but EBIT decreased by 6.3% to DKK 470 million. The division saw positive development in the US, while European markets remained impacted by soft activity levels in retail and automotive.

Schenker Acquisition Details

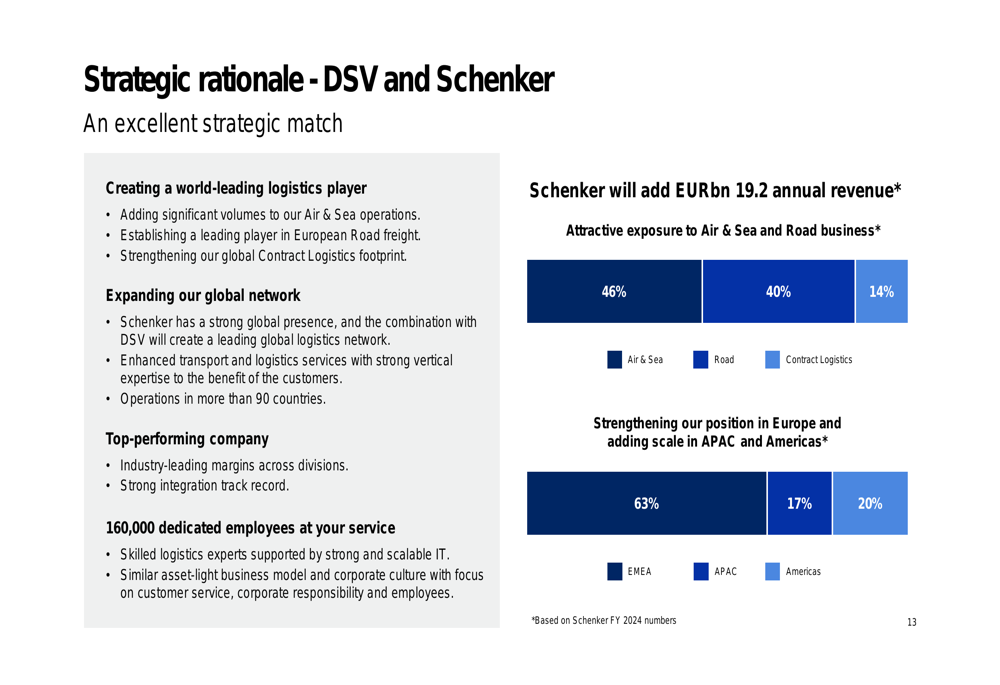

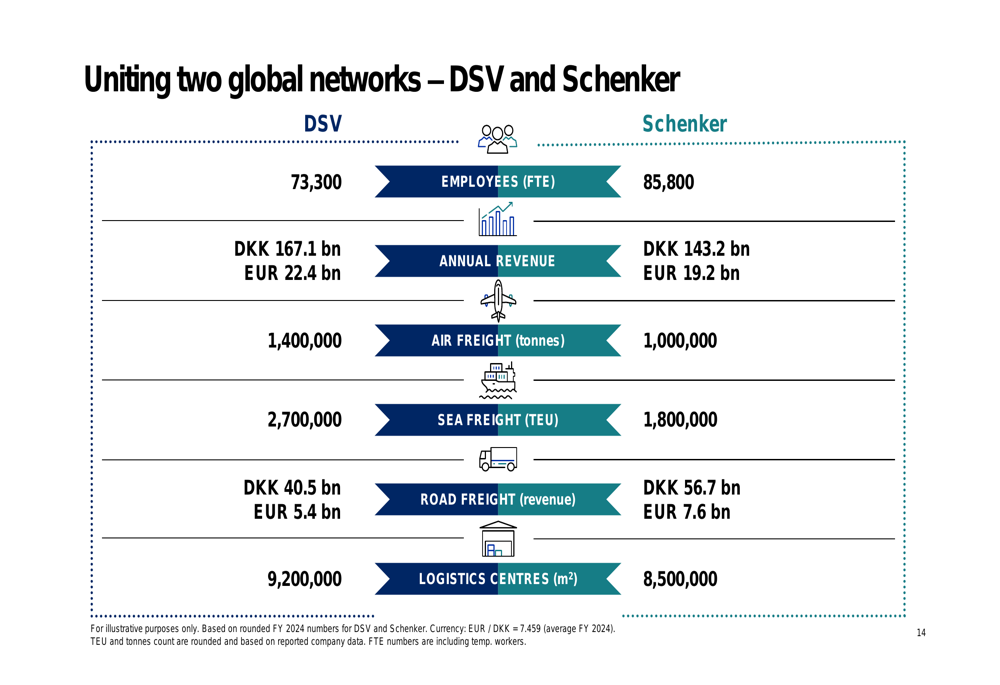

The acquisition of Schenker represents a transformative step in DSV’s growth strategy, creating a world-leading logistics player with significantly enhanced global reach and scale. The strategic rationale for the acquisition includes adding substantial volumes to Air & Sea operations and strengthening the global Contract Logistics footprint.

The following chart illustrates the strategic benefits of combining the two companies:

The acquisition creates an impressive global network, with the combined entity employing approximately 159,100 people and generating annual revenue of around EUR 41.6 billion. The business mix will be 46% Air & Sea, 40% Road, and 14% Contract Logistics, with a geographic distribution of 63% EMEA, 17% APAC, and 20% Americas.

The comparative metrics between DSV and Schenker before integration demonstrate the scale of this combination:

DSV successfully raised DKK 75.0 billion (EUR 10.0 billion) through equity and bonds to finance the transaction. The company expects annual synergies to reach DKK 9.0 billion by the end of 2028, with an aspiration to lift Schenker’s operating margins to DSV’s levels by 2028. The transaction is expected to be EPS accretive by 2026.

Management noted that total transaction and integration costs are expected to be around DKK 11.0 billion, with restructuring and integration costs of DKK 2.0-2.5 billion anticipated in 2025. Schenker will be included in DSV’s consolidated financial results from May 1, 2025.

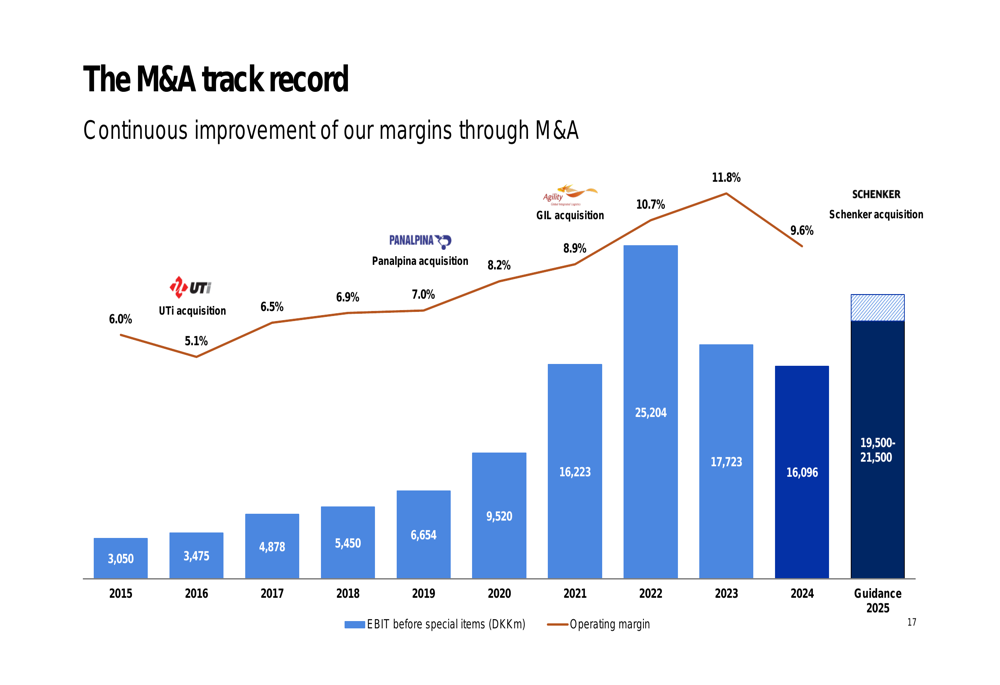

DSV has a strong track record of successful M&A integration, as illustrated in this historical performance chart:

Forward-Looking Statements

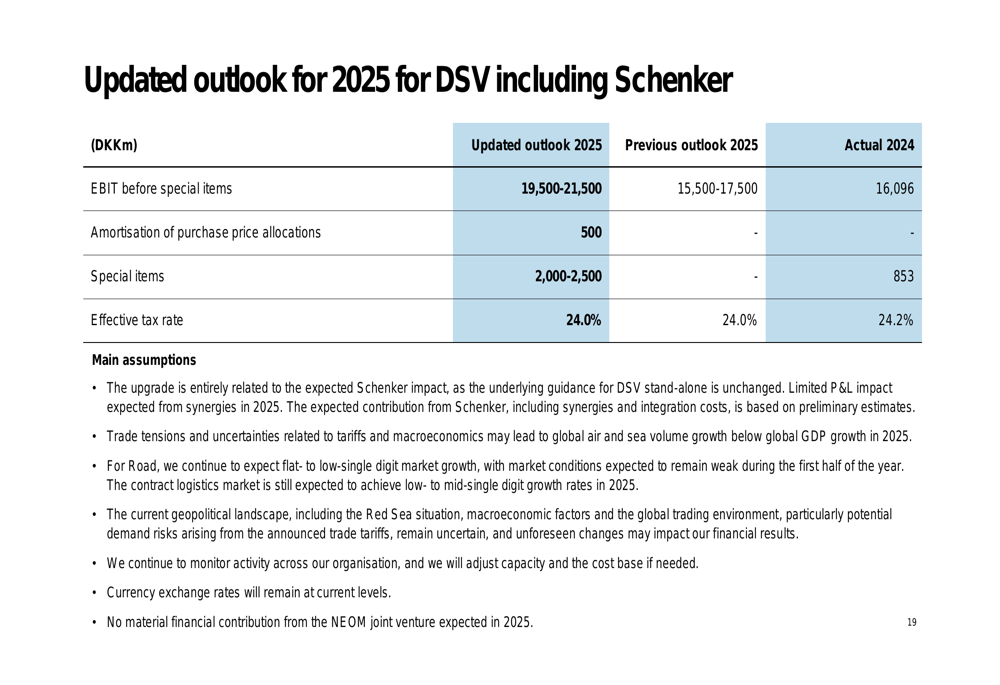

Following the Schenker acquisition, DSV has significantly upgraded its full-year 2025 guidance. The company now expects EBIT before special items to reach DKK 19.5-21.5 billion, up from the previous guidance of DKK 15.5-17.5 billion. This upgrade is entirely related to the expected Schenker impact, as the underlying guidance for DSV stand-alone remains unchanged.

The updated outlook for 2025 is presented in the following table:

Management expects limited P&L impact from synergies in 2025. The company anticipates that trade tensions and uncertainties related to tariffs and macroeconomics may lead to global air and sea volume growth below global GDP growth in 2025. For the Road segment, DSV continues to expect flat to low-single-digit market growth, with market conditions expected to remain weak during the first half of the year.

Executive Summary

DSV’s Q1 2025 results and the completion of the Schenker acquisition position the company for significant growth in the coming years. The Air & Sea division continues to drive performance with double-digit earnings growth, while the Road and Solutions segments face more challenging market conditions.

The Schenker acquisition represents a major strategic move that will substantially increase DSV’s global scale and reach. With expected synergies of DKK 9.0 billion by the end of 2028 and a strong track record of successful integrations, DSV is well-positioned to create significant shareholder value from this transaction.

The company’s upgraded guidance for 2025 reflects confidence in its ability to successfully integrate Schenker while maintaining solid organic performance. As the integration progresses, investors will be closely watching the realization of synergies and the company’s ability to lift Schenker’s operating margins to DSV’s levels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.