Gold prices stabilizes after Fed’s Williams signals a December rate cut

Introduction & Market Context

Indra Group (BME:IDR) presented its Q1 2025 financial results on May 6, 2025, highlighting solid performance across most business divisions. The Spanish technology and consulting company reported a 4% increase in revenues, driven primarily by 18% growth in its Defence segment, while transitioning from a net debt to a net cash position.

The company’s stock closed at €29.62 before the presentation and was trading down 3.85% at the time of the results announcement, suggesting some market adjustment to the mixed results that included a slight decline in net profit despite overall revenue growth.

Quarterly Performance Highlights

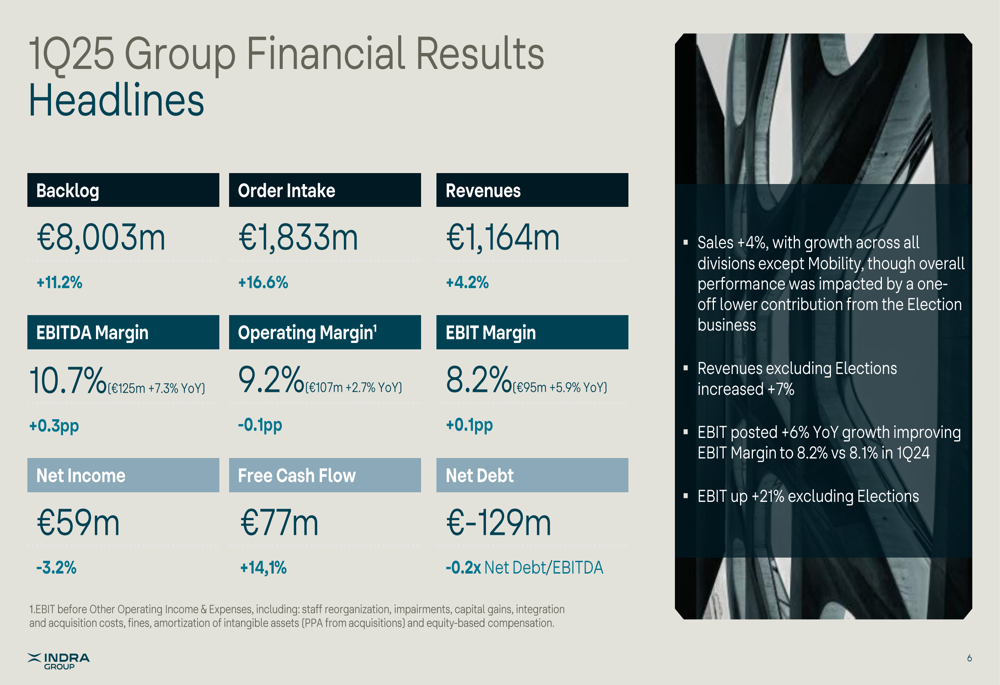

Indra reported Q1 2025 revenues of €1,164 million, up 4.2% year-over-year, with growth across all divisions except Mobility, which remained flat. Excluding the Election business, which had a lower one-off contribution this quarter, revenues increased by a more robust 7%.

As shown in the following financial results summary:

The company’s backlog grew 11.2% to €8,003 million, while order intake increased 16.6% to €1,833 million, indicating strong future revenue potential. EBITDA rose 7.3% to €125 million, improving margin by 0.3 percentage points to 10.7%. EBIT increased 5.9% to €95 million, with margin slightly up to 8.2%.

Net income declined 3.2% to €59 million, which the company attributed to higher financial costs and taxes. Free cash flow showed strong improvement, up 14.1% to €77 million compared to Q1 2024.

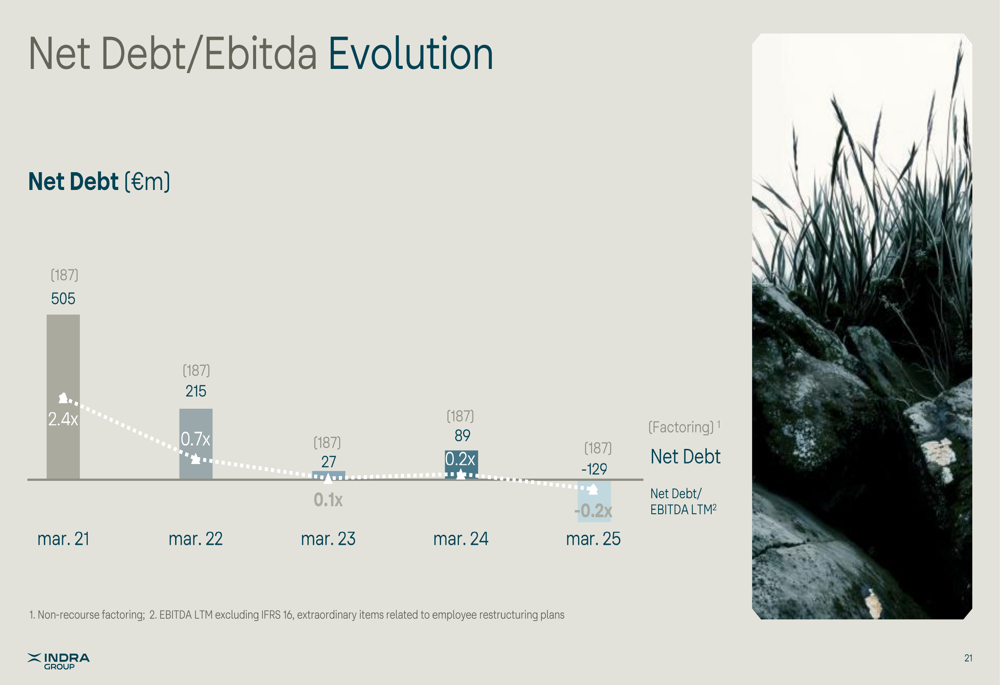

A significant financial milestone was Indra’s shift to a net cash position of €129 million, compared to a net debt of €89 million in March 2024, representing a Net Debt/EBITDA ratio of -0.2x.

Detailed Financial Analysis

Defence Division

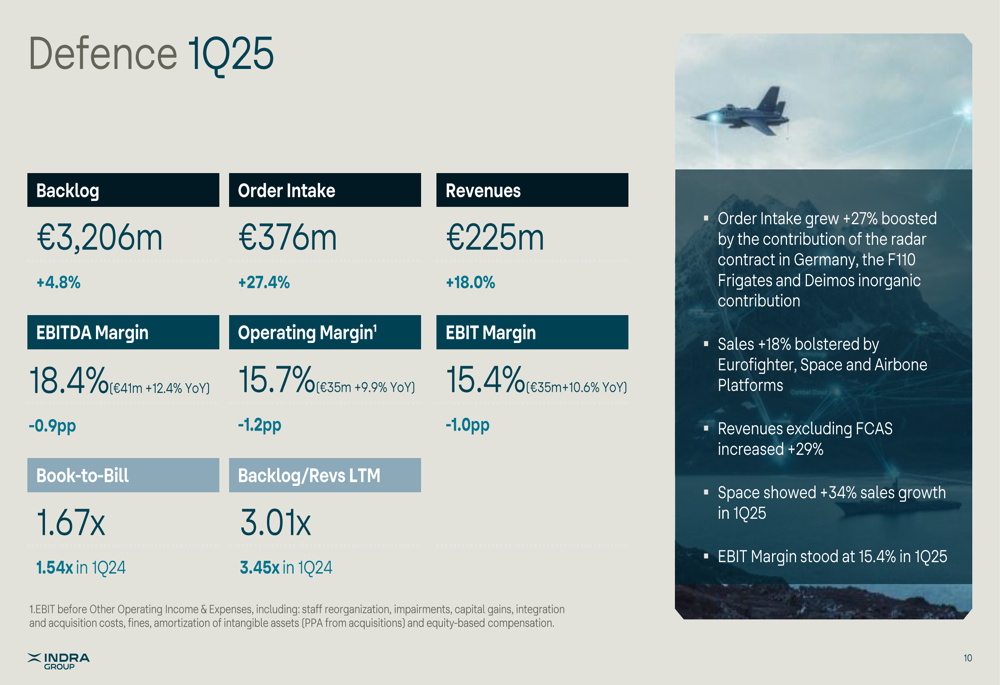

The Defence division was the standout performer, with revenues increasing 18% to €225 million. Excluding the Future Combat Air System (FCAS) program, revenue growth was even more impressive at 29%. Order intake grew 27.4% to €376 million, bolstered by radar contracts in Germany, F110 Frigate work, and the inorganic contribution from Deimos.

The following chart details the Defence division’s performance:

The division maintained strong profitability with an EBIT margin of 15.4%, though this represented a slight decrease of 1 percentage point year-over-year. Space activities showed particularly strong growth at 34% in Q1 2025.

Air Traffic Management

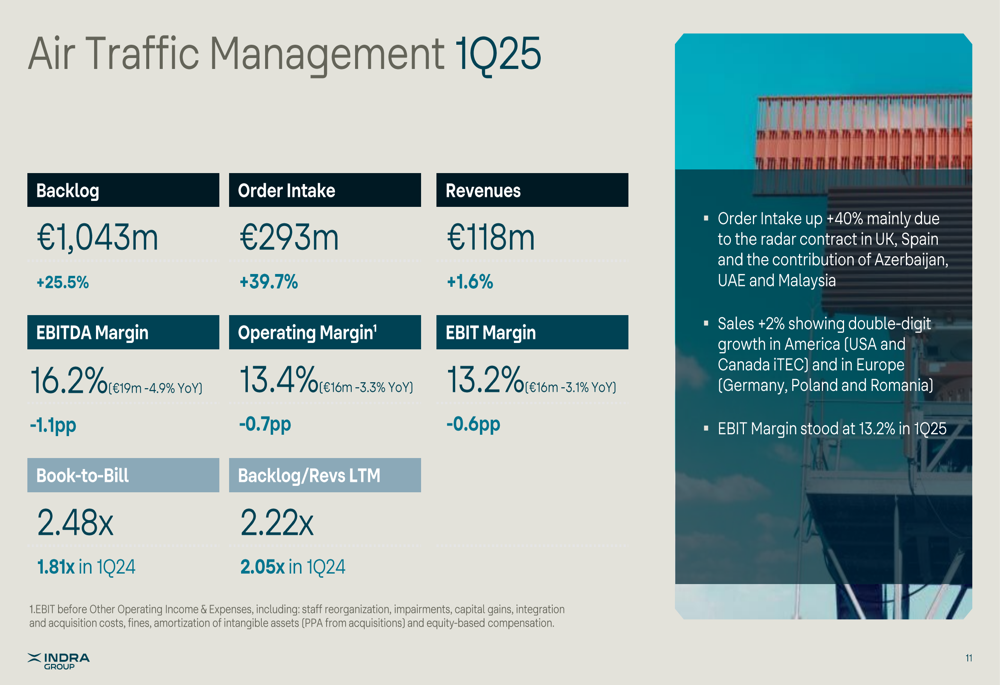

The Air Traffic Management division saw modest revenue growth of 1.6% to €118 million, but order intake surged 39.7% to €293 million, driven by radar contracts in the UK, Spain, Azerbaijan, UAE, and Malaysia.

As illustrated in this divisional breakdown:

The division’s book-to-bill ratio improved to 2.48x from 1.81x in Q1 2024, indicating strong future revenue potential. EBIT margin remained solid at 13.2%, though slightly down 0.6 percentage points from the previous year.

Mobility

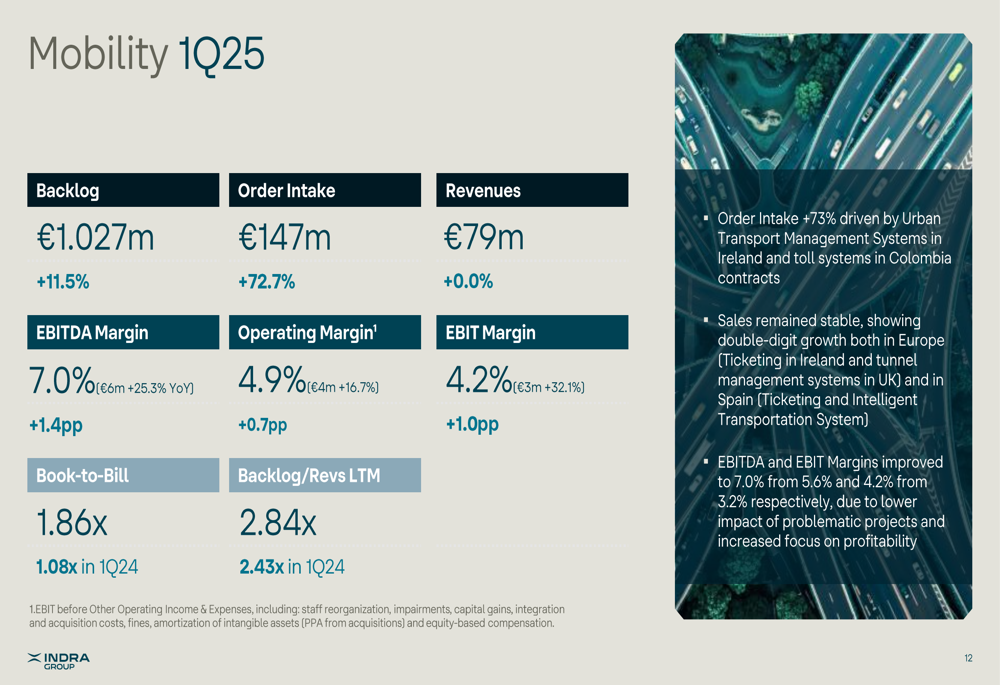

While Mobility revenues remained flat at €79 million, order intake jumped 72.7% to €147 million, driven by Urban Transport Management Systems contracts in Ireland and toll systems in Colombia.

The division’s performance is detailed here:

Profitability improved significantly, with EBITDA margin increasing to 7.0% from 5.6% and EBIT margin rising to 4.2% from 3.2%, which the company attributed to lower impact from problematic projects and increased focus on profitability.

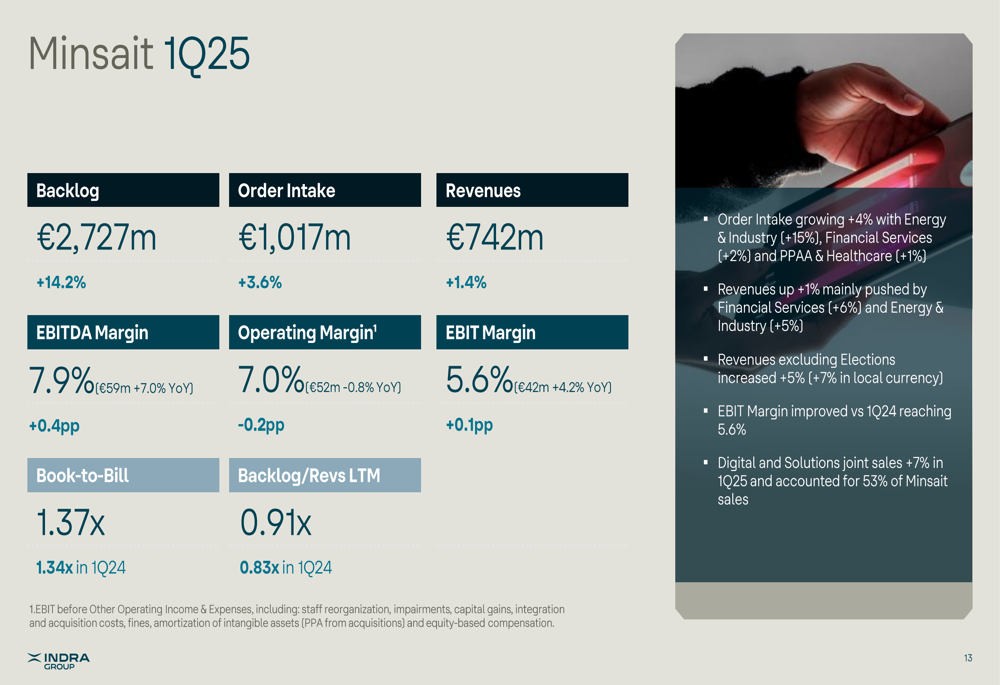

Minsait

Minsait, Indra’s IT services division and largest by revenue, posted a modest 1.4% increase in revenues to €742 million. Excluding the Elections business, revenue growth was 5% (7% in local currency).

The division’s performance metrics are shown here:

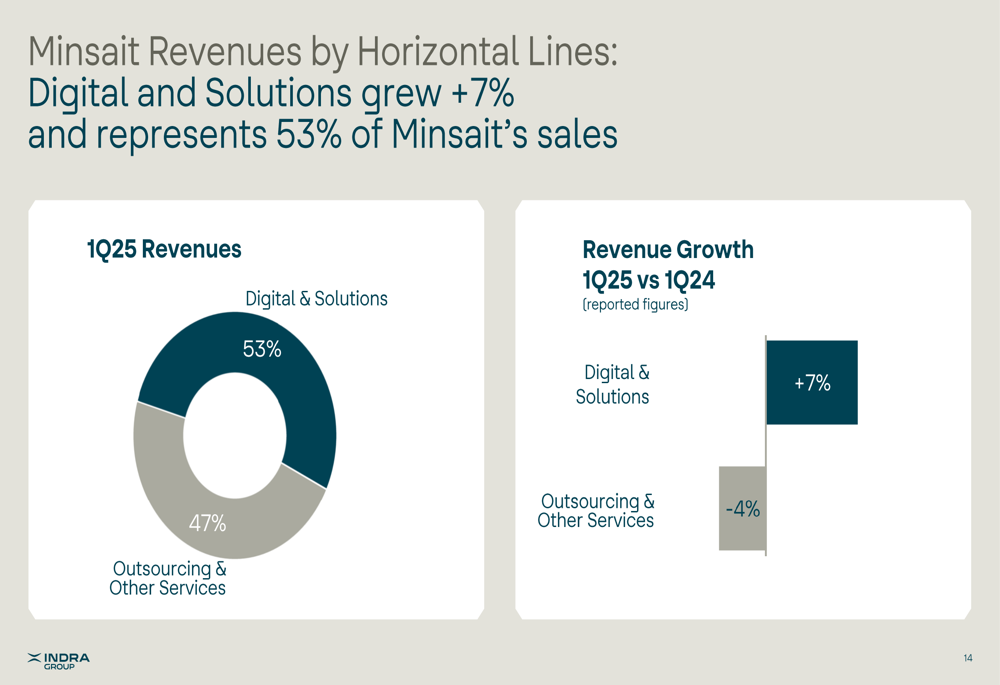

Within Minsait, Digital and Solutions services grew 7% and now represent 53% of the division’s sales, reflecting the company’s strategic shift toward higher-value services:

Financial Services and Energy & Industry were the strongest performing sectors within Minsait, growing 6% and 5% respectively, while Telecom (BCBA:TECO2m) & Media and Public Administration & Healthcare both declined by 5%.

Strategic Initiatives

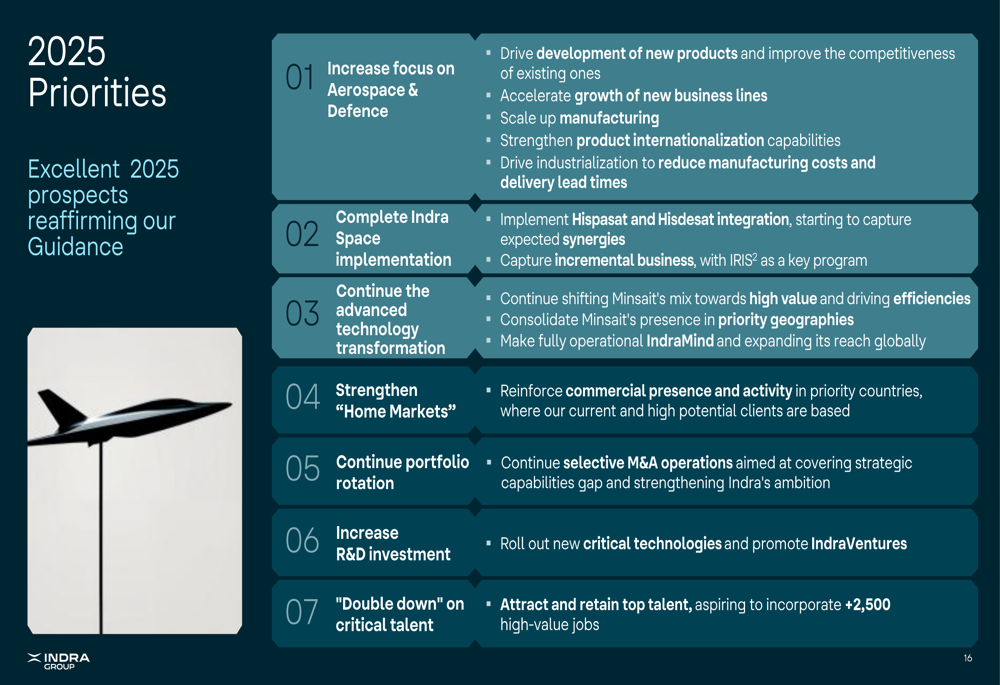

Indra outlined seven key priorities for 2025, with increased focus on Aerospace & Defence at the top of the list. The company plans to drive development of new products, accelerate growth in new business lines, scale up manufacturing, and strengthen internationalization capabilities.

The company’s strategic roadmap is detailed in this slide:

Other priorities include completing the Indra Space implementation through the integration of Hispasat and Hisdesat (expected by Q4 2025), continuing technological transformation, strengthening presence in "home markets," portfolio rotation through selective M&A, increasing R&D investment, and attracting critical talent.

A notable strategic development was the signing of a Memorandum of Understanding between Indra and Rheinmetall (ETR:RHMG) to upgrade Spanish Leopard 2E Main Battle Tanks, reinforcing the company’s position in the defence sector.

The company also announced the launch of IndraMind, an AI Platform for automating critical and multi-domain operations, with a business plan to be presented in the 1H 2025 results presentation.

Forward-Looking Statements

Indra reaffirmed its commitment to its 2025 financial guidance and to the targets of its 2026 Strategic Plan, "Leading the Future." The company expects Defence net order intake to double in 2025 compared to 2024, driven by increased military expenditure.

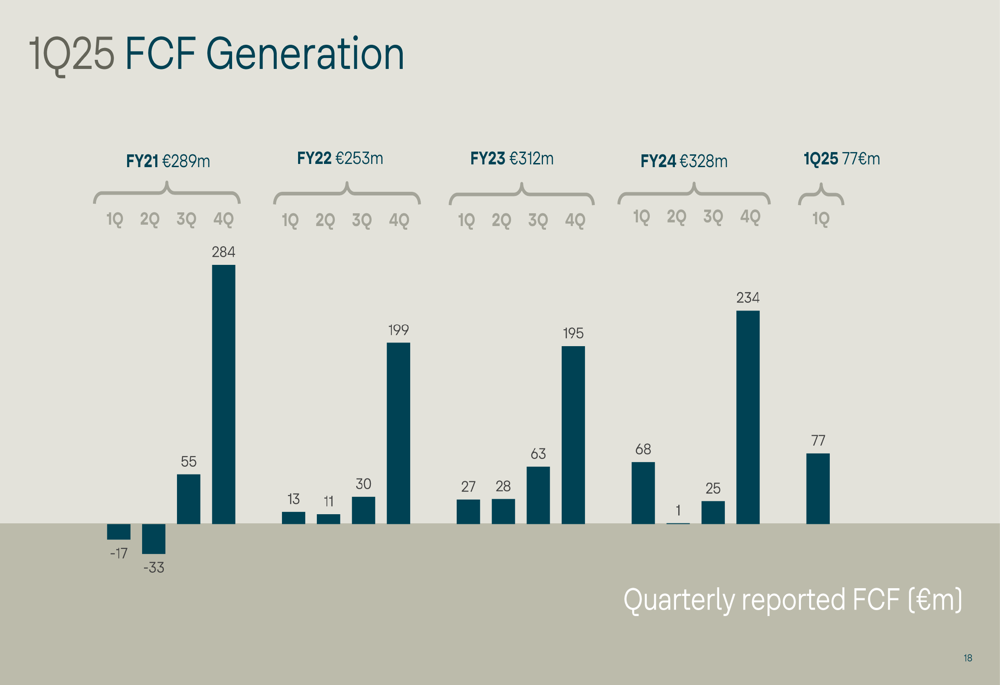

The company’s free cash flow generation has shown consistent improvement over recent years, with Q1 2025 marking the strongest first quarter in the company’s recent history:

Indra’s financial position has strengthened considerably, as evidenced by the evolution of its Net Debt/EBITDA ratio over the past five years:

With a diversified debt structure, available credit facilities of €905 million, and an improved average debt life of 3.3 years (up from 1.5 years in Q1 2024), the company appears well-positioned to pursue its strategic initiatives and capitalize on growth opportunities, particularly in the Defence sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.