Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Introduction & Market Context

OneMain Holdings Inc (NYSE:OMF) presented its second quarter 2025 financial results on July 25, 2025, showcasing strong year-over-year growth and improved credit metrics. The company, which positions itself as the "Lender of Choice for the Nonprime Consumer," reported significant improvements in capital generation and delinquency rates while continuing to expand its product offerings beyond traditional personal loans.

The stock responded positively to the results, with premarket trading showing a 1.91% increase to $59.75. This follows a slight decline after Q1 results despite an earnings beat, suggesting investors are increasingly confident in OneMain’s strategy and execution.

Quarterly Performance Highlights

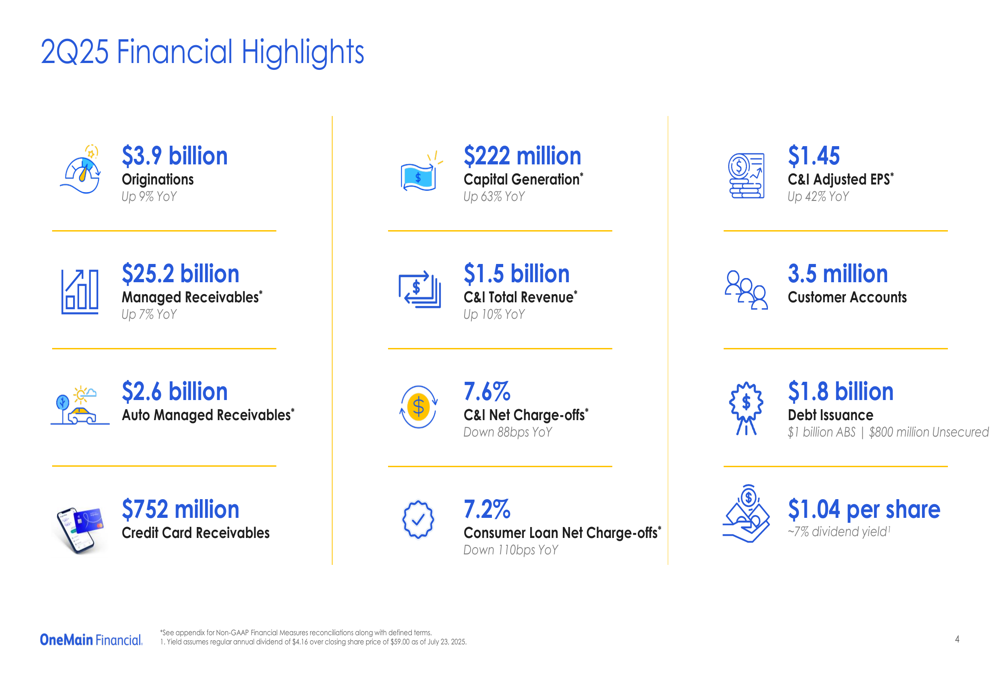

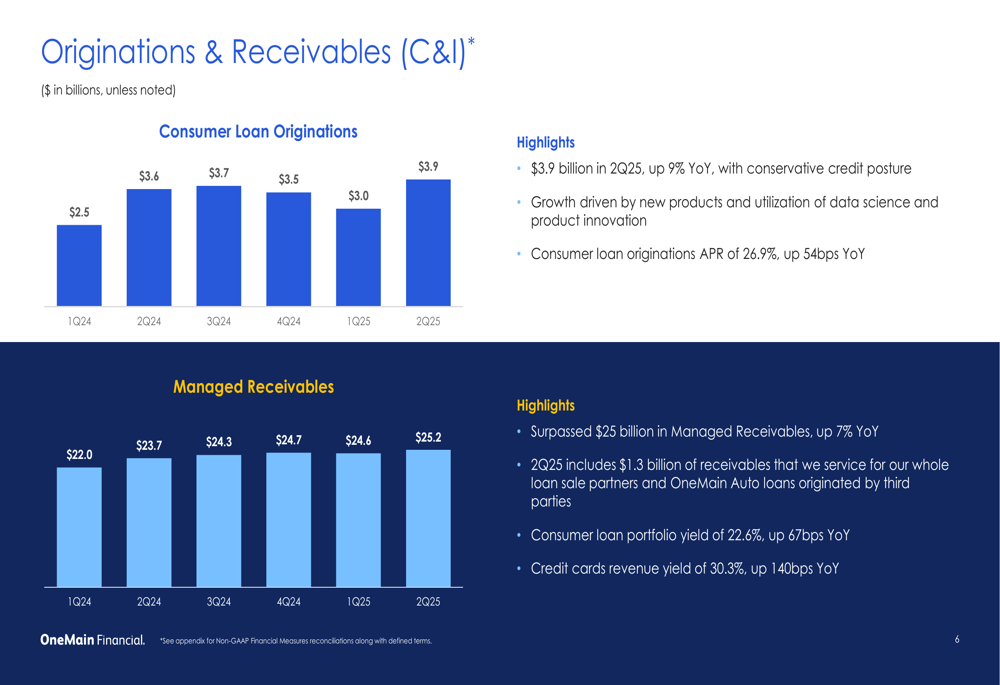

OneMain reported robust financial results for Q2 2025, with several key metrics showing strong year-over-year improvement. The company generated $3.9 billion in originations, representing a 9% increase compared to the same period last year.

As shown in the following comprehensive overview of key financial metrics:

Particularly noteworthy is the company’s capital generation, which reached $222 million, up 63% year-over-year. Consumer & Insurance (C&I) adjusted earnings per share came in at $1.45, representing a 42% increase from Q2 2024. While this represents a sequential decline from the $1.72 reported in Q1 2025, the year-over-year growth demonstrates the company’s improving fundamentals.

Total (EPA:TTEF) revenue for the C&I segment reached $1.5 billion, up 10% year-over-year, while managed receivables grew to $25.2 billion, a 7% increase compared to Q2 2024. The company maintained a strong dividend yield of approximately 7%, with a quarterly dividend of $1.04 per share.

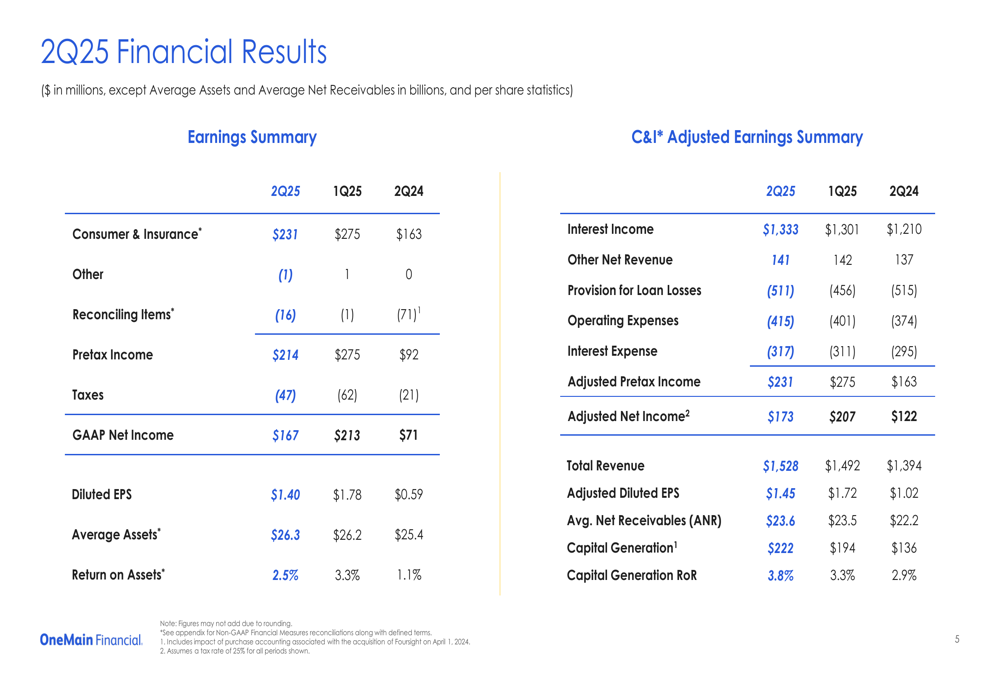

The detailed financial summary shows the progression across key metrics:

Credit Quality Improvements

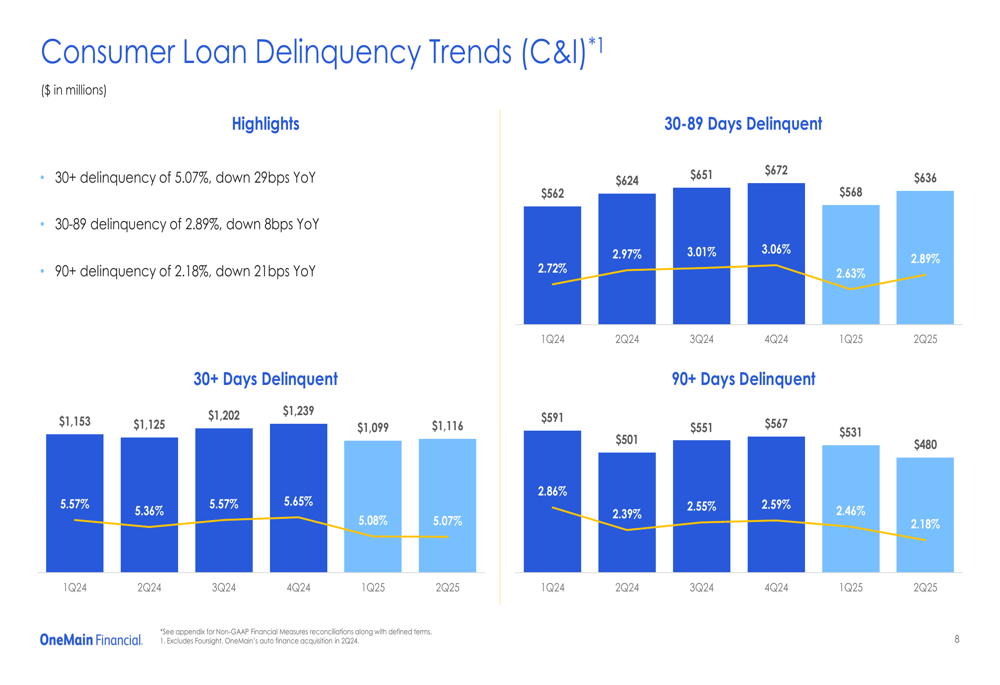

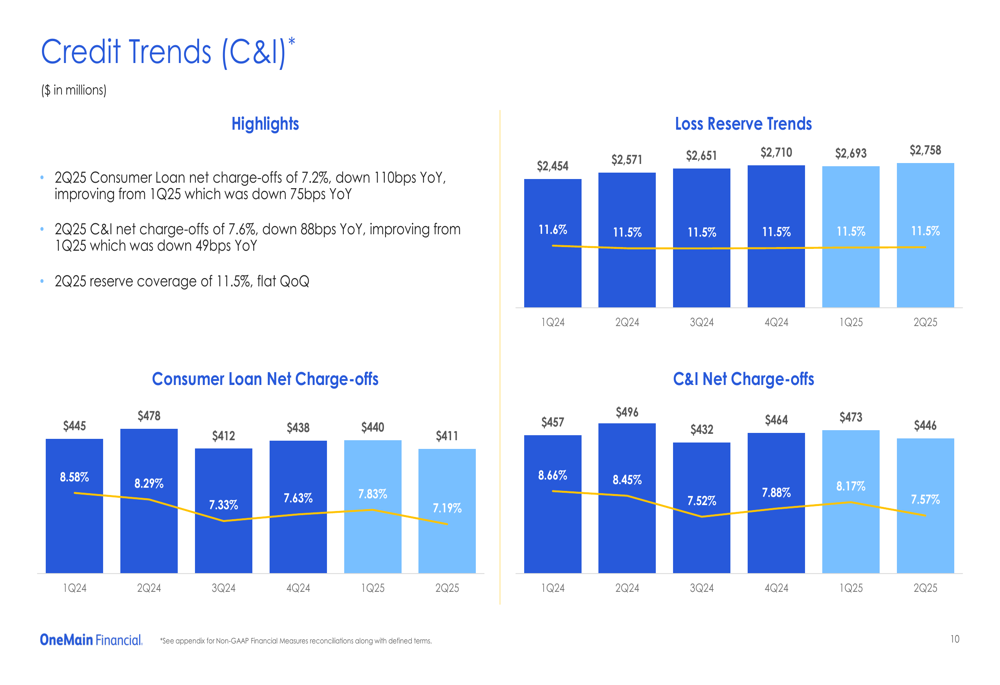

A standout aspect of OneMain’s Q2 results was the significant improvement in credit quality metrics. The company reported consumer loan net charge-offs of 7.2%, down 110 basis points year-over-year, while overall C&I net charge-offs decreased to 7.6%, an 88 basis point improvement from Q2 2024.

The following chart illustrates the positive trend in delinquency rates:

The 30+ day delinquency rate improved to 5.07%, down 29 basis points year-over-year, while the 90+ day delinquency rate decreased to 2.18%, a 21 basis point improvement. These improvements are particularly significant given the challenging economic environment for non-prime consumers.

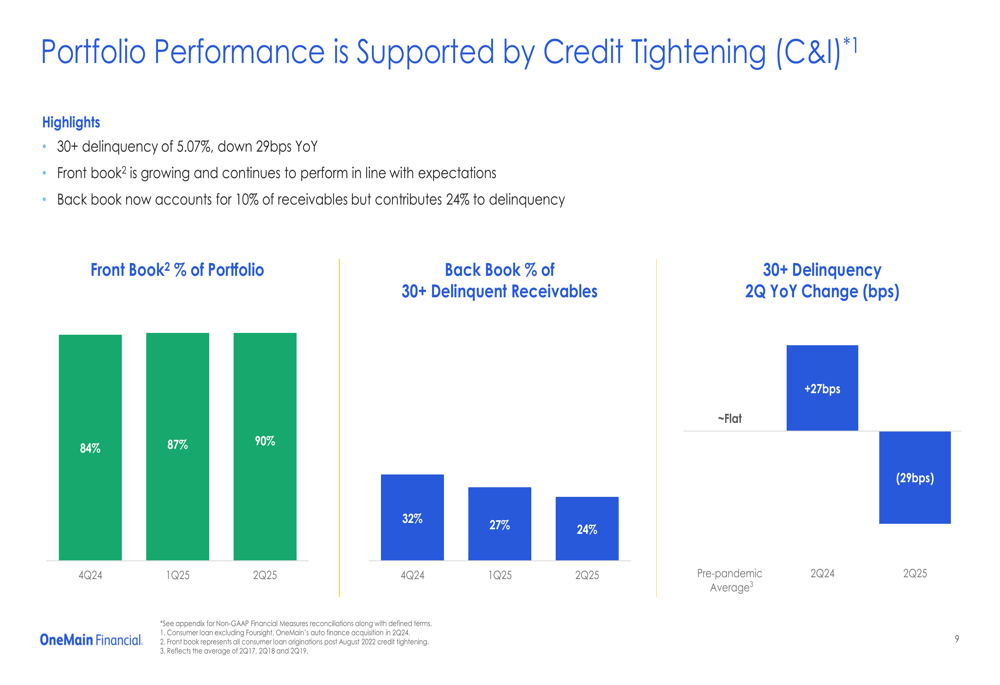

OneMain attributes these improvements to its strategic credit tightening initiatives implemented over the past several quarters. The company’s "front book" of newer loans now comprises 90% of the portfolio, up from 84% in Q4 2024, while the "back book" accounts for just 24% of delinquent receivables, down from 32% in Q4 2024.

As illustrated in this portfolio performance breakdown:

The company’s loss reserve remained stable at 11.5% of receivables, indicating a continued conservative approach to credit risk management despite the improving delinquency trends.

New Product Growth

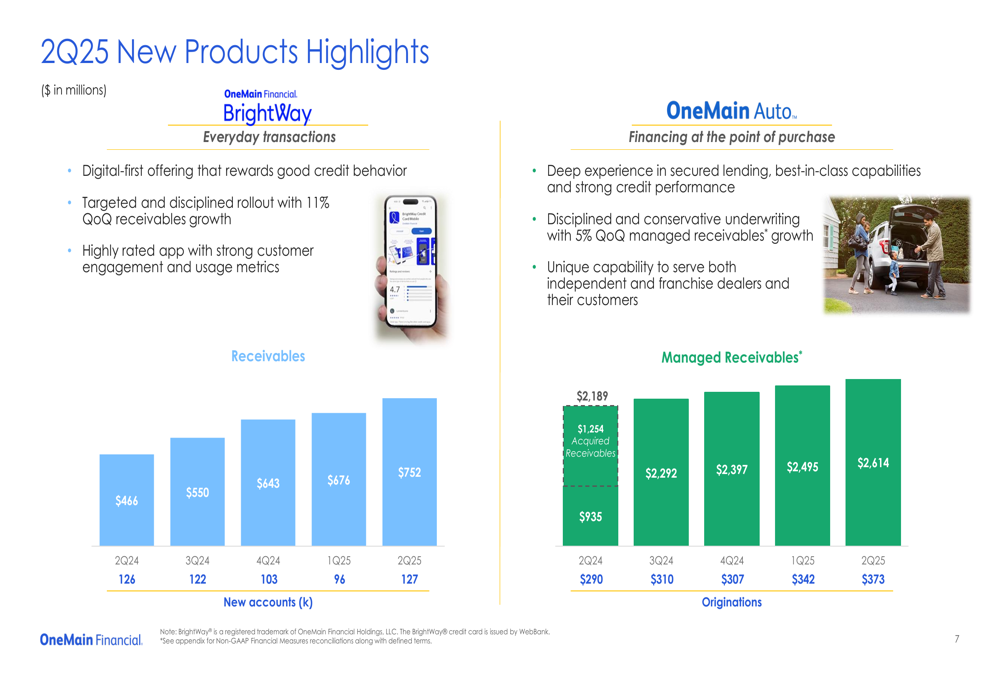

OneMain continues to make progress on its diversification strategy, with significant growth in both its credit card and auto finance offerings. The BrightWay credit card program saw receivables increase to $752 million in Q2 2025, up from $466 million in Q2 2024, with 127,000 new accounts opened during the quarter.

The following chart details the growth trajectory of these new product initiatives:

Similarly, OneMain Auto’s managed receivables reached $2.6 billion, with originations of $373 million in Q2 2025, up from $290 million in the same period last year. The auto segment continues to leverage the company’s experience in secured lending and disciplined underwriting approach.

These new product lines represent important growth vectors for OneMain as it expands beyond its traditional personal loan business. The company’s vision encompasses a broader range of financial products and services designed to meet the needs of non-prime consumers.

Strategic Outlook & Guidance

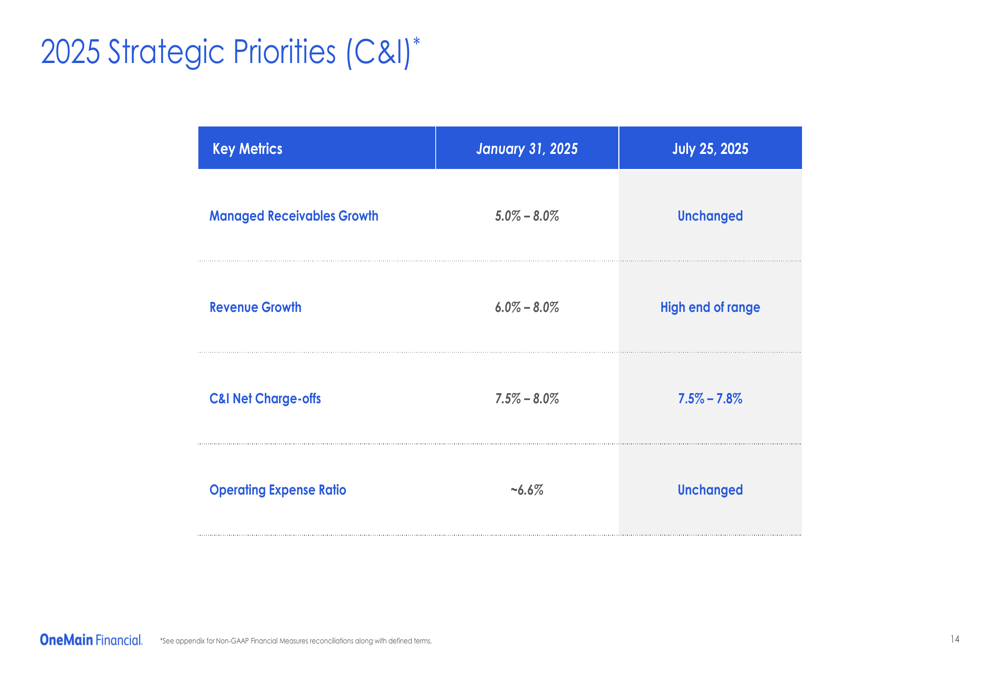

OneMain maintained most of its 2025 strategic priorities, projecting managed receivables growth of 5.0-8.0% and an operating expense ratio of approximately 6.6%. The company raised its revenue growth guidance to the high end of its 6.0-8.0% range and slightly improved its C&I net charge-off guidance to 7.5-7.8% from the previous 7.5-8.0%.

The updated strategic priorities are outlined in the following table:

The company’s capital allocation framework continues to balance business investment, regular dividends, and share repurchases. In Q2 2025, OneMain repurchased 460,000 shares for $21 million while maintaining its quarterly dividend of $1.04 per share.

OneMain’s balance sheet remains well-positioned, with a diversified funding structure and manageable debt maturities. The company issued $1.8 billion in debt during the quarter, comprising $1 billion in asset-backed securities and $800 million in unsecured debt.

Detailed Financial Analysis

Operating expenses for the C&I segment increased to $415 million in Q2 2025, representing 6.7% of receivables, slightly up from 6.4% in Q2 2024 but in line with the company’s annual target of approximately 6.6%. This modest increase reflects OneMain’s continued investments in technology and new product initiatives while maintaining overall cost discipline.

The company’s originations and managed receivables both showed consistent growth over the past six quarters, with originations rebounding strongly in Q2 after a seasonal dip in Q1:

OneMain’s performance in Q2 2025 demonstrates the company’s ability to generate strong financial results while improving credit quality and expanding its product offerings. The significant improvements in capital generation and credit metrics, combined with the successful growth of new product initiatives, position the company well for continued success in the non-prime consumer lending market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.