Vivek Ramaswamy buys Strive Inc (ASST) stock worth $1.25 million

- Mega-cap tech earnings, PCE inflation data, Q1 GDP in focus this week.

- McDonald’s stock is a buy with earnings due on Tuesday.

- Intel shares set to underperform amid huge Q1 loss, bleak outlook.

Stocks on Wall Street ended little changed on Friday as investors weighed the latest round of corporate earnings results while continuing to focus on recession fears as well as the Federal Reserve’s monetary policy outlook.

All three major U.S. stock indexes finished the week in the red, with the Dow Jones Industrial Average slipping 0.2% to snap a four-week win streak. The benchmark S&P 500 and the tech-heavy Nasdaq dipped 0.1% and 0.4% respectively.

The coming week is expected to be an extremely busy one as Q1 earnings season shifts into high gear, with reports expected from mega-cap tech companies Microsoft (NASDAQ:MSFT), Google-parent Alphabet (NASDAQ:GOOGL), Amazon (NASDAQ:AMZN), and Meta Platforms (NASDAQ:META).

The earnings agenda also consists of other high-profile names, including Snap (NYSE:SNAP), Coca-Cola (NYSE:KO), PepsiCo (NASDAQ:PEP), Boeing (NYSE:BA), Exxon Mobil (NYSE:XOM), Chevron (NYSE:CVX), Caterpillar (NYSE:CAT), General Electric (NYSE:GE), 3M Company (NYSE:MMM), Verizon (NYSE:VZ), Visa (NYSE:V), Mastercard (NYSE:MA), Merck (NYSE:MRK), Eli Lilly (NYSE:LLY), American Airlines (NASDAQ:AAL), Southwest Airlines (NYSE:LUV), and UPS (NYSE:UPS).

All told, about 35% of the companies in the S&P 500 will report results next week.

On the economic calendar, most important will be Friday’s core personal consumption expenditures (PCE) price index, which is the Federal Reserve’s preferred inflation measure. As per Investing.com, analysts expect both the month-over-month (+0.3%) and year-over-year rates (+4.5%) to remain at elevated levels.

In addition, there is also important first-quarter GDP data due on Thursday, which will provide more clues as to whether the economy is heading for recession.

Markets are currently pricing in an 89.1% chance of a 25 basis point hike at the May policy meeting, according to Investing.com’s Fed Rate Monitor Tool.

Regardless of which direction the market goes, below I highlight one stock likely to be in demand and another which could see further downside.

Remember though, my timeframe is just for the week ahead, April 24-28.

Stock To Buy: McDonald’s

I believe McDonald’s (NYSE:MCD) stock will extend its rally in the week ahead, with a breakout to new record highs on the horizon, as the fast-food giant’s first quarter earnings update will surprise to the upside in my view, thanks to favorable consumer demand trends and a robust fundamental outlook.

McDonald’s is scheduled to deliver its Q1 report before the U.S. market open on Tuesday and results are once again likely to benefit from higher menu prices as U.S. consumers flock to its restaurants amid the current economic backdrop.

Many Americans have cut back spending at traditional full-service restaurants in response to persistently high inflation and a slowing economy, boosting demand for McDonald’s iconic lineup of ‘Big Mac’ burgers and chicken ‘McNuggets’.

Not surprisingly, an Investing Pro survey of analyst earnings revisions points to mounting optimism ahead of the report, with analysts raising their EPS estimates 17 times in the past three months, while making just two downward revisions.

Source: InvestingPro

Consensus expectations call for McDonald’s to post earnings per share of $2.34, rising 2.6% from EPS of $2.28 in the year-ago period. Revenue is forecast to dip 1.6% year-over-year to $5.58 billion.

Despite the expected decline in sales growth, I reckon U.S. Q1 same-store sales - which track sales at stores open for at least 12 months - will easily surpass expectations. Outside the U.S., international same-store sales are also expected to improve from a year ago, fueled by strong performance in the U.K., Germany, France, Japan, and Brazil.

The Chicago, Illinois-based fast-food chain has beaten Wall Street’s top-line expectations in seven of the past eight quarters, while trailing revenue estimates only twice in that span, a testament to the resilience of its underlying business and strong execution across the company.

MCD ended at a fresh all-time peak of $292.06 on Friday, above the prior record high close of $291.27 from two days earlier. McDonald’s has a market cap of $213.2 billion at its current valuation.

Year-to-date, shares of the fast-food restaurant chain, which is one of the 30 components of the Dow Jones Industrial Average, are up 10.8% to vastly outperform the blue-chip index over the same timeframe.

Stock To Sell: Intel

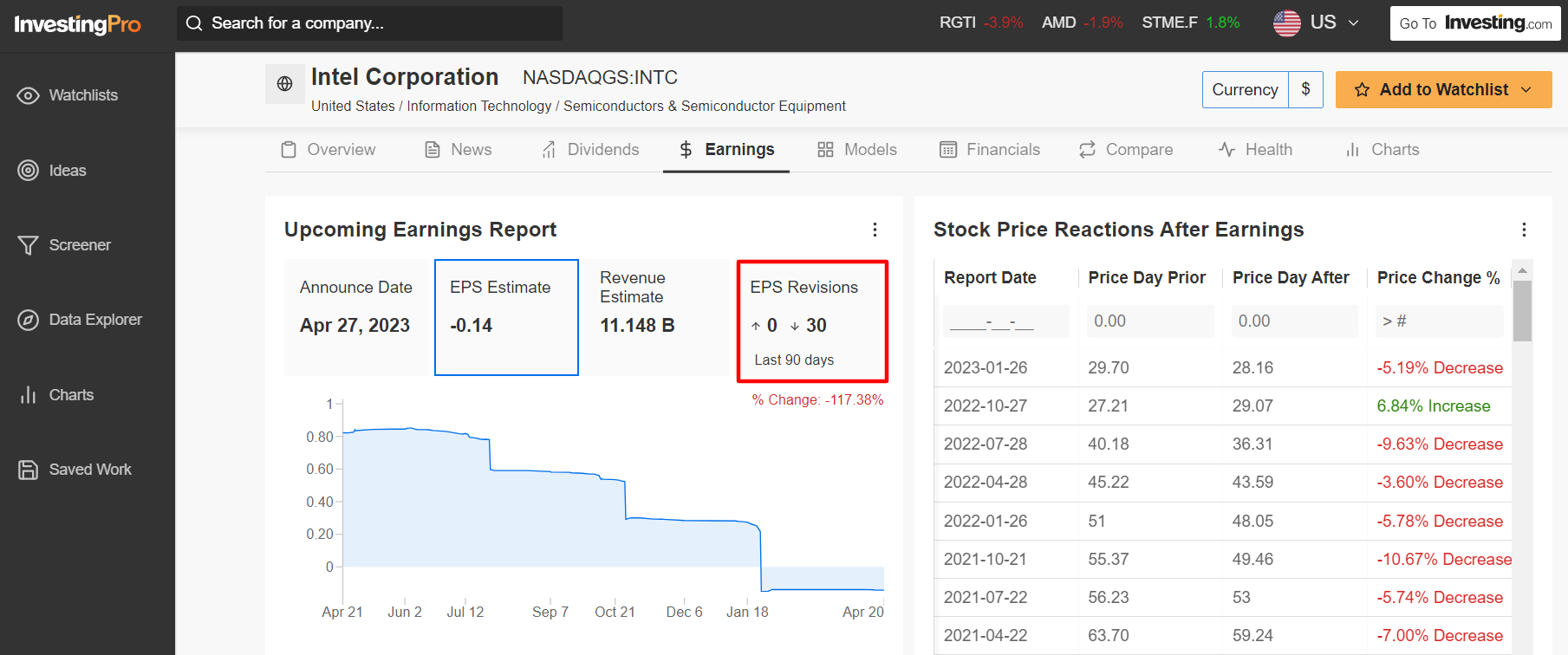

I expect shares of Intel (NASDAQ:INTC) to underperform in the week ahead as the struggling semiconductor company prepares to deliver dismal financial results after the closing bell on Thursday, April 27 due to the challenging operating environment.

Based on moves in the options market, traders expect a sizable swing in INTC shares following the results, with a possible implied move of roughly 7% in either direction.

Analysts have sharply lowered expectations heading into Intel’s first quarter earnings report, as per Investing Pro data: over the last three months, EPS estimates have seen 30 downward revisions compared to zero upward revisions.

Source: InvestingPro

According to InvestingPro, Wall Street sees the Santa Clara, California-based chipmaker losing $0.14 a share, compared to earnings of $0.87 in the year-ago period.

If confirmed, it would mark one of Intel’s biggest quarterly losses in its history, underscoring the several challenges the company currently faces.

Revenue is expected to plunge 39.3% year-over-year to $11.1 billion, amid a sluggish performance in its all-important chip business, weak data center sales, as well as dwindling PC demand from consumers.

Looking ahead, it is my belief that Intel’s forward guidance will point to further near-term weakness as I become increasingly concerned by the chipmaker’s future prospects.

Once considered the undisputed leader in the computer processors industry, Intel has been steadily losing market share in recent years to rivals such as Advanced Micro Devices (NASDAQ:AMD), Nvidia (NASDAQ:NVDA), and Taiwan Semi (NYSE:TSM). In addition, its business has also suffered as more and more Big Tech companies, including Apple (NASDAQ:AAPL), Microsoft, and Amazon, opt to develop their own chips and microprocessors.

INTC stock, which slumped to a bear-market low of $24.59 in October 2022, ended at $30.30 on Friday. At current valuations, Intel has a market cap of $125.3 billion.

Shares are up 14.6% so far in 2023, amid a broad-based rebound in the semiconductor space. Notwithstanding the recent turnaround, INTC stock remains more than 55% away from its January 2020 all-time high of $69.29.

Disclosure: At the time of writing, I am short on the S&P 500 and Nasdaq 100 via the ProShares Short S&P 500 ETF (SH) and ProShares Short QQQ ETF (PSQ). I regularly rebalance my portfolio of individual stocks and ETFs based on ongoing risk assessment of both the macroeconomic environment and companies' financials. The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.